Taxation & Compliance

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

TL;DR

GST e-Invoice is a government-validated electronic invoice system under India’s GST regime.

E-invoices must be generated for eligible transactions by businesses with an annual total revenue of more than ₹5 crore.

To receive an Invoice Reference Number (IRN) and QR code, e-invoices must be reported to the Invoice Registration Portal (IRP).

Businesses with revenue above ₹10 crore are required to disclose bills within 30 days starting in April 2025; otherwise, an IRN cannot be obtained.

Under GST rules, non-compliance can render an invoice invalid and result in fines and ITC denial.

e-Invoicing enhances transparency, decreases reconciliation errors, and streamlines GST return filing.

Why is GST e-invoice crucial in 2026?

India's tax system has gradually changed to become more digital, transparent, and compliant in real time. One of this transformation's most important structural changes is the GST e-invoice. What started out as a 2020 compliance requirement for big corporations has now spread to mid-sized and expanding companies nationwide.

GST e-invoicing is no longer a specialised area of compliance in 2026. Now that the barrier has been lowered to ₹5 crore in total yearly turnover, a large group of SMEs, exporters, agencies, SaaS firms, and service providers are covered. Understanding e-invoice regulations is crucial for these companies not only to prevent fines but also to guarantee continuous operations, easy submission of GST returns, and a steady flow of input tax credits.

Invoice-level reporting has become essential to maintaining compliance integrity as GST systems become more linked and data-driven. This blog provides businesses with a structured and useful explanation of all they need to know about GST e-invoicing 2026.

What is GST e-invoice? (Explanation in Simple Words)

A GST e-invoice is not simply a digital invoice sent via email. A tax invoice that has been electronically verified by the government's Invoice Registration Portal (IRP) is referred to as an e-invoice under the GST framework.

The invoice is initially created by the supplier using their ERP or accounting software. However, the invoice data must be posted to the IRP in a specified JSON format prior to being sent to the customer. The system creates a unique Invoice Reference Number (IRN) and a digitally signed QR code after validation. For businesses to which e-invoicing is applicable, the invoice only becomes legally legitimate under GST law after the IRN is received.

The main goals of GST e-invoicing are to limit tax leakage, establish a consistent standard for invoice reporting throughout India, and facilitate smooth interaction between the e-way bill, GST return, and invoicing systems.

GST e-Invoice Applicability in 2026

The first step to compliance is understanding whether GST e-invoices apply to your business.

Turnover-Based Applicability

Businesses whose total yearly revenue in any given fiscal year exceeds ₹5 crore will be required to use GST e-invoicing as of 2026. Since the turnover is determined on a PAN basis, all GSTINs under that PAN are required to comply if one GST registration exceeds the specified threshold.

Unless otherwise exempted, the rule remains in effect even if the turnover surpasses ₹5 crore in a single fiscal year.

Transactions Covered Under GST e-Invoicing

E-invoicing primarily applies to B2B supplies. This covers exports, presumed exports, supply to SEZ units, supplies to registered individuals, and credit or debit notes issued in connection with these activities.

B2C transactions, however, are not covered by e-invoicing. Regardless of turnover, some taxpayer categories are now excluded from e-invoicing obligations, including banks, insurance businesses, NBFCs, goods transport agencies, passenger transport services, and government offices.

Determining applicability accurately is essential because, under GST law, submitting a regular invoice when an electronic invoice is required can make the invoice void.

Who Must Generate an e-Invoice Under GST?

One of the most frequent queries that companies have is: Who must create a GST e-invoice? The Aggregate Annual Turnover (AATO) of a taxpayer during a fiscal year is used to evaluate if GST e-invoicing is applicable. In an effort to increase compliance and transparency, the government has progressively lowered the requirement over time, enrolling more companies in the e-invoicing system.

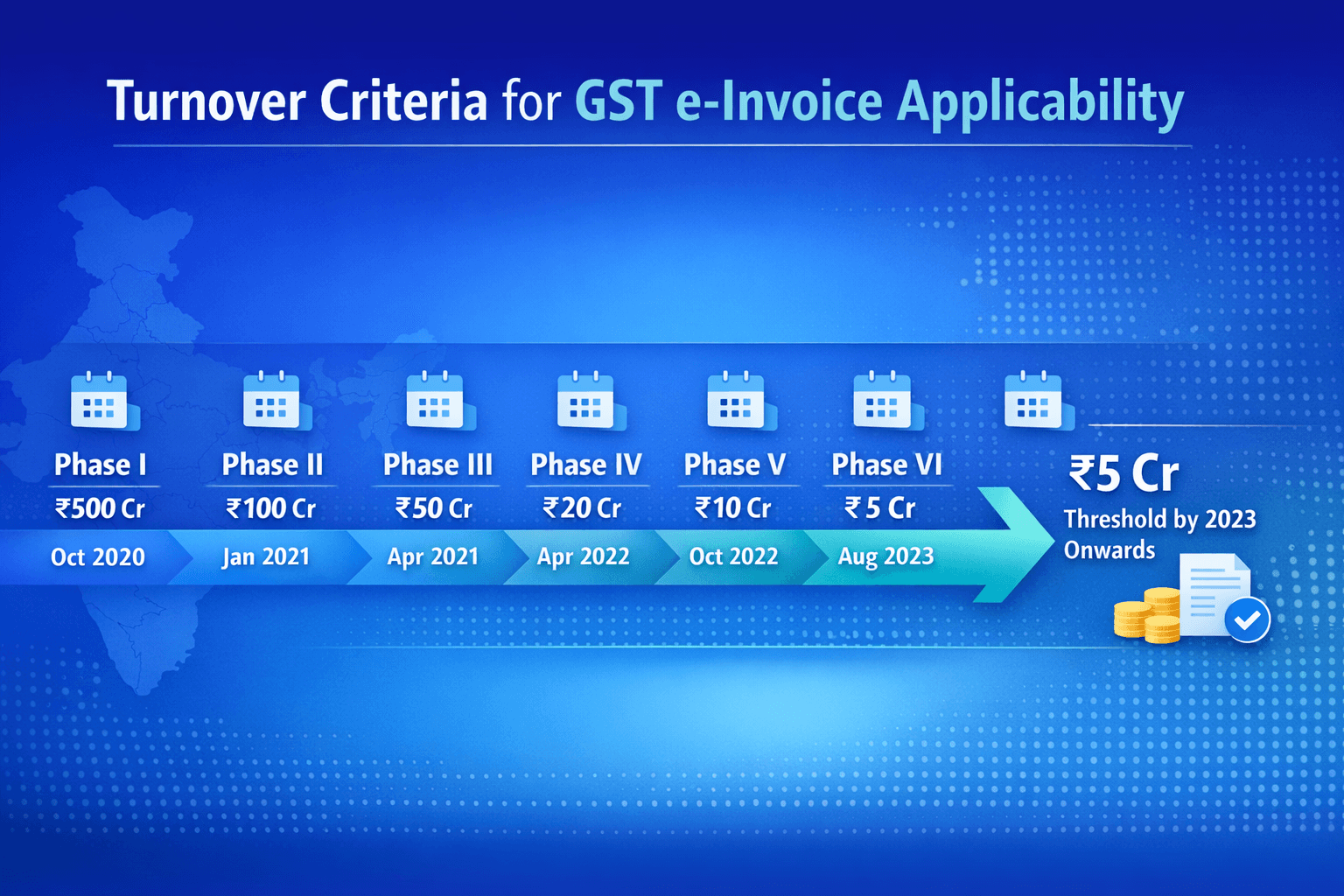

Turnover Criteria for GST e-Invoice Applicability

Not every organisation is required to create an electronic invoicing right away. Rather, it was applied in stages, progressively reducing the turnover cap.

When GST e-invoicing was initially implemented in October 2020, it was limited to companies with a total revenue of more than ₹500 crore. To increase coverage, the government gradually lowered this cap over the ensuing years. The threshold was lowered to ₹5 crore by August 2023, greatly broadening the scope of India's required e-invoicing.

Here is how the rollout progressed:

Phase I (Effective 1 October 2020)

E-invoicing became mandatory for taxpayers with aggregate turnover exceeding ₹500 crore, as per Notification No. 61/2020 – Central Tax and 70/2020 – Central Tax.

Phase II (Effective 1 January 2021)

The turnover threshold was reduced to ₹100 crore under Notification No. 88/2020 – Central Tax.

Phase III (Effective 1 April 2021)

Businesses with aggregate turnover exceeding ₹50 crore were brought under the e-invoicing system through Notification No. 5/2021 – Central Tax.

Phase IV (Effective 1 April 2022)

The applicability expanded further to taxpayers with turnover exceeding ₹20 crore, as per Notification No. 1/2022 – Central Tax.

Phase V (Effective 1 October 2022)

The limit was reduced to ₹10 crore under Notification No. 17/2022 – Central Tax.

Phase VI (Effective 1 August 2023)

Currently, GST e-invoicing is mandatory for businesses with aggregate turnover exceeding ₹5 crore, as per Notification No. 10/2023 – Central Tax.

As of 2026, this ₹5 crore threshold continues to apply unless revised by the government.

What Is Included in Aggregate Annual Turnover (AATO)?

The total turnover of all GST registrations (GSTINs) under a single PAN throughout India is included in the aggregate annual turnover for the purposes of applying e-invoices. This implies that the total turnover of all these registrations will be taken into account when deciding whether e-invoicing is required if a business operates in numerous states and has multiple GSTINs.

Among the components of aggregate turnover are:

Taxable supplies

Exempt supplies

Exports of goods or services

• Inter-state supplies

It does not include inward supplies that are subject to GST and reverse charge.

Businesses cannot avoid compliance by dividing operations over several states because of this PAN-based computation.

When Does e-Invoicing Become Applicable?

The timing of applicability is another crucial component of compliance.

GST e-invoicing becomes required at the start of the following fiscal year if a taxpayer's total turnover surpasses the specified threshold in any given fiscal year.

For instance, a company must start using e-invoicing from April 1, 2025 (FY 2025–26) if its turnover exceeds ₹5 crore in FY 2024–2025.

On the other hand, e-invoicing is not required if a company's turnover was below the threshold the year before and stays below it.

Before compliance becomes mandatory, businesses have time to upgrade accounting software, prepare their systems, and align with IRP regulations thanks to this forward-looking approach.

How does GST e-invoice Works? Step-by-Step Explanation

A systematic workflow is used by the GST e-invoice system to guarantee invoice validation prior to tax reporting.

Invoice Creation in Business Software

The supplier starts the process by creating a tax invoice in their billing or ERP software. Mandatory information such the buyer's and supplier's GSTINs, invoice numbers, dates, HSN codes, taxable values, applicable GST rates, and the place of delivery are all included in this invoice. The invoice is not yet a legitimate electronic invoice at this point.

Conversion into Standard JSON Format

After that, the invoice data is transformed into the standard JSON structure that GSTN has specified. This standardised framework facilitates smooth connection with government portals and guarantees consistency across various accounting systems.

Uploading to the Invoice Registration Portal (IRP)

Using bulk upload tools, GST Suvidha Providers, or API connectivity, the JSON file is uploaded to the IRP. Data consistency and duplicate verification are among the validation checks carried out by the IRP.

Generation of Invoice Reference Number (IRN)

After validation, the IRP creates a distinct IRN using the supplier's GSTIN, invoice number, and fiscal year. The invoice's registration with the GST system is attested by the IRN. An invoice that needs to be e-invoiced is deemed invalid if it does not have an IRN.

QR Code Authentication

The IRP creates a digitally signed QR code with important invoice information in addition to the IRN. Authorities and purchasers can confirm the legitimacy of the invoice by scanning this QR code.

Auto-Population into GST System

The GST system receives the verified invoice data, and relevant data automatically appears in GSTR-1. To cut down on repetitive data entry, invoice details may, if applicable, also flow into the e-way bill site.

Issuance of Final Valid Invoice

The supplier sends the buyer the invoice following the creation of the IRN and QR code. It now has legal validity under GST law.

Important GST e-Invoice Rules in 2026

Compliance requirements around GST e-invoice have tightened over time.

30-Day Reporting Rule for ₹10 Crore+ Businesses

Businesses with an annual total revenue of more over ₹10 crore are required to submit invoices to the IRP within 30 days of the invoice date starting in April 2025. The invoice cannot be confirmed and IRN generation is blocked if it is not uploaded within this window.

This regulation discourages backdated reporting and strengthens real-time compliance.

No Backdated IRN Generation

Companies are unable to generate an IRN for invoices that are very old. Strong system controls lower the danger of tampering and guarantee prompt reporting.

Mandatory Authentication Measures

To protect invoice data and stop unauthorised access, enhanced security features, including two-factor authentication, have been put in place.

Benefits of GST e-Invoice for Businesses

GST e-invoicing has generated some operational benefits, despite the fact that its main purpose was to increase tax compliance.

Improved Accuracy in GST Reporting

Errors in GSTIN, tax computations, and invoice duplication are significantly decreased because invoice data is verified in real time. Reconciliation errors and errors in human entry are reduced when GST returns are filled in automatically.

Faster Input Tax Credit Processing

Buyers can more confidently claim input tax credit because invoices are reported centrally. Standardised reporting lowers disputes and fortifies the ITC chain.

Reduction in Fake Invoices

Making fraudulent bills is extremely difficult with the IRN and digitally signed QR code. This improves supply chain trust and strengthens the integrity of the GST system in India.

Seamless Integration with e-Way Bill System

Integration between e-way bill and e-invoice systems increases operational efficiency and minimises repeated data entry for businesses that deal with goods.

How Infinity Simplifies the Process of e-Invoicing for Cross-Border Payments?

Cross-border payment management and GST e-invoice compliance are connected for exporters, freelancers, agencies, and SaaS companies that work with clients around the world. Exports are zero-rated under GST, but if turnover over the limit, they are still regarded as reportable transactions under the e-invoicing framework.

It can become operationally hard to manage export invoices in addition to foreign inward remittances, currency rate reconciliation, LUT compliance, and filing GST returns. Reconciliation issues are frequently caused by gaps between the billed value and the actual foreign exchange amount.

By keeping organised transaction records and accelerating cross-border payment flows, Infinity makes the scenario simpler. GST reconciliation is made much simpler when invoice data and foreign currency receipts are properly aligned within a single financial workflow. Mismatches are reduced, and more seamless compliance reporting is supported by transparent conversion records and well-organised paperwork.

Having a structured cross-border payment infrastructure like Infinity indirectly improves e-invoice compliance and lessens the strain of manual reconciliation for companies that operate internationally, as GST compliance becomes more data-integrated in 2026.

Frequently Asked Questions (FAQ)

What is GST e-invoice?

A GST e-invoice is a tax invoice authenticated by the Invoice Registration Portal and assigned a unique IRN.

What is the GST e-invoice limit in 2026?

Businesses with aggregate annual turnover exceeding ₹5 crore must generate e-invoices for applicable transactions.

Is e-invoice required for B2C transactions?

No, GST e-invoicing primarily applies to B2B transactions and certain notified supplies.

What happens if an e-invoice is not generated?

If applicable and not generated, the invoice may be treated as invalid under GST law, and penalties may apply.

Is GST e-invoice applicable for exports?

Yes, exporters must generate e-invoices if they cross the turnover threshold and the supply qualifies under e-invoicing rules.

Can an e-invoice be cancelled?

Yes, it can be cancelled within the prescribed time limit on the IRP, subject to GST rules.

![9 Best Cross Border Payment Platforms in India [Based on Real User Reviews]](https://framerusercontent.com/images/ZOzvHCU1ezQxfPmG2hFSGdvRrWE.png?width=1536&height=1024)