Taxation & Compliance

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

Understanding FIRC is crucial if you are an exporter, freelancer, SaaS entrepreneur, consultant, or agency owner who receives payments from clients internationally. In recent years, India has tightened its regulations regarding international inward remittances, and documentation is essential for FEMA reporting, GST refunds, and audit procedures. The phrase "FIRC certificate" is commonly used in banking and tax conversations, regardless of whether you are exporting products or services. But do you actually need it, and what does it mean exactly?

This detailed guide provides a clear and organised explanation of every aspect of FIRC, including its entire form, meaning, importance, process, charges, GST implications, and how it differs from FIRA.

What is FIRC?

Foreign Inward Remittance Certificate is the full form of the FIRC. It is a formal document provided by an Indian Authorised Dealer (AD) bank that attests to the receipt of foreign money from outside the country via the appropriate banking channels.

To put it simply, a FIRC certificate verifies that your company has been paid by a foreign customer. The bank logs the inward transfer when a client from the US, UK, Europe, or any other nation transfers payments into your Indian bank account. Formal documentation of that transaction is provided by the FIRC.

India's foreign exchange laws, which are regulated by the Reserve Bank of India under the authority of the Foreign Exchange Management Act (FEMA), form the foundation of the FIRC concept. The country's balance of payments is affected by foreign exchange inflows, thus each remittance must be appropriately categorised and reported. That documentation ecosystem includes the FIRC.

What is an FIRC certificate?

A FIRC certificate is more than just an acknowledgement sheet. After confirming the inward remittance, your bank issues this organised and comprehensive document. The beneficiary's name, the remitter's information, the amount of foreign currency received, the equivalent Indian rupees credited, the conversion rate used, the date of transfer, and—above all—the purpose code linked to the transaction are all commonly included in the certificate.

Because it classifies the type of payment, the purpose code is essential. Payments for software services (P0802), consulting (S1006), exporting commodities (P1006), or professional services, for instance, all have separate codes. This classification helps authorities precisely track export proceeds and guarantees proper regulatory reporting.

These specifics make the FIRC an essential document for export paperwork, GST claims, audits, and compliance checks.

Why is FIRC important?

FIRC is more than just a bank certificate; it is important for export compliance, taxation, and regulatory reporting. Its significance can be understood in a number of ways:

1. Exporters' GST Refund Claims

Exports are considered zero-rated supply for exporters using a Letter of Undertaking (LUT). However, authorities need evidence that the payment was made in convertible foreign currency in order to grant a GST refund. Refund applications are strengthened and the likelihood of GST inspectors asking questions is decreased by the FIRC certificate, which serves as official proof that foreign currency has truly been realised in India.

2. FEMA and RBI Compliance

The Reserve Bank of India controls foreign exchange inflows into India in compliance with FEMA regulations. Export earnings have to be realised within the allotted time frames. FIRC assists in proving adherence to these deadlines and verifies that payment was made using approved banking channels.

3. Audit and Income Tax Scrutiny

Foreign receipts may be questioned by authorities during GST audits or income tax assessments. Sometimes it's not enough to just present a bank statement. Through the purpose code, a FIRC offers organised and verified evidence of inward remittance, including the type of transaction.

4. Export Documentation and Regulatory Reporting

By integrating with customs systems such as ICEGATE, FIRC data makes it easier for exporters of commodities to issue e-BRCs (Bank Realisation Certificates). It may become challenging to reconcile exports and payment receipts in the absence of appropriate remittance paperwork.

5. Proof of Export Income for Service Providers

SaaS founders, consultants, agencies, and freelancers frequently receive international payments. Particularly when interacting with banks, investors, compliance assessments, or regulatory checks, FIRC strengthens export income documentation.

Who needs an FIRC?

An FIRC may eventually be necessary for any Indian organisation or individual receiving foreign funds through approved banking methods. This comprises independent freelancers, IT firms, SaaS startups, consultants, digital agencies, and exporters of goods and services.

Electronic Bank Realisation Certificates (e-BRC) are made easier for goods exporters by the integration of FIRC data with customs reporting systems like ICEGATE. FIRC is still one of the key documents used by service exporters to show inward remittance.

Your international income is officially categorised as an export of services, even if you are a sole proprietor providing services to clients abroad. FIRC may be significant in GST or audit scenarios.

Difference between FIRC vs e-FIRC

In the past, physical FIRC certificates with an authorised signature and stamp were issued by banks on paper. Exporters had to physically visit the branch, make their requests, and pick up the certificate. This procedure was frequently tedious and involved a lot of paperwork. The system developed into electronic reporting over time.

These days, e-FIRC, a digitally created certificate, is issued by the majority of banks. Transparency is increased, and paperwork is decreased by using electronic means to capture and report the data to regulatory systems.

To facilitate smooth reconciliation, e-FIRC data is immediately linked with customs systems for goods exporters. e-FIRC is typically issued as a PDF document with digital authentication for service exporters.

What are the steps involved in receiving FIRC from the Bank?

It's not always easy to get a FIRC. After receiving the inward remittance, you have to make a separate request in many banks.

Once the international payment is credited to your account, the process usually starts. Depending on the type of export, the bank gives the transaction a purpose code. It is essential that your business activity be appropriately reflected in this purpose code. Later compliance issues may arise from an inaccurate classification.

You must ask your bank to issue the FIRC once the remittance has been credited. While some banks need a branch visit, others permit online applications. If you are exporting products, you might be required to submit your Import Export Code (IEC), a copy of the invoice, and a transaction reference number (such as SWIFT data).

The bank confirms the transaction information and makes sure it conforms with foreign exchange laws. The FIRC is issued after approval, typically in a few working days.

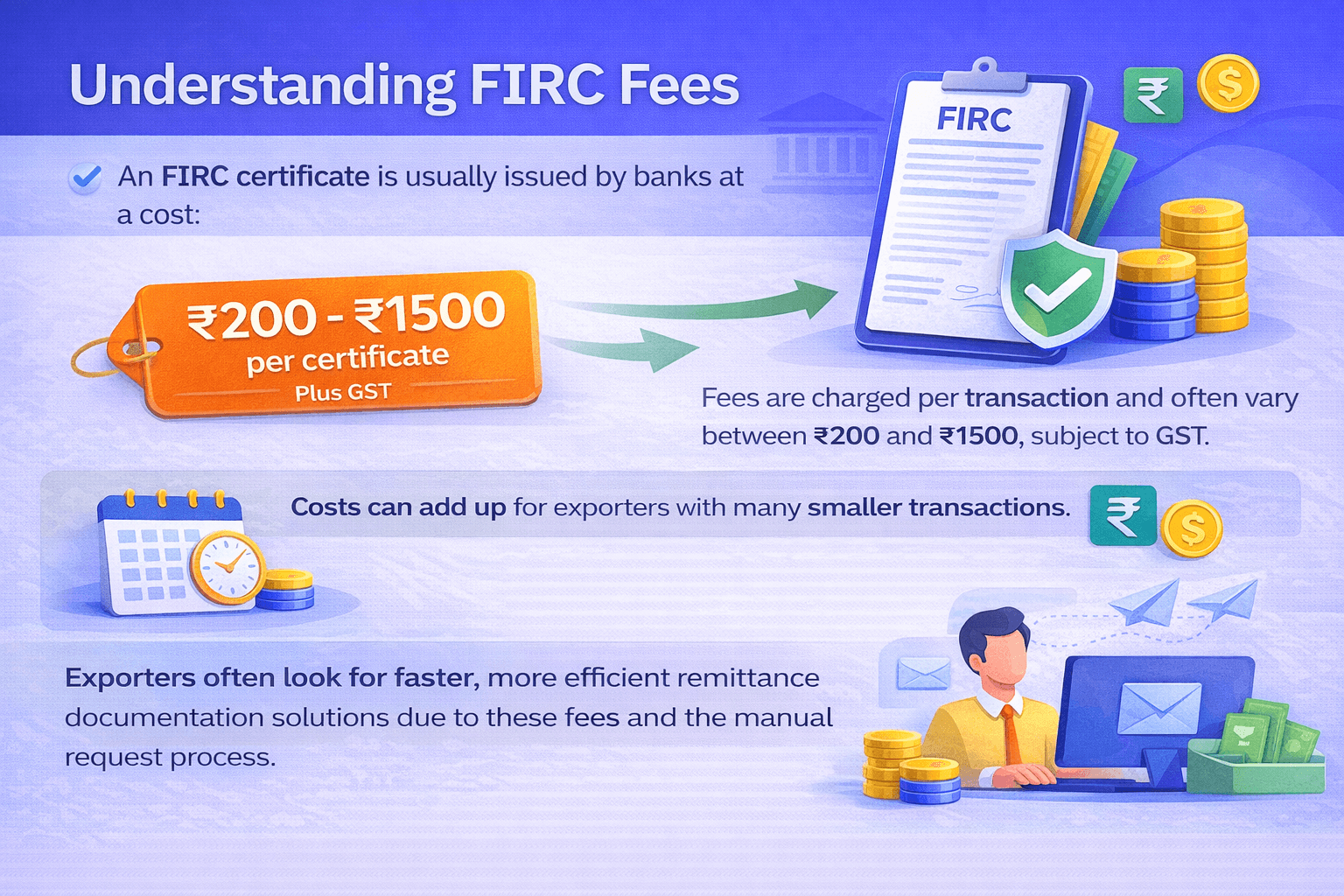

FIRC Charges: How much do banks charge?

An FIRC certificate is typically issued by banks at a cost. Depending on the bank, the fees can vary, but they usually fall between 200 and 1500 per certificate. These fees are typically subject to GST.

Usually, the fee is assessed on each transaction. This implies that you might have to pay for each FIRC separately if you receive several overseas payments. These fees could add up over time for companies that receive a lot of small-value transactions.

Many exporters search for more effective remittance documentation options due to these extra expenses and the manual request procedure.

FIRC vs FIRA: What’s the difference?

Particularly among freelance workers and service exporters, the terms FIRC and FIRA are frequently confused.

An Authorised Dealer (AD) bank would typically issue a FIRC (Foreign Inward Remittance Certificate), which is a formal banking document attesting to the receipt of foreign cash.

On the other hand, cross-border payment companies or fintech platforms typically issue FIRA (Foreign Inward Remittance Advice). It is frequently used by service exporters as evidence of foreign inward remittances and functions as a remittance confirmation document.

Although both certificates attest to the receipt of foreign payments, their issuer, format, and pricing structure are different.

Basis | FIRC | FIRA |

Full Form | Foreign Inward Remittance Certificate | Foreign Inward Remittance Advice |

Issued By | Authorised Dealer (AD) Bank | Fintech/payment platform |

Format | Formal stamped/digital certificate | Remittance advice document |

Charges | Usually ₹200–₹1500 per certificate | Often free or included |

Processing | Manual request required | Usually auto-generated |

Used For | GST refunds, compliance, audits | GST documentation (service exports), compliance |

Ideal For | Traditional exporters | Freelancers, SaaS founders, agencies |

Is FIRC mandatory?

In certain situations, FIRC is not always required. Depending on your export activities and whether you are requesting GST refunds, it may or may not be necessary.

Documentation connecting remittance to export filings becomes crucial if you are exporting items and requesting refunds. FIRC or similar electronic reporting is essential in these situations.

Alternative paperwork, such as FIRA, bank statements, and remittance advice, may be adequate for service exporters who are not requesting refunds. Formal documentation, however, improves your compliance position during audits or inspections.

Common Mistakes to Avoid While Applying for FIRC

Due to simple mistakes, many exporters experience delays in compliance. By being aware of these typical errors, you can avoid refund rejections and save time.

Choosing the wrong purpose code

Allowing the bank to assign the incorrect purpose code is one of the worst errors. Inaccurate classification of your export revenue—for instance, labelled as "personal remittance" rather than "export of services"—can lead to issues with FEMA and GST. After the credit, always check the purpose code right away.

Mismatch between the invoice and the remittance amount

Authorities may raise questions if the received amount is quite different from the invoice value because of bank fees, incomplete payments, or currency conversion issues. To support such discrepancies, keep accurate reconciliation documents.

Delays in Requesting FIRC

FIRC is not always generated automatically by banks. It may become more difficult to retrieve past data if you wait too long to make the request. Requesting documents as soon as possible after receipt is advised.

Not Keeping Up Appropriate Records

A lot of exporters only use bank statements. However, keeping track of contracts, invoices, remittance advice, and correspondence guarantees more efficient GST refund processing and audits.

Several Small Transactions Without Consolidation

Multiple FIRCs may be needed for frequent low-value payments, which would increase expenses and administrative work. An efficient billing cycle structure helps simplify documentation.

Conclusion

In India's export ecosystems, FIRC is essential. It guarantees adherence to FEMA regulations overseen by the Reserve Bank of India, supports GST refund claims, acts as documentation of foreign inward remittance, and strengthens your audit trail.

However, manual requests, paperwork, different fees for each transaction, and administrative follow-ups are frequently involved in the traditional FIRC issuance process through banks. This can become time-consuming for consultants, freelancers, agencies, and SaaS companies who receive regular overseas payments.

This is where the process is made simpler by modern cross-border platforms.

Infinity is designed especially for Indian professionals. Infinity automatically issues FIRA for each transaction, eliminating the need for typical bank-issued FIRC and facilitating quicker and easier international inward remittance documentation. Infinity reduces the operational load related to overseas payments with its simple forex conversion, lack of hidden FX markup, export-focused compliance support, and streamlined documentation workflows.

Selecting the appropriate payment partner can have a big impact on companies that are more concerned with growing internationally than with handling paperwork. It's crucial to fully understand FIRC, but it's far more important to make compliance simpler.

FAQs on FIRC

What is FIRC full form?

FIRC stands for Foreign Inward Remittance Certificate.

Is FIRC mandatory for freelancers?

Not always. It depends on whether you are claiming GST refunds and the specific documentation requirements applicable to your case.

How long does it take to get FIRC from a bank?

Typically 2–7 working days, depending on the bank’s internal process.

What is the difference between FIRC and BRC?

FIRC confirms receipt of foreign remittance. BRC (Bank Realisation Certificate) is issued for goods exporters after remittance is reported to customs.

Are banks allowed to charge for FIRC?

Yes, most banks charge a documentation fee per certificate.

Can FIRA be used instead of FIRC?

In many service export cases, FIRA is accepted as proof of foreign inward remittance, provided it contains complete transaction details.