Global payments

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

TL;DR

An overdraft (OD) is a type of banking facility that lets you take out more money than you have in your account, up to a certain amount. To help people and companies handle short-term cash flow shortfalls, banks provide overdraft services.

Only the amount used is subject to interest; the full limit is not. Depending on the type of overdraft and the customer's credit history, overdraft interest rates in India normally vary from 7% to 24% annually.

Salaried people, independent contractors, and companies that want rapid access to short-term funding frequently use the facility.

Introduction

Both individuals and businesses may find it difficult to manage their financial flow. Unexpected expenses can occur anytime even before the anticipated income is received. For instance, a company may have to pay suppliers before getting paid by clients, or a salaried worker may have to pay an emergency bill before their next pay cheque is sent.

Banks provide a range of loan facilities that offer short-term financial assistance in order to handle such circumstances. The overdraft feature, which enables account holders to take out more money than they currently have in their bank account, is one such popular choice. This is known as overdraft in banking.

Businesses, exporters, and small firms in India frequently use overdraft arrangements to handle their working capital needs. The Reserve Bank of India reports that over the past ten years, bank lending to the MSME sector has expanded gradually as companies rely on short-term credit instruments, including cash credit and overdrafts, to manage liquidity.

Businesses and people can make better financial decisions by being aware of overdraft fees, how they operate, and when they should be used.

What Is Overdraft in Banking?

An overdraft is a credit facility provided by banks that allows customers to withdraw funds from their accounts even when the account balance is insufficient. The bank essentially lends money to the customer up to a specified limit.

An overdraft in banking functions more like a flexible credit line than a typical loans, which pay out a set of amount up front. Consumers are able to withdraw money as needed and return it whenever they want within the predetermined time frame.

Overdraft services are especially helpful for handling short-term financial needs because of this flexibility.

Overdraft Meaning

To put it simply, an overdraft lets you spend more money than you have in your bank account right now.

Assume, for instance, that your bank has authorised an overdraft limit of ₹50,000 and your account balance is ₹10,000. In that scenario, your total withdrawal limit is ₹60,000 (₹10,000 balance plus ₹50,000 overdraft limit).

But just the amount borrowed from the bank—not the whole overdraft limit—will be subject to interest.

Overdraft Full Form

In banking terminology, overdraft is commonly referred to as OD. The term OD is frequently used in business banking and corporate finance.

Depending on the customer's creditworthiness and profile, banks frequently offer OD accounts connected to current accounts, savings accounts, or salary accounts.

Which Is Better: Cash Credit (CC) or Overdraft (OD)?

Banks provide short-term lending options like Cash Credit (CC) and Overdraft (OD) to assist companies in managing their cash flow. The primary difference is in their application.

Cash credit is typically given to companies in exchange for assets like inventory or receivables, and it is mostly utilised for ongoing working capital requirements. Conversely, an overdraft permits people or companies to take out more money than what is available in their bank account, up to a predetermined limit.

Overdrafts are more appropriate for short-term or infrequent liquidity demands, whereas cash credit is generally preferable for companies that need ongoing working capital. The Reserve Bank of India oversees both facilities, which only impose interest on the amount utilised rather than the total credit.

How Does an Overdraft Facility Work?

Customers can utilise an overdraft facility anytime they need more cash because it functions as a revolving credit line.

Step 1: Bank Approves an Overdraft Limit

The bank must first approve the customer's overdraft limit. A number of variables, including income level, business turnover, credit history, and collateral (if necessary), are taken into consideration when determining this limit.

For instance, an overdraft limit of ₹1 lakh may be granted to a salaried person, whereas a firm may be granted a significantly higher amount based on its financial profile.

Step 2: Customer Withdraws Beyond Account Balance

The customer can take out more money than their available account balance once the overdraft feature is enabled.

You can make this withdrawal by:

ATM transactions

online banking transfers

cheques

debit card payments

The bank automatically records the amount used under the overdraft limit.

Step 3: Interest Is Charged Only on the Used Amount

The fact that interest is charged only on the amount utilised rather than the full credit limit is one of the main benefits of an overdraft.

For instance, interest will only be calculated on ₹20,000 if your overdraft limit is ₹1 lakh but you only take out ₹20,000.

Step 4: Repayment Reduces Interest

The overdraft amount may be repaid at any moment by customers. The interest computation decreases as soon as the borrowed sum is paid back.

Overdraft facilities are appropriate for short-term financial needs because of their flexibility.

Types of Overdraft Accounts

Depending on the customer's financial profile and the availability of collateral, banks offer a variety of overdraft possibilities.

Secured Overdraft

A secured overdraft is made possible by collateral like shares, real estate, insurance policies, or fixed deposits.

For instance, overdrafts against fixed deposits are provided by numerous institutions. The overdraft limit in these situations is often between 75% and 90% of the FD value.

Because the bank has collateral security, interest rates on this kind of overdraft are usually lower.

Unsecured Overdraft

Collateral is not required for unsecured overdrafts. Customers with solid credit records or steady salaries are typically given this.

Unsecured overdraft facilities connected to salary accounts are frequently provided to salaried workers.

However, interest rates on unsecured overdrafts are typically higher due to the lack of collateral.

Overdraft for Businesses

Businesses frequently use overdraft facilities for working capital management.

For example, companies may use overdrafts to:

pay suppliers

manage payroll expenses

purchase inventory

cover operational costs

Overdrafts linked to current accounts are commonly used by SMEs and exporters.

Overdraft Interest Rates and Charges

Overdraft facilities have some expenses, regardless of their convenience. Customers can utilise the facilities properly if they are aware of these fees.

Interest Rates

Overdraft interest rates vary depending on the bank, type of overdraft, and customer profile.

Typical ranges in India include:

OD against fixed deposit: 7% – 9% per year

Business overdraft: 10% – 18% per year

Unsecured overdraft: 12% – 24% per year

These rates may change depending on market conditions and bank policies.

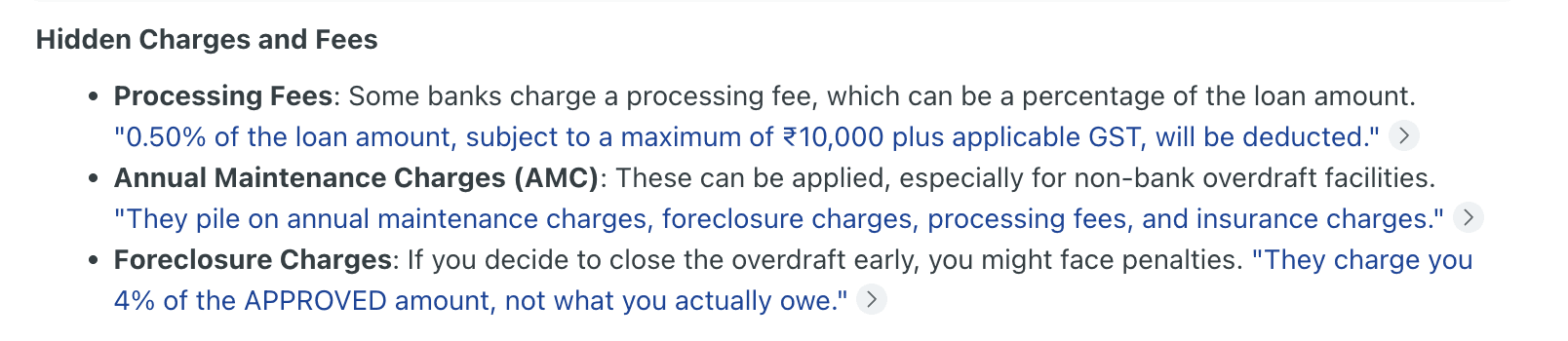

Processing Fees

When authorising an overdraft facility, banks frequently impose a processing fee.

Usually, this charge is between 0.5% and 2% of the authorised overdraft amount.

Renewal Charges

Overdrafts for businesses typically need to be renewed every year. Banks examine the borrower's financial situation during this procedure and may change the overdraft limit.

Depending on the bank's policies, renewal fees can also be applicable.

Penalty Charges

Banks may impose additional fees or penalty interest if a customer exceeds the authorised overdraft limit.

Therefore, customers should keep a close eye on how they use their overdraft.

Source: Reddit

Overdraft vs Loan: What’s the Difference?

Although overdrafts and loans both provide access to credit, they work very differently.

Feature | Overdraft | Loan |

Credit Type | Flexible credit line | Fixed loan amount |

Interest Charged | Only on amount used | Entire loan amount |

Repayment | Flexible | Fixed EMI schedule |

Usage | Short-term needs | Long-term expenses |

Overdrafts are typically better for managing short-term cash flow gaps, while loans are more suitable for large planned expenses.

Common Use Cases of Overdraft (With Real-Life Examples)

In many real-world financial scenarios where short-term cash are needed, overdraft facilities are utilised.

Managing Cash Flow for Businesses

Time gaps between receiving payments and paying suppliers are a common problem for small and medium-sized enterprises.

For instance, an exporter might ship products to a customer abroad and get paid after a few weeks. The company might use an overdraft facility to pay staff or buy supplies during this time. This keeps everything running smoothly without interfering with cash flow.

Handling Emergency Expenses

In times of financial emergency, people may utilise overdraft capabilities.

For example, if someone has only ₹20,000 in their account but an unforeseen medical bill of ₹50,000, the overdraft feature enables them to pay the entire amount right away.

The loan amount can be paid back when the next salary comes in.

Short-Term Working Capital

Overdraft facilities are sometimes used by retail enterprises during periods of high sales.

For instance, a clothes business getting ready for the holiday season can use an overdraft to buy more stock before demand from customers rises. This enables the company to take full advantage of sales possibilities without having to wait for financial reserves.

Overdraft Limits in Indian Banks

Depending on a number of variables, including the customer's income level, credit history, business turnover, and whether the overdraft is secured or unsecured, Indian banks' overdraft limits can vary greatly. Although the fundamental idea of an overdraft is the same for all banks, each customer's actual limit is decided after the bank conducts a financial evaluation.

Banks typically provide overdraft facilities with varying limit structures to corporations, self-employed professionals, and salaried individuals.

Overdraft Limits for Salaried Individuals

Overdraft services connected to salary accounts are offered by numerous Indian banks. These overdrafts are typically unsecured and are granted in accordance with the customer's credit score, pay, and job stability.

Overdraft restrictions for salaried individuals often range from ₹50,000 to ₹5 lakh, depending on their banking relationship and salary.

For instance, some banks provide overdrafts equal to two to three months' worth of the customer's pay. An overdraft limit of approximately ₹1.5 lakh to ₹2.5 lakh may be approved by the bank for an individual earning ₹80,000 per month.

Before the following pay cycle, this kind of overdraft is frequently utilised to handle urgent or short-term obligations.

Overdraft Limits for Businesses

Overdraft facilities are often used by businesses, particularly small and medium-sized organisations (SMEs), to manage working capital requirements. Usually connected to current accounts, these overdrafts are set up according to the company's creditworthiness, turnover, and financial performance.

Overdraft limits for businesses typically start at ₹5 lakh and can go up to ₹5 crore or more, depending on the company's size and financial stability.

For instance, an overdraft limit may be granted to a manufacturing company with a yearly turnover of ₹10 crore, enabling it to pay for short-term operational costs like inventory purchases, staff salaries, and supplier payments.

These restrictions are reviewed by banks on a regular basis, and depending on the company's financial situation, they may be increased or decreased.

Overdraft Against Fixed Deposits

An overdraft against a fixed deposit (FD) is one of the most popular and readily authorised overdraft options in India. Banks view this as a low-risk lending option because the FD serves as collateral.

The majority of banks permit overdrafts of up to 75% to 90% of the value of fixed deposits.

For instance, the bank might let someone use an overdraft of between ₹3.75 lakh and ₹4.5 lakh if they have a fixed deposit of ₹5 lakh.

Because the loan is fully secured, interest rates on overdrafts against fixed deposits are often lower.

Factors That Influence Overdraft Limits

Before approving an overdraft facility or setting a limit, banks consider a number of variables. Among the important factors are:

Income level or business turnover

Credit score and repayment history

Existing relationship with the bank

Availability of collateral or security

Type of bank account (salary, savings, or current account)

In order to maintain secure and careful lending practices, financial institutions in India are subject to regulations set by the Reserve Bank of India.

Overdraft restrictions are rarely set and may vary from customer to customer due to these variable factors. Higher limits and better interest rates are frequently granted to clients with solid credit histories and established banking connections.

Common Mistakes to Avoid When Using Overdraft

Overdraft facilities are useful, but they must be used wisely to prevent unnecessary financial strain.

Using Overdraft for Long-Term Expenses

The purpose of overdrafts is to provide short-term liquidity. High interest rates may result from using them for long-term costs like financing significant investments or purchasing a car.

Ignoring Interest Accumulation

The fact that overdraft interest accumulates on the borrowed amount every day is often overlooked by users. The total amount of interest paid can rise significantly if repayment is delayed.

Exceeding the Approved Limit

Banks may levy extra fees or penalty interest if the overdraft limit is exceeded. Monitoring consumption and adhering to the authorised limit are important.

Not Repaying Early

Early repayment may significantly decrease interest expenses because overdraft interest is based on the outstanding amount.

How Infinity Helps Businesses Manage Global Payments

While overdraft facilities help organisations in managing their short-term liquidity demands, businesses dealing with foreign clients frequently encounter a distinct issue: delays in receiving cross-border payments.

Conventional bank-to-bank overseas transfers can include various intermediary fees and take several days to process. For exporters, freelancers and businesses, this may result in brief cash flow gaps.

By giving companies a streamlined method of accepting international payments, Infinity helps in streamlining this procedure.

Businesses may manage international payments more effectively, obtain greater clarity on transaction fees, and reduce the time to 24-hours settlement to receive international payments by avoiding complicated banking procedures.

A cutting-edge financial platform like Infinity can greatly enhance international payment management and cash flow visibility for businesses that frequently deal with foreign clients.

Conclusion

Overdraft facilities are a useful financial tool that allows individuals and businesses to access short-term credit when needed. By enabling account holders to withdraw funds beyond their available balance, overdrafts help bridge temporary cash flow gaps.

In India, they are frequently used for things like handling emergencies, controlling business expenses, and paying for immediate operating expenses.

Overdrafts, however, should be utilised wisely and paid back as soon as possible to reduce expenses because they come with fees and interest.

FAQ on Overdraft in India

What is an overdraft in banking, with an example?

An overdraft allows you to withdraw more money than what is available in your bank account. For example, if your balance is ₹10,000 and your overdraft limit is ₹50,000, you can withdraw up to ₹60,000.

What is the full form of OD in banking?

OD in banking stands for Overdraft.

What is the interest rate for overdraft in India?

Overdraft interest rates typically range between 7% and 24% per year, depending on the bank and type of overdraft.

Is overdraft better than a personal loan?

Overdrafts are better for short-term financial needs because interest is charged only on the amount used. Personal loans are better for long-term planned expenses.

Can salaried employees get overdraft facilities?

Yes, many banks offer overdraft facilities linked to salary accounts for eligible employees.

What happens if the overdraft limit is exceeded?

If the overdraft limit is exceeded, banks may charge penalty interest or additional fees.

![9 Best Cross Border Payment Platforms in India [Based on Real User Reviews]](https://framerusercontent.com/images/ZOzvHCU1ezQxfPmG2hFSGdvRrWE.png?width=1536&height=1024)