Global payments

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

Dealing with banks to receive international payments can be frustrating. From high forex markups to hidden bank charges and slow processing times, freelancers and small businesses often end up losing both money and time. Adding compliance requirements like FIRC (Foreign Inward Remittance Certificate) can feel overwhelming.

This guide lists the top 5 Indian banks for receiving international payments.

What to Look for in a Bank for Receiving International Payments?

Almost all Indian banks follow the same process for receiving international payments—they accept the foreign currency, convert it into INR, and then credit it to your account.

So, how do you decide which bank is actually the best?

Check how much they charge in hidden fees, how competitive their exchange rates are, how fast the money reaches you, and how easily you can track the transaction. Let’s break it down.

FX markup (Hidden costs in exchange rate spreads)

When you receive money in USD, EUR, or any foreign currency, your bank converts it to INR. But they don’t use the rate you see on Google. In fact, banks add a markup, usually around 1.5% to 3%, sometimes more. This is called the FX spread, and it’s how banks quietly profit from your payments.

Hence, always ask your bank, “What’s your exact FX markup?” and compare with other banks or platforms.

SWIFT/Transaction fees

Banks charge a fee for processing international wire transfers through the SWIFT network. It is usually between ₹500 to ₹1,500 per transaction, depending on the currency and the amount converted.

Sometimes, intermediary banks also deduct fees, usually without warning. You should check both the sending and receiving fees so you know the total deductions.

Processing time

Ask how soon your money will arrive in your local bank account. Private banks in India usually process international payments within 1–3 business days, while public sector banks may take up to 5 days.

Ease of getting FIRC (for Tax & Legal Compliance)

A Foreign Inward Remittance Certificate (FIRC) is your proof that money came from abroad for legitimate purposes. It’s essential for tax filings, GST exemption on foreign exchange (especially for exporters), and legal compliance.

Some banks (like ICICI and HDFC) offer online downloadable FIRCs, while others still rely on manual, time-consuming processes.

Customer support & online banking features

Choose banks that offer dedicated helplines or chat support to enquire about payment processes and delays.

RBI Compliance

Make sure that the bank complies with FEMA and the Liberalised Remittance Scheme (LRS) Rules.

Oversight of payment aggregators

Under the new Payment Aggregator–Cross Border (PA-CB) framework, all banks and non-banks handling online cross-border payments must be registered and authorised by the RBI.

The earlier OPGSP model has been phased out. Each transaction is capped at ₹25 lakh, adding a layer of risk control and traceability.

Foreign currency accounts for exporters, with tight controls

RBI now allows resident exporters to open overseas foreign currency accounts specifically for trade settlements.

However, any funds received (like export payments) must be repatriated to India within 1 month, making timely routing through compliant Indian banks even more important.

5 Best Banks to Receive International Payments in India

Here's a detailed comparison of the five most efficient banks to receive money transfers from abroad.:

1. HDFC Bank

HDFC Bank allows foreign remittances in 19–22 major currencies, including USD, EUR, GBP, CAD, AUD, SGD, AED, etc. The bank processes international payments through SWIFT and correspondent bank tie-ups.

Key features:

Automatic currency conversion: The bank automatically converts foreign funds INR at the bank’s telegraphic transfer (TT) selling rate once the amount is credited.

Charges & fees: HDFC charges a ₹500–750 inward remittance fee per transaction. Additional deductions may occur via intermediary (correspondent) banks.

Processing time: You get the payment in your bank account within 72 hours.

FX markup: Expect a forex markup of about 2-3.5% of the transaction amount.

Cheque collection: It accepts foreign currency cheques and demand drafts for 14 currencies in savings or current accounts.

Pros and cons of using HDFC Bank for receiving international payments

Pros | Cons |

Auto conversion at credit, no manual forex conversion needed | FIRC fee of ₹200 + GST per certificate, plus ACE and wire transfer charges |

Easy integration with global platforms | Additional wire transfer fees |

Clear fee structure; fixed markup and flat charges provide predictability | Customer support can be delayed at times |

FIRC can be accessed digitally | No negotiation flexibility for small accounts |

A Reddit user shared their experience with HDFC for foreign payments

Source: Reddit Post

2. ICICI Bank

ICICI Bank is more suitable for export firms and mid-size agencies to receive international payments. If you’re an exporter, agency, or business with high international turnover and your monthly remittances are on the higher side, ICICI offers more personalised service and slightly better forex rates than most.

Key features:

Payment processing time: International wire transfers typically take 1–2 working days to process and for the funds to reflect in your account.

High-value transfers: ICICI’s Money2India app allows remittances up to $300,000 in a single transaction—ideal for large payments.

Personalised support: Offers dedicated relationship managers for high-volume clients, helping resolve forex and compliance issues faster.

FIRC availability: Foreign Inward Remittance Certificates (FIRCs) can be conveniently downloaded online.

Instant credit feature: ICICI is among the few banks in Asia‑Pacific offering SWIFT GPI Instant for inbound remittances up to ₹2 lakh, instantly credited via IMPS.

Pros and cons of using ICICI Bank for international payments

Pros | Cons |

No transfer fees for high-value remittances | Higher forex markup (3.5%) |

Exchange rates improve with higher transfer amounts—a tiered structure that rewards bulk remittance | Additional wire transfer fees, exchange rate markups, and fees from intermediary banks |

Solid online banking tools | Hidden fees may not always be disclosed upfront |

FIRC can be accessed digitally | Setup might take longer |

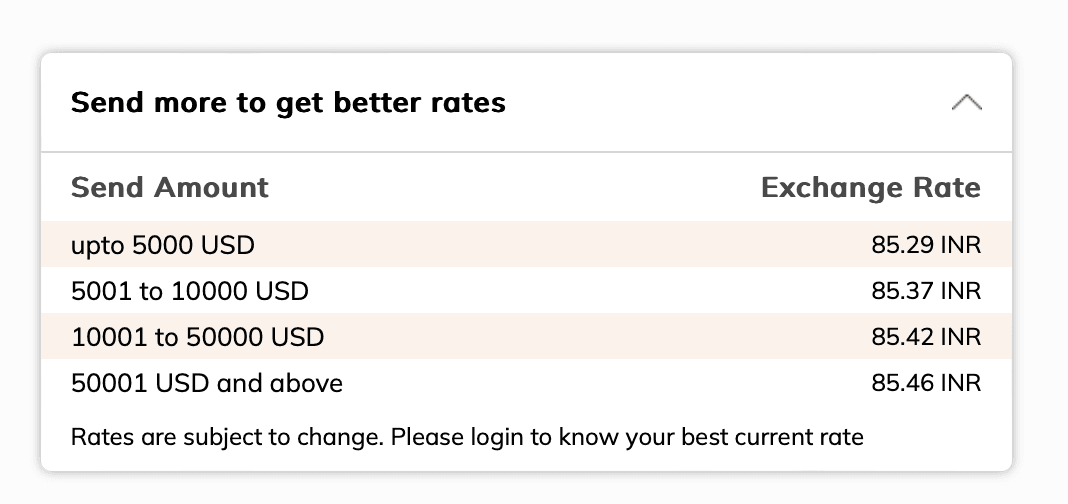

ICICI Bank’s conversion rate for converting USD to INR

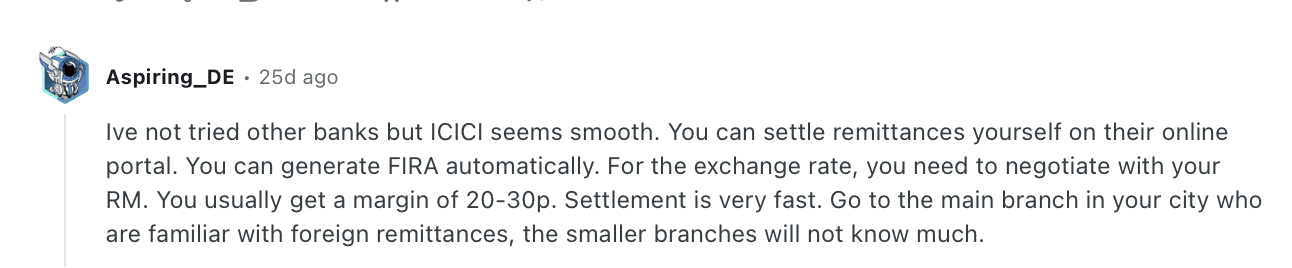

Here’s what a Reddit user says about receiving foreign payments through ICICI Bank:

Source: Reddit Post

3. Axis Bank

Axis Bank has a startup-friendly approach. If you’re just setting up your global payment process, you can use this bank for better transparency.

Key features:

Processing time: Internet/mobile banking takes 2-5 working days and branch transfers take 3-5 working days.

Forex markup: FX markup is around 3.5%.

Tracking feature: The Axis mobile app lets you track inbound remittances in real time.

24/7 USD settlement: 24/7 real-time USD settlement in partnership with J.P. Morgan’s Kinexys platform, enabling commercial clients to send or receive USD payments at any hour, all year round.

FIRC availability: FIRCs are available, but you’ll need to request them manually (email or branch).

Pros and cons of using Axis Bank for international payments

Pros | Cons |

Transparent fee structure with no onboarding or processing charges via OIRM | Higher forex markup (3.5%) |

Real-time tracking of inbound funds with instant rate booking and split credit capabilities | FIRCs require manual requests, which can cause delays |

Reliable for regular, smaller payments | Some hidden charges may apply via intermediary banks for SWIFT transfers |

This is what a user says about using Axis Bank for international payments:

Source: Reddit Post

4. Indian Overseas Bank (IOB)

Indian Overseas Bank offers a better foreign exchange rate compared to other Indian banks. This makes it attractive for exporters or freelancers receiving frequent foreign inward remittances.

Key features:

Top-tier exchange rates: It often offers ₹0.50–₹1 higher INR/USD TT buying rates in India than private banks on mid-market rates.

Automated inward remittances: Funds typically clear within 24–48 hours once FEMA declaration & purpose codes are submitted.

Low flat charges: Nominal service fees (₹500 + GST) and fixed SWIFT charges make costs predictable and transparent.

Convenient NRE/NRO/FCNR accounts: Offers full repatriability of foreign earnings with tax‑exempt status on NRE interest.

UPI-enabled inbound remittances: Supports IMPS/NEFT/RTGS and UPI cross-border transactions via NRE/NRO accounts.

Pros and cons of using IndusInd Bank for international payments:

Pros | Cons |

Excellent for regular forex clients— branches and managers often offer negotiation room | Inward remittances may take 2–3 days due to manual checks |

Sends FIRC/e‑FIRC post inward remittances as per RBI norms | Several users reported needing in‑branch visits for FEMA forms and documentation |

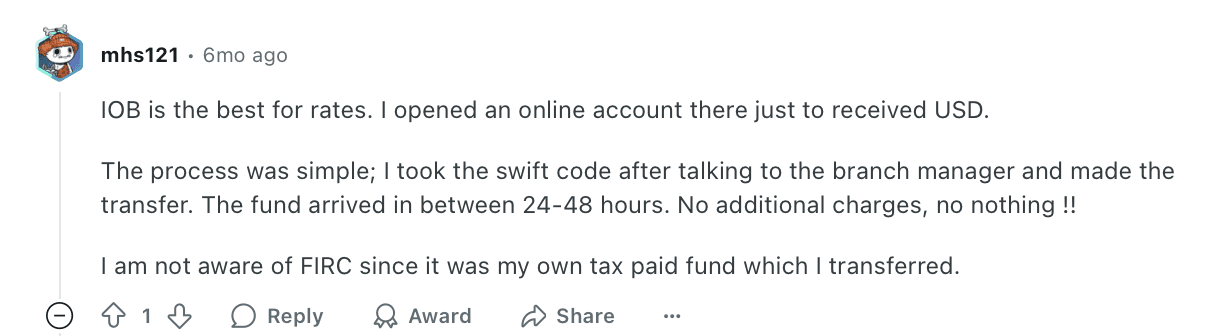

Here’s what a Reddit user says about receiving foreign payments through IOB Bank:

Source: Reddit Post

5. State Bank of India (SBI)

SBI Bank has a wide branch network and low service fees. It is suitable especially for exporters handling large, less frequent payments.

Key features:

Supported platforms: It supports SWIFT transfers and PayPal integration.

Service fees and FX rates: Service fees are low, and FX rates are close to the RBI’s reference rate.

Processing time: Processing time can be 3–5 business days, slower than private banks.

FIRC availability: FIRC is handled manually and may require multiple follow-ups.

Pros and cons of using SBI Bank for international payments

Pros | Cons |

Low service fees (often ₹500–₹1,000 per transaction) | Slower processing times |

Good for large, infrequent payments. | Some users say that the mobile banking app can be more intuitive |

Public sector trust and stability | FIRA process can be tedious |

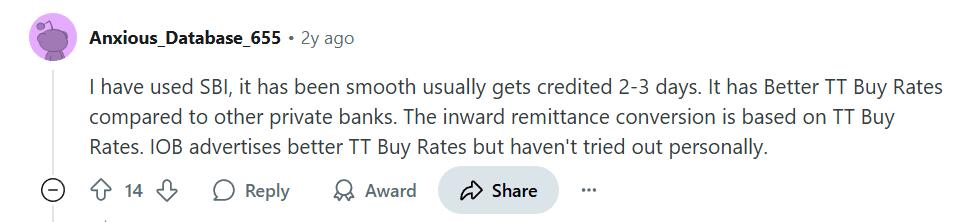

Here’s what a Reddit user says about receiving international payments through SBI Bank:

Source: Reddit Post

Pro Tips for Receiving International Payments via Banks

Now, let’s see some tips to receive international money transfers smoothly:

Receive payment in foreign currency: You’ll usually get a much better rate if you convert the amount from foreign currency to INR.

Always request an FIRC: Request a FIRC every single time, even if the amount seems small. It’s essential for tax filing, GST refunds, or showing proof of export income later.

Negotiate your forex rates: If you receive large or regular payments, talk to your Relationship Manager (RM). Even a 0.5% difference in rates can save you thousands over time.

Use a business account instead of a personal one: You’ll get higher transaction limits and smoother handling of international remittances in your current account.

Track exchange rates regularly: Check online platforms like Currency Converter for FX rates and request the payment from the client when the conversion rates are favourable.

Alternative to Banks for Receiving International Payments: Infinity

Banks often have hidden charges, delayed payments, and slow customer support. Infinity takes a simpler and more transparent approach.

What is Infinity?

Infinity is a modern international payment platform designed specifically for freelancers, creators, and SMBs in India.

Here’s what makes Infinity better than banks for receiving international payments in India:

No/Minimal FX markup: Infinity offers live FX rates with zero markup, so you get more of your hard-earned money.

Transparent, flat fees: With Infinity, you don’t get any mystery charges. Just a simple, flat 0.5% transaction fee on all foreign payments.

Faster transfers: While banks can take 2–5 days, Infinity typically processes your payments in under 24 hours.

FIRC support: Do you need proof for tax or GST purposes? Infinity automatically provides FIRC documentation, saving you the follow-up emails and branch visits.

Multi-currency Support: Infinity offers multi-currency accounts so you can easily receive payments in USD, GBP, EUR, and AUD. This makes it easy to collect payments from clients anywhere in the world.

Platform integration: Infinity works smoothly with platforms like Upwork, Fiverr, Stripe, and more, making your global workflow even easier.

Feature | Infinity | Traditional Banks (ICICI, Axis, etc.) |

Processing Time | Within minutes to 1 working day | 1–5 working days, depending on the method |

FX Markup | Zero FX markup | Higher (typically 2.5–3.5% or more) |

FIRC Certificates | Auto-generated and downloadable | Available, but often need manual requests |

User Experience | Fully digital onboarding, intuitive UI | Traditional often requires branch visits for issues |

Remittance Tracking | Real-time updates on app/web | Some banks provide tracking via ma obile app |

Customer Support | Dedicated support via chat and email | Relationship managers for high-volume clients only |

Freelancer/SMB Friendliness | Designed for freelancers & SMBs | Primarily focused on exporters, corporates, and NRIs |

Ease of Setup | Fast online KYC and activation | May involve paperwork and in-person verification |

Choose Infinity over Traditional Banks

Banks often come with unexplained deductions, slow settlements, and unclear FX rates. And traditional banks just weren’t built with freelancers or small businesses in mind.

Infinity was built to fix exactly that problem.

It’s built for people like you. Freelancers, creators, consultants, and business owners who work globally need a payment system that actually works for them. With faster transfers, real-time tracking, clearer fees, and no hidden FX charges, Infinity removes the usual stress from international payments.

Sign up for Infinity today!

FAQs

1. Which is the best Indian bank to receive international payments?

HDFC and ICICI Bank are popular choices for international money transfers due to their online banking support and faster processing time.

2. What is FIRC, and how can you get it?

FIRC (Foreign Inward Remittance Certificate) is an official document issued by banks to confirm that you've received a foreign payment in India. You have to request it manually. Platforms like Infinity provide automated FIRC support with every withdrawal at no extra cost.

3. Which bank offers the best forex rates?

IOB offers the best forex rates. However, you should check the transaction charges.

4. Can I use a savings account for international payments?

Yes, you can receive payments into a regular savings account via SWIFT transfers. However, business accounts may offer higher limits and better support.

5. How long does it take to process international payments?

Indian banks usually process international payments within 2 to 5 business days. It depends on the sending country, bank holidays, and intermediary banks involved.