Taxation & Compliance

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

TL;DR

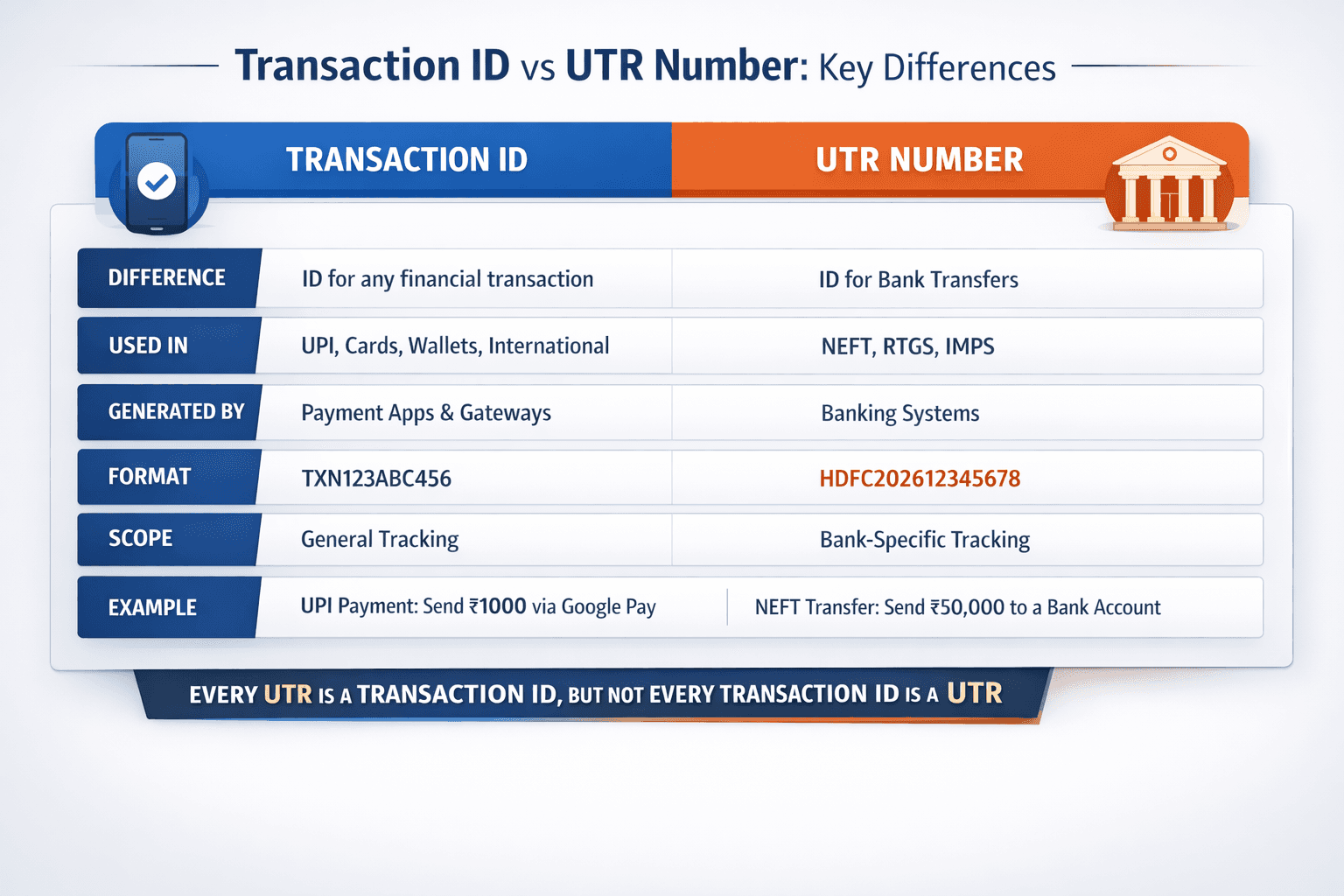

Every financial transaction, regardless of the mode of payment—UPI, card payments, wallets, or foreign transfers—is given a unique identification known as a transaction ID. On the other hand, a particular kind of Transaction ID used only in bank-to-bank transactions like NEFT, RTGS, and IMPS is called a UTR (Unique Transaction Reference) number.

To put it simply, not every Transaction ID is a UTR, but every UTR is a Transaction ID. When tracking payments, settling disputes, or corresponding with banks and payment platforms, it's important to understand this difference.

Introduction

Over the past few years, India's digital payment landscape has swiftly changed. Millions of transactions are handled every second across various platforms due to the growth of UPI, real-time transfers, and international payment platforms.

However, a structured system that guarantees each transaction is precisely tracked, confirmed, and recorded lies behind this speed and convenience. Even a small malfunction or delay could cause trouble for both users and financial institutions in the absence of such a system.

Transaction IDs and UTR numbers are examples of unique identifiers that are crucial in this situation.

These two terms could appear to be interchangeable at first. When interacting with banks or customer service, many users misuse them because they believe they are the same thing. However, this misunderstanding may result in miscommunication with financial institutions or even delays in resolving payment-related difficulties.

It is not only a technical matter to understand the difference between a Transaction ID and a UTR number; it is also a practical requirement. Understanding how these identifiers operate provides you with more control over your finances, whether you're a firm handling big transactions, a freelancer receiving international payments, or an individual making everyday payments.

What Is a Transaction ID?

Each time a financial transaction occurs, a unique alphanumeric identifier known as a Transaction ID is created. It serves as a digital reference that enables the system to recognise, monitor, and confirm that particular transaction among millions of ongoing ones.

The system assigns a Transaction ID as soon as you start a payment, whether you are using a payment gateway, sending money via a UPI app, or making an online card payment. This ID is always linked to that transaction and can be used at any time to verify its progress or fix problems.

The Transaction ID, for example, enables you to confirm whether a payment made via a UPI app was successful or is still waiting. In the same way, it assists banks and retailers in handling refunds and payment reconciliation in card transactions. It guarantees reliable tracking of payments travelling between nations in international transfers.

A Transaction ID essentially functions as a digital fingerprint, guaranteeing total traceability and transparency since no two transactions can ever have the same one.

What does a Transaction ID look like?

The format of a Transaction ID varies depending on the platform you are using. There is no single universal format, but here are some common examples:

UPI Transaction ID:

231456789012Card Payment ID:

TXN9F8D7C6B5AWallet Transaction ID:

PAY123456789XYZ

These IDs are usually a mix of numbers and letters, and they are designed to be unique for every transaction.

Read more: What is Transaction ID?

What Is a UTR Number?

One particular kind of Transaction ID used in the banking system is called a UTR number, or Unique Transaction Reference number. It is produced when money is moved between banks using RTGS, IMPS, or NEFT.

A UTR number is exclusively issued by banking systems, in contrast to standard Transaction IDs, which can be generated by different payment platforms. Because of this, it is especially crucial for transactions involving the transfer of money between banks.

Both the sending and receiving banks use the UTR number that is assigned to a bank transfer when it is initiated to monitor its progress. The UTR number becomes the main point of reference for any delays, failures, or errors.

The structured nature of UTR numbers is another important feature. It usually contains information like the bank code, transaction date, and a distinct sequence number, though the precise structure may differ between banks. Banks can find and handle transactions in their systems more rapidly due to this structure.

Practically speaking, the UTR number becomes the most crucial piece of information you need to trace or handle a bank transfer, particularly one involving a substantial amount of money.

What does a UTR number look like?

UTR numbers follow a more structured format compared to general Transaction IDs. While the exact format can vary between banks, they typically include a combination of bank codes, dates, and unique reference numbers.

Here are some examples:

HDFC Bank UTR:

HDFC202612345678SBI UTR:

SBIN202598765432ICICI UTR:

ICICR5202301234567

These formats help banks identify the origin, date, and sequence of the transaction within their systems.

Read more: What is UTR number?

Transaction ID vs UTR Number: Key Difference

Despite having the same basic function of identifying transactions, Transaction IDs and UTR numbers have rather different applications.

All kinds of financial transactions on different platforms are covered under the general term "transaction ID." Payment apps, gateways, banks, and even global systems produce it. A UTR number, on the other hand, is more specialised and is only utilised for interbank transfers within banking channels.

When you examine how these indicators are applied in actual situations, the difference becomes more evident. For example, when you use a UPI app to make a payment, the system creates a Transaction ID that you may use to follow the payment. On the other hand, if you send money via RTGS or NEFT, the bank creates a UTR number that acts as the transaction's formal reference.

The way these IDs are used in problem solving is another significant difference. When handling app-based transactions, payment systems usually want a Transaction ID, but banks need a UTR number when looking into transfer-related problems.

By being aware of this distinction, you can save time and prevent unnecessary confusion by ensuring that you provide the appropriate reference number in the right context.

Is UTR the Same as Transaction ID?

The short answer is no, but it's crucial to understand how the two relate to one another.

In simple terms, a UTR number is a subset of Transaction IDs. Not all Transaction IDs are UTR numbers, even though all UTR numbers are eligible to be Transaction IDs since they identify transactions.

This implies that the UTR number will serve as your Transaction ID in the case of a bank transfer. However, the Transaction ID you obtain won't be regarded as a UTR if you are paying with cards or UPI.

When speaking with banks or payment platforms, the difference is especially helpful because utilising the right terminology guarantees quicker and more precise assistance.

Where Is Transaction ID Used vs Where UTR Is Used?

The payment type you are choosing will determine how Transaction IDs and UTR numbers are used.

In modern digital payment systems like UPI apps, online payment gateways, card transactions, and mobile wallets, transaction IDs are frequently utilised. The Transaction ID enables consumers to swiftly authenticate and trace their payments, and these systems are made for speed and ease.

However, traditional banking systems use UTR numbers, especially for interbank transfers. The UTR number serves as the official transaction reference whenever funds are transferred between banks via NEFT, RTGS, or IMPS.

Practically speaking, you will probably want a UTR number if your transaction includes a bank account and a transfer between banks. A Transaction ID will be utilised in place of apps, cards, or online platforms.

Real-Life Examples

Let's examine a few actual situations get a better understanding of the difference.

Assume you use a UPI app to send a friend ₹5,000. The payment is finished in a matter of seconds, and you get a Transaction ID and a confirmation. You can use this ID to check the status of your payments or file a complaint if something goes wrong.

Now imagine a different scenario in which you use NEFT to send ₹50,000 using online banking. In this case, the transaction's official reference is a UTR number created by the bank. The bank will utilise the UTR number to look into the matter if the payment is not received or is delayed.

Both kinds of identifiers may be useful in a business setting, particularly for freelancers or exporters who are getting paid. A SWIFT reference number, which acts globally similarly to a Transaction ID, may be used in an international transfer, whereas a UTR number may be generated in a local transfer.

These illustrations show how the type of identifier is totally dependent on the mode of payment.

How to Find Transaction ID and UTR Number

Most consumers frequently ignore the reference information displayed on the screen after a payment has been made. However, the Transaction ID or UTR number becomes the most crucial piece of information when a transaction fails, is delayed, or requires verification.

Although both identifiers are easily accessible, how you find them will vary depending on how the payment was completed. Knowing where to search can help you solve problems much more quickly and save time.

How to Find a Transaction ID

Almost all digital payments, including UPI, card payments, wallets, and internet transactions, create a Transaction ID. The Transaction ID is made to be easily accessible because these payments are usually handled via apps or online platforms.

Payment Confirmation Screen

Most apps provide a confirmation page right after a transaction is finished. All of the important payment-related information, including the Transaction ID, is displayed on this screen. Despite the fact that this is the quickest way to access it, many people fail to see the reference because they close the screen too quickly.

UPI or Banking App Transaction History

You may always get the Transaction ID from your app later if you don't see the confirmation screen. You can choose a particular payment and see all related information, including the Transaction ID, by going to the transaction history or passbook section of your UPI or banking app.

SMS or Email Notifications

When a transaction is completed, the majority of banks and payment providers immediately notify users. Important details, including the amount, transaction status, and reference number, are usually included in these notifications. It's simpler to just open the message and search for the transaction reference specified inside it rather than listing details individually.

Payment Receipts or Invoices

When you pay a company or merchant, you might get an invoice or a receipt. The Transaction ID is typically included in these documents as part of the payment reference, which makes it simple to find later.

Customer Support or Help Section

If you are unable to find the Transaction ID through the usual methods, most apps provide a help or support section where you can access transaction details. In situations where even that doesn’t work, customer support teams can retrieve the Transaction ID using basic information like the date, amount, and recipient.

Why this matters

Transaction IDs are purposefully made simple to get because they are utilised throughout app-based ecosystems. Having easy access to this ID guarantees that you can monitor your payments or take care of problems right away.

How to Find a UTR Number

UTR numbers are created within banking systems and are mostly connected to bank transfers like NEFT, RTGS, and IMPS, in contrast to Transaction IDs. As a result, rather than payment apps, they are usually found in bank-related information.

Bank Statement

Your bank statement is one of the most trustworthy sources for a UTR number. Every transaction entry on a statement, whether it is downloaded online or seen in person, has a reference number, which is your UTR. When examining previous transactions or confirming high-value transfers, this technique is especially helpful.

Net Banking Portal

You can access your transaction history by logging in if you use online banking. You can read full details with the UTR number clearly visible by choosing a specific transfer. Additionally, a lot of institutions offer downloaded transaction receipts with this reference.

SMS Alerts from Bank

When a transaction is started or finished, banks usually send out SMS alerts. In addition to transaction-related data, these messages contain a reference number, or UTR. The UTR is often included in the message rather than displayed as a distinct labelled field, though the structure may vary between banks.

Email Notifications

Banks may send email confirmations for specific transactions, particularly business or high-value transfers. These emails are a dependable source for obtaining the UTR number when necessary because they include a thorough explanation of the transaction.

Contacting the Bank

The last resort is to get in touch with your bank if you are unable to find the UTR number via statements, SMS, or online banking. The bank can track the transaction and provide you with the UTR number if you give them basic information, such as the transaction date, amount, and beneficiary details.

Why this matters

When interacting with banks, UTR numbers are crucial, particularly when transactions are unsuccessful or delayed. Having this reference number on hand guarantees better clarity and faster resolution because banks use it to look into transactions.

Pro Tip

After making a significant payment, it is usually a good idea to save or take a screenshot of your Transaction ID or UTR number. This simple habit can help you stay stress-free and make it much simpler to track or fix problems later.

Common Mistakes People Make in Transaction ID and UTR Number

Even though these identifiers are crucial, a lot of users make preventable errors that might make tracing payments more difficult.

Confusion between a Transaction ID and a UPI ID is one of the most frequent mistakes. A Transaction ID identifies a particular transaction, whereas a UPI ID identifies a user. Sharing the incorrect one can cause problems to take longer to resolve.

Incorrect reference number input is another common error. Banks or platforms may be unable to locate the transaction due to even a small misspelling, which can cause inconvenience and waste time.

Additionally, a lot of people forget to store their transaction data since they think they won't need it in the future. However, it can be more challenging to resolve unsuccessful or delayed payments if the right reference is missing.

Furthermore, when contacting support, users frequently give the incorrect kind of identifier—for example, a Transaction ID when a UTR is needed. The entire process may be slowed down as a result.

Preventing these errors guarantees a more seamless and dependable payment process in addition to saving time.

Conclusion

UTR numbers and transaction IDs are essential to the smooth operation of modern financial systems. Regardless of the mode of payment, they guarantee that each transaction is uniquely identifiable, traceable, and verifiable.

Even while the differences between the two might not seem like much, knowing it can greatly enhance your capacity to monitor payments, handle problems, and interact with banks and payment platforms.

Understanding these ideas is now crucial as the scope and complexity of digital payments continue to expand.

How Infinity Simplifies International Payment Tracking

Payment monitoring is frequently overly complicated by traditional banking systems, particularly when there are numerous middlemen, delays, and hidden fees. For freelancers and businesses that conduct business internationally, this becomes even more difficult.

By providing a quicker, more transparent, and user-friendly payment experience, Infinity helps eliminate these inefficiencies.

You don't need to rely on different systems or unclear reference numbers when using Infinity to track your international payments in real time. You can stay updated at every level because the platform guarantees total insight into your transactions.

What truly sets Infinity apart is its transparent pricing structure. With a flat 0.5% transaction fee (all inclusive) and 0% forex markup, you know exactly what you’re paying without worrying about hidden costs.

In addition to this, Infinity offers 24-hour settlements, ensuring faster access to your funds, and instant, free FIRA, making compliance effortless for freelancers and exporters.

All your transactions are managed through a centralised dashboard, giving you complete control and clarity in one place.

In a world where payment tracking can often feel fragmented and confusing, Infinity brings simplicity, speed, and transparency together.

FAQ on Transaction ID vs UTR

What is the difference between Transaction ID and UTR?

A Transaction ID is used for all types of payments, while a UTR is specifically used for bank transfers like NEFT, RTGS, and IMPS.

Is the UTR number the same as the Transaction ID?

No, but a UTR is a type of Transaction ID used in banking systems.

Where is the UTR number used?

It is used in bank transfers such as NEFT, RTGS, and IMPS.

Can I track payments using the Transaction ID?

Yes, Transaction IDs help track payment status and resolve issues.

How can I find my UTR number?

You can find it in your bank statement, net banking portal, or SMS from your bank.

Which is better: Transaction ID or UTR?

Neither is better, they serve different purposes depending on the type of transaction.