Taxation & Compliance

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

TL;DR

FIRC (Foreign Inward Remittance Certificate) is an official bank-issued certificate. FIRC was historically used as proof of receiving international payments in India. Although, since 2016, it has been issued only for capital account transactions like FDI and FII.

FIRA (Foreign Inward Remittance Advice) is the modern, RBI-mandated replacement for FIRC for all routine export collections. This includes freelance payments, IT/software exports, consulting fees, and goods exports. If you are a freelancer or exporter in India, FIRA is the document you need.

eFIRA is the electronic version of FIRA. It is digitally issued via the EDPMS (Export Data Processing and Monitoring System), and it is legally equivalent to a physical FIRA.

Getting FIRA from a traditional bank involves visiting the forex desk, submitting a written request, waiting 5–7 business days, and then sometimes paying bank charges. It is slow, manual, and frustrating.

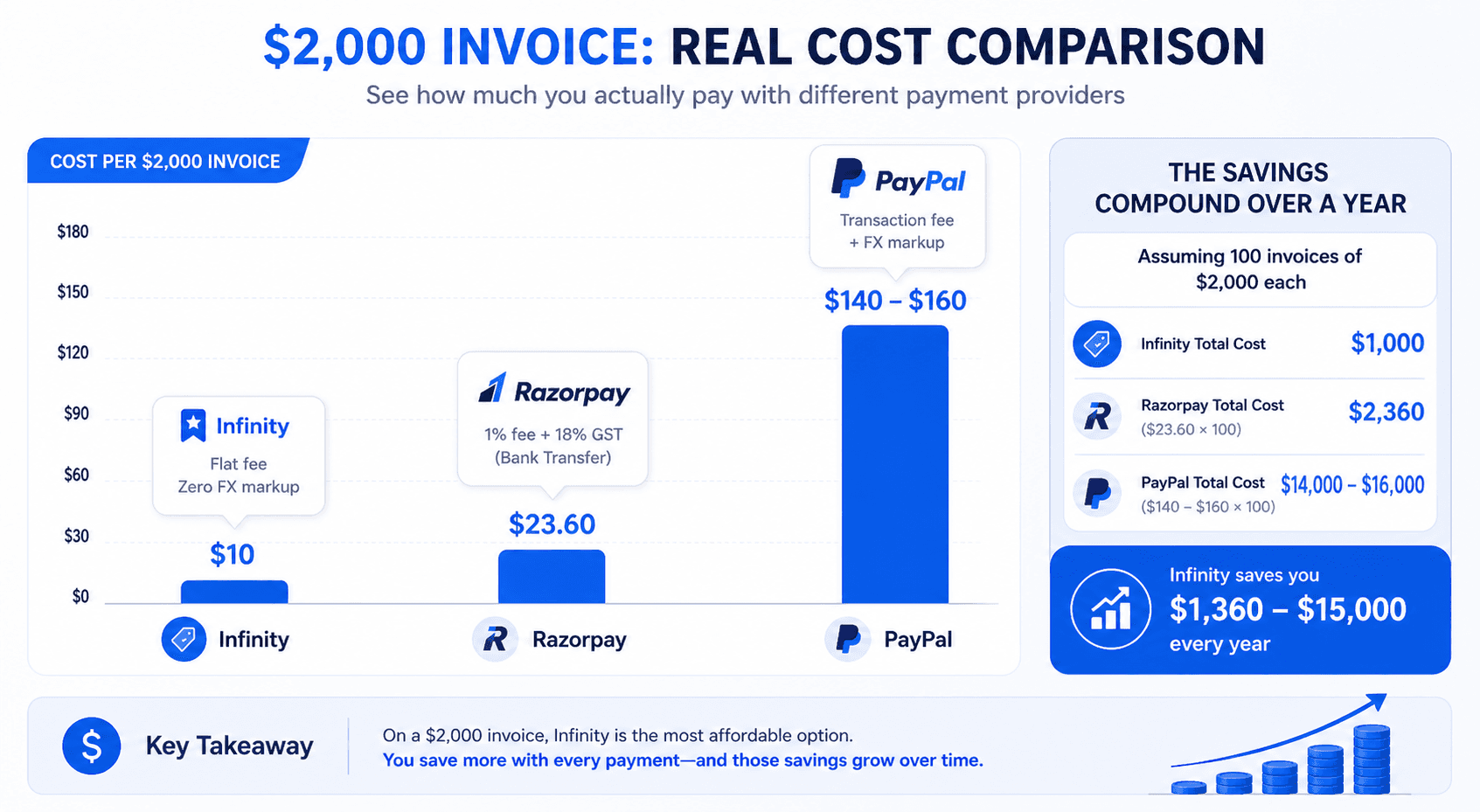

Infinity auto-generates a free FIRA with every successful international payment. It is issued by an RBI-authorised AD-1 bank, delivered digitally within 24 hours, with no paperwork or bank visits required. Combined with a flat 0.5% all-inclusive fee and zero FX markup, Infinity is the best platform for receiving international payments in India in 2026. (You can sign up with Infinity now).

Introduction: India's $137.7 Billion Remittance Story

India is the undisputed global leader in foreign inward remittances. In 2024, the country received a staggering $137.7 billion in international payments market. India is becoming the first nation in history to cross the $100 billion mark in annual remittance inflows. Behind this number are millions of Indian professionals who are working day and night with global clients.

Every single one of these transactions, like every dollar, pound, and euro that flows into an Indian bank account, comes with a compliance obligation. Under the Foreign Exchange Management Act (FEMA), every inward foreign remittance must be documented, categorised with the correct purpose code, and backed by official proof of receipt. That proof comes in the form of one of two documents: a FIRC or a FIRA.

Despite their critical importance, these two terms remain deeply misunderstood. Many Indian freelancers and exporters use them interchangeably. This blog breaks down FIRC and FIRA in detail. It explains what each document is, how they differ, and which one applies to your specific situation. At the end of the blog, you will understand whether FIRC or FIRA is useful to you.

What Is a FIRC? (Foreign Inward Remittance Certificate)

A Foreign Inward Remittance Certificate (FIRC) is an official document issued by an Authorised Dealer (AD) bank in India. It is a formal proof that a foreign currency payment has been received by an Indian individual or entity from an overseas source. In simple terms, it is the receipt that says: "This Indian bank account received this specific amount of foreign money, from this sender and on this date, for this purpose."

The FIRC has a long history in Indian banking. For decades, right up until 2016, it was the universal document used by every Indian professional for receiving any kind of international payment. Whether you received $500 from a US client for a design project or $500,000 from a foreign investor putting money into your startup, the document that proved it was the same: a FIRC, issued physically by your AD bank.

The FIRC contained several critical pieces of information that made it a legally powerful document. It recorded the full name and address of the remitter (the overseas sender), the name and address of the beneficiary in India (you or your business), It also included the exact amount received in foreign currency, the equivalent INR amount after conversion, the exchange rate applied at the time of conversion, the purpose code indicating the nature of the transaction, the Unique Transaction Reference (UTR) number, and the name of the AD bank that processed the remittance.

For Indian exporters, the FIRC was not merely a compliance document; it was a gateway to financial benefits. It was required to claim GST refunds on zero-rated exports, to access DGFT (Directorate General of Foreign Trade) incentive schemes. It was also used to apply for the EPCG (Export Promotion Capital Goods) scheme and to prove foreign currency inflow for tax and audit purposes.

However, the physical FIRC era effectively ended in 2016. It was a turning point that reshaped how international payment documentation works in India.

What Is a FIRA? (Foreign Inward Remittance Advice)

A Foreign Inward Remittance Advice (FIRA) is the modern-day document for proving receipt of receiving international payments in India. Structurally, it serves the same core purpose as a FIRC, that is, confirming that foreign currency was received by an Indian beneficiary. Although FIRA exists in a different format. It is issued through a different regulatory channel, and applies to a different (and now much broader) category of transactions.

FIRC was a formal certificate issued on bank letterhead and typically delivered physically. A FIRA is an advice document. It is a digital notification that is generated electronically and delivered to the beneficiary, usually as a PDF via email or through an online banking portal. The eFIRA (Electronic Foreign Inward Remittance Advice) is the most common format in 2026. It is a fully digital document that carries the same legal and compliance weight as any physical document it replaced.

The FIRA contains all the essential remittance details that Indian professionals and businesses need for compliance. It includes the beneficiary's name and bank account details, the remitter's name and address, the foreign currency amount received, the INR equivalent after conversion, the exchange rate applied, the purpose code, the Unique Transaction Reference (UTR), and other important details.

Why FIRC Was Replaced by FIRA for Most Transactions?

The single most important event in the history of Indian inward remittance documentation happened in 2016. This is when the Reserve Bank of India launched the Export Data Processing and Monitoring System (EDPMS).

Before EDPMS, export payment tracking in India was largely manual. Banks maintained paper records, exporters chased physical FIRCs, and the government had limited visibility into whether export proceeds were being realised within the mandated timeline. The system was slow, opaque, and prone to gaps.

EDPMS changed all of this. It created a centralised digital platform through which all AD Category-I banks can report every inward remittance against export transactions directly to the RBI. Every time a payment comes in against an export invoice, it is recorded in EDPMS with a unique Inward Remittance Message (IRM) number.

As part of this digitisation initiative, the RBI issued new guidelines instructing AD Category-I banks to stop issuing physical FIRCs for export collections. This covered goods exports, software exports, IT-enabled services, consulting, and all other trade transactions. In their place, banks were required to issue FIRA (or eFIRA) through the EDPMS system.

This shift was transformative. It brought greater transparency to India's export payment system, making tracking and reconciliation faster for both banks and the government. This transformation had set the stage for fintech platforms to issue eFIRAs automatically and instantly by eliminating the manual, delay-prone process that had frustrated Indian exporters for decades.

FIRA vs FIRC — Key Differences (Side-by-Side)

Understanding the distinction between FIRA and FIRC is essential for every Indian professional receiving international payments. Here is a detailed comparison across all the parameters that matter:

Full Form: FIRA stands for Foreign Inward Remittance Advice. FIRC stands for Foreign Inward Remittance Certificate.

Nature of Document: FIRA is an advice or notification document. It informs the beneficiary that a foreign payment has been received and credited. FIRC is a formal certificate. It provides official attestation of the receipt of foreign funds.

Issuing Authority: Both are issued by AD (Authorised Dealer) Category-I banks in India. However, FIRA is now generated digitally through the EDPMS system, while FIRC (where still applicable) may be issued on bank letterhead.

Format: FIRA is issued electronically as an eFIRA, a digital PDF document. FIRC was traditionally issued as a physical paper certificate, though electronic versions (eFIRC) exist for certain capital account transactions.

Who Needs It: Freelancers, IT service exporters, SaaS companies, goods exporters, and agencies receiving payment from overseas clients need FIRA. Businesses receiving foreign investment (FDI) or foreign institutional investment need FIRC.

EDPMS Linkage: FIRA is directly tied to the EDPMS system. Every FIRA corresponds to an IRM entry in EDPMS, which is the mechanism through which the RBI monitors export realisation. FIRC is not linked to EDPMS in the same way.

GST Refund Claims: For zero-rated export GST refund claims, FIRA (or eFIRA) is now the required proof of foreign exchange realisation. Physical FIRCs are no longer accepted for routine export GST claims since 2016.

DGFT Incentives: Both documents can be used for DGFT purposes, though the specific requirement depends on the scheme. For eBRC (Electronic Bank Realisation Certificate) generation, which is mandatory for claiming RoDTEP and other export incentive schemes, FIRA is now the relevant document.

Availability on Modern Platforms: Most modern Indian fintech platforms (including Infinity, Xflow, Skydo) auto-generate eFIRA with every transaction. FIRC for FDI must still be manually requested from your AD bank.

Cost: Many banks charge a fee for issuing FIRA manually, typically ₹500–₹2,000 per certificate, depending on the bank and account type. Modern fintech platforms like Infinity provide FIRA free of charge with every transaction.

What is eFIRA? (Electronic Foreign Inward Remittance Advice)

The eFIRA, or Electronic Foreign Inward Remittance Advice, is simply the digital version of FIRA. In 2026, virtually all FIRAs issued in India are eFIRAs. The physical paper format has been almost entirely replaced by digital PDFs issued through the EDPMS system or directly by RBI-authorised payment platforms.

Despite being digital, the eFIRA carries exactly the same legal and compliance validity as any physical document. It is accepted by the GST department for refund claims, by the Income Tax department during assessments, by the DGFT for incentive schemes, and by auditors for FEMA compliance verification.

When Do You Need FIRA vs FIRC?

The most practical question for any Indian professional is: which document do I actually need for my situation? Here is clear, use-case-by-use-case guidance.

Freelancers receiving service payments from overseas clients — You need a FIRA. Whether you are a freelance developer, designer, writer, consultant, or any other service provider billing international clients, all your inward payments are current account transactions covered by FIRA.

IT and software exporters — You need a FIRA (eFIRA). Software and IT-enabled service exports are categorised under specific purpose codes (P0802 for software consultancy, P0803 for other IT services) and are reported through EDPMS. Your bank or fintech platform generates the eFIRA, which is then used for GST refund claims and FEMA compliance.

SaaS companies collecting international subscriptions — You need a FIRA. Subscription-based foreign currency income from overseas customers is treated as a service export and documented with FIRA.

Goods exporters — You need a FIRA, which is then linked to your Shipping Bill in EDPMS to generate an eBRC (Electronic Bank Realisation Certificate).

Businesses receiving Foreign Direct Investment (FDI) — You need an FIRC. When a foreign entity invests equity capital into an Indian company, the Indian company must obtain an FIRC from its AD bank as proof of the capital infusion.

Businesses receiving Foreign Institutional Investment (FII) — You need an FIRC. Portfolio investments by registered foreign institutional investors into Indian securities markets require FIRC documentation.

Claiming GST refunds on zero-rated exports — You need a FIRA. Since 2016, GST refund claims for export of services must be backed by FIRA or eFIRA. Physical FIRCs are no longer accepted for this purpose by the GST department.

Applying for DGFT incentive schemes (EPCG, Advance License) — Historically, it required FIRC. In the post-EDPMS era, the relevant document requirements vary by scheme. You should consult your DGFT advisor or CA for the specific current requirement.

Key Information Contained in FIRA and FIRC

Both FIRA and FIRC record specific transaction details that make them valid compliance documents. Understanding what each field means will help you in verifying your documents and resolving discrepancies quickly.

Unique Transaction Reference (UTR): It is a unique alphanumeric code that identifies the specific inward remittance transaction within the Indian banking system. The UTR is your primary reference for tracking a payment and reconciling it against invoices.

Remitter Details: The full name, address, and bank details of the overseas entity or individual who sent the payment are in FIRC or FIRA. This field proves the foreign origin of the funds and links the remittance to a specific client.

Beneficiary Details: Your full name (or your company's legal name), address, and the Indian bank account into which the funds were credited are contained in FIRA and FIRC.

Foreign Currency Amount: The exact amount received in the original foreign currency (USD, GBP, EUR, etc.) before conversion to INR.

INR Equivalent Amount: The rupee value credited to your account after FX conversion is recorded in FIRA and FIRC. It is calculated using the exchange rate applied at the time of processing.

Exchange Rate Applied: The specific USD/INR (or other currency pair) rate used for conversion. This is a critical field for verifying that your platform or bank has not applied an undisclosed FX markup.

Purpose Code: An RBI-mandated code that categorises the nature of the transaction. For IT services, the code is P0802; for other business services, P0803; for consulting, P0899; and so on. Correct purpose codes are essential for EDPMS reporting and GST refund eligibility.

AD Code: The Authorised Dealer code identifying the specific bank branch that processed and reported the inward remittance to the RBI. This links your transaction to the regulated banking infrastructure.

Date of Receipt: The date on which the foreign currency was credited to your account. This is used for FEMA compliance timelines.

Narration/Nature of Transaction: A description of what the payment is for — e.g., "software export services," "IT-enabled services," "consulting fees." This narration supports the purpose code and provides additional context for auditors.

How Infinity Simplifies FIRA? And Why It's the Best Platform for Receiving International Payments

The traditional FIRA process is like a painful administrative obligation layered on top of an already complex cross-border payment journey. And it is exactly the problem that Infinity is eliminating along with every other friction point in the international payment collection experience for Indian professionals.

Automatic FIRA With Every Payment

With Infinity, FIRA generation is not a process; it is a guarantee. Infinity automatically triggers a free FIRA certificate, issued by an RBI-authorised AD-1 bank, with every international payment received. It is delivered instantly with every successful transaction.

There is no request letter to write. No forex desk to visit. No 5–7 day wait. No follow-up calls to your relationship manager. No fee per certificate. The moment your international payment clears, your compliance documentation is already on its way to your inbox.

For a freelancer in Bangalore who is receiving 5–8 international payments per month, this means 5–8 FIRA certificates will be automatically generated per month.

The Lowest Fees in the Market

Beyond FIRA automation, Infinity's fee structure is the most competitive available for Indian inward remittances in 2026. The platform charges a single flat fee of 0.5% on every transaction — all-inclusive. This 0.5% covers the platform charge, GST, FIRA generation, FX conversion, and INR settlement. There are no additional layers, no GST charged separately, no withdrawal fee, and no FX markup.

Zero FX Markup

Infinity converts your foreign currency to INR at the live mid-market exchange rate (the same rate you see on Google) at the time of conversion. There is no spread applied, no markup layered into the rate, and no gap between what the market shows and what you receive.

24-Hour INR Settlement

Infinity settles funds to your Indian bank account within 24 hours of receiving the international payment. This is dramatically faster than traditional bank SWIFT settlements (3–7 business days), Razorpay's T+7 international settlement, or PayPal's 2–5 day timeline.

Full RBI and FEMA Compliance

Every transaction processed through Infinity flows through AD-1-certified, RBI-authorised banks. It is the highest tier of regulated banking infrastructure in India. Every payment is FEMA-compliant, tagged with the correct purpose code, and reported through proper banking channels. Funds never sit with Infinity itself. They move directly through regulated banking channels from your client's account to your Indian bank.

Why Infinity Is the Complete Solution

The case for Infinity is not built on any single feature; it is the combination of everything working together. The lowest fees in the market. Zero FX markup. 24-hour settlement. Automatic free FIRA with every payment. Full RBI and FEMA compliance. Local virtual receiving accounts in 50+ currencies. Built-in invoicing.

For Indian freelancers, agencies, SaaS companies, IT exporters, and consultants receiving international payments, Infinity eliminates every friction point in the process. From the moment your client hits "send" to the moment your INR lands in your bank account and your FIRA arrives in your inbox. In 2026, there is no more complete, cost-effective, or compliant solution available in the Indian market for inward remittances.

FIRA vs FIRC — Quick Reference Comparison Table

Parameter | FIRA | FIRC |

Full Form | Foreign Inward Remittance Advice | Foreign Inward Remittance Certificate |

Nature | Advice / notification document | Formal certificate |

Format | Digital (eFIRA) — PDF | Physical (historically); eFIRC for some capital transactions |

Issued By | AD Category-I banks via EDPMS | AD Category-I banks |

Applies To | Current account transactions — exports, services, freelance | Capital account transactions — FDI, FII |

Who Needs It | Freelancers, IT exporters, SaaS, goods exporters | Businesses receiving foreign investment |

EDPMS Linked | Yes — tied to IRM number | No |

Valid for GST Refund | Yes (post-2016 standard) | No (not accepted for routine export claims) |

DGFT Incentives | Yes (via eBRC linkage) | Varies by scheme |

Issued Since | 2016 (post-EDPMS) | Pre-2016 (now restricted to FDI/FII) |

Cost from Traditional Banks | ₹500–₹2,000 per certificate | ₹500–₹2,000+ per certificate |

Cost via Infinity | Free — auto-generated with every payment | N/A |

Delivery Time (Traditional Bank) | 5–7 business days | 7–10 business days |

Delivery Time via Infinity | Within 24 hours — automatic | N/A |

Mandatory Record-Keeping | 5 years (FEMA requirement) | 5 years (FEMA requirement) |

Frequently Asked Questions (FAQs) about FIRA vs FIRC

Q1. What is the main difference between FIRA and FIRC?

FIRA (Foreign Inward Remittance Advice) is the document used to prove receipt of international payments for current account transactions. FIRC (Foreign Inward Remittance Certificate) is now used primarily for capital account transactions such as FDI and FII.

Q2. Do freelancers in India need a FIRA or a FIRC?

Freelancers need a FIRA. All freelance service payments received from overseas clients are current account transactions, covered by the modern FIRA/eFIRA system.

Q3. Is FIRA valid for claiming GST refunds on the export of services?

Yes. FIRA (specifically eFIRA generated through EDPMS) is the required proof of foreign exchange realisation for claiming GST refunds on zero-rated exports of services.

Q4. What does eFIRA mean?

eFIRA stands for Electronic Foreign Inward Remittance Advice. It is the digital version of FIRA. It is a PDF document generated electronically through the EDPMS system by your AD bank or RBI-compliant fintech platform.

Q5. How does Infinity generate FIRA automatically?

Infinity operates in partnership with AD-1 certified RBI-authorised banks. Every time an international payment is received and settled through Infinity, the banking infrastructure automatically generates an eFIRA linked to that transaction.

Q6. Is FIRC still issued in 2026?

Yes, but only for specific capital account transactions. If your Indian company receives foreign direct investment (FDI) from an overseas investor, or if foreign institutional investors (FIIs) invest in your securities, your AD bank will still issue a FIRC as proof of that capital infusion]