Taxation & Compliance

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

TL;DR

A financial organisation that serves as a middleman between the sending and receiving banks during an international transfer is known as an intermediary bank. The payment goes via one or more intermediary banks to finish the transaction when two banks are not directly connected to each other. With the help of networks like the SWIFT (Society for Worldwide Interbank Financial Telecommunication), these banks assist in the processing of cross-border payments, but they may also charge extra costs. Because of middleman fees, foreign exchange rate markups, and processing costs, recipients sometimes receive less money than expected.

Introduction

As businesses expand globally and freelancers work with international clients, cross-border payments have become an everyday part of modern businesses.

Businesses frequently transfer funds between nations for investments, products, and services. However, compared to domestic payments, international bank transfers are often more complicated.

International payments often go via several banks before they reach the receiver, in contrast to domestic bank transfers that go straight between two accounts. These extra organisations that are referred to as intermediary banks, plays an essential role in facilitating international transfers.

The ecosystem for international cross-border payments is enormous. International trade, freelancing, and digital services are expected to accelerate cross-border payment flows to exceed $250 trillion annually by 2027, according to estimates by McKinsey & Company.

Many international transfers still rely on traditional banking networks and correspondent banking connections, despite technological developments in financial services. Because of this, intermediary banks continue to play a significant role in the global payment system.

Businesses, exporters, and freelancers who often handle international payments must understand how intermediary banks operate, why they are needed, and what hidden costs they may bring in the whole transfer process.

What Is an Intermediary Bank?

An intermediary bank is a financial institution that acts as a middle bank in an international money transfer. When there is no direct relationship between the sender's and recipient's banks, it helps in routing the money between them.

Not every bank in the world has direct ties to every other bank. Rather, banks conduct international transactions through networks of partner institutions. The payment is routed through an intermediary bank that facilitates the transfer in the absence of a direct banking relationship.

Usually, these banks are part of global payment networks like SWIFT, or the Society for Worldwide Interbank Financial Telecommunication. Banks can securely transmit standardised payment instructions to one another via the SWIFT system.

To put it simply, an intermediary bank facilitates international transfers between banks that do not have direct accounts with one another by acting as a link.

What is the difference between a correspondent bank and an intermediary bank?

A financial institution that offers banking services on behalf of another bank, typically located abroad, is known as a correspondent bank. It keeps track of the partner bank's accounts and assists with currency exchanges, trade finance, and foreign transactions.

In contrast, when there is no direct contact between the sending and receiving banks, an intermediate bank serves as a middle bank that temporarily provides a route for an international transfer between them.

To put it simply, an intermediary bank primarily assists in the routing of a particular cross-border payment through networks such as the Society for Worldwide Interbank Financial Telecommunication, whereas a correspondent bank maintains long-term banking ties.

How an Intermediary Bank Works in International Transfers

It is important to look at how a standard international bank transfer operates in order to understand the function of intermediary banks.

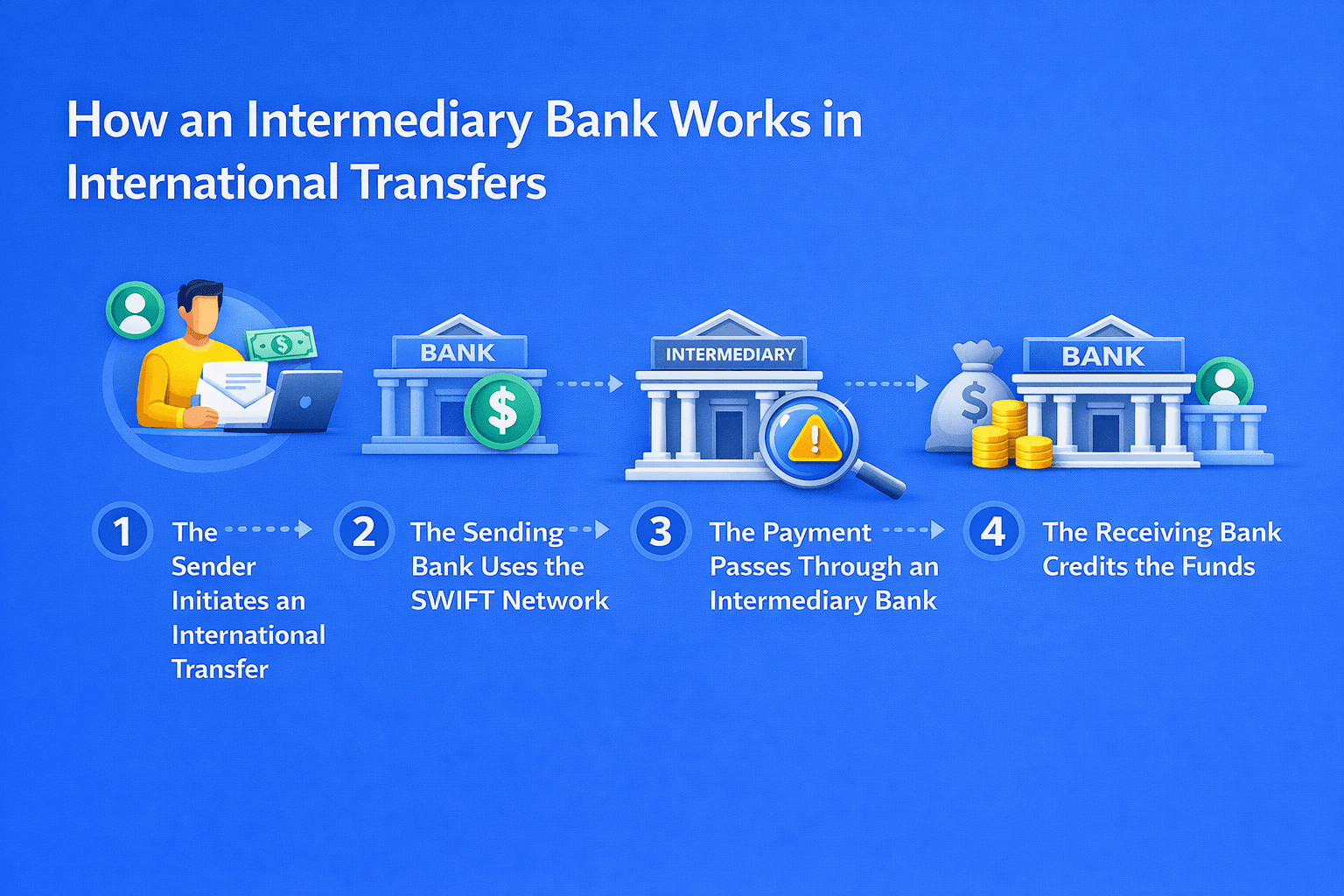

Step 1: The Sender Initiates an International Transfer

When a sender gives their bank instructions to transfer funds to a receiver in another nation, the process starts. This could be a personal transfer, a freelancer payment, or a corporate payment.

The sender gives information like:

Recipient’s bank name

Account number or IBAN

SWIFT/BIC code

Transfer amount and currency

The sending bank then prepares the payment instruction.

Step 2: The Sending Bank Uses the SWIFT Network

The payment instruction is sent over the SWIFT network by the sender bank. In simple terms, SWIFT is a messaging system that enables banks to safely exchange payment details.

Although, it is important to understand that the transmitting bank and the recipient's bank might not be directly connected.

Step 3: The Payment Passes Through an Intermediary Bank

The payment must go through one or more intermediary banks that have accounts with both institutions if there is no direct connection between the two banks.

When a U.S. bank transfers funds to an Indian bank, for instance, it may do it via a major international bank in Europe or Asia that has connections to both organisations.

Step 4: The Receiving Bank Credits the Funds

After completing all the necessary checks and currency conversions, the recipient's bank credits the funds to their account.

Even though the procedure is often effective, whenever a new intermediary bank is introduced in the system, additional fees and delay might occur.

Example of an Intermediary Bank Transfer

Imagine a simple situation where a client in the US and a freelancer in India are involved.

1. An Indian freelancer receives $1,000 from a U.S. client via a traditional international bank transfer.

2. The payment is sent over the SWIFT network by the client's bank.

3. The payment is sent through one or two intermediary banks because the U.S. bank might not have a direct connection with the Indian bank.

4. After processing the transaction, these intermediary banks send it to the Indian bank.

5. The money is credited to the freelancer's account by the receiving bank.

Intermediary banks may, however, charge fees during this procedure before transferring the money. Consequently, the freelancer may get between $950 and $980 less than the entire $1,000.

Why Banks Use Intermediary Banks

The nature of the global banking system makes intermediary banks an important part of the process. It would be incredibly difficult and expensive to maintain direct connections with every bank in the world.

Rather, banks use networks of correspondent banks to facilitate international payment routing.

Lack of Direct Banking Relationships

Only a small number of foreign banks have direct accounts with the majority of banks. They depend on intermediary banks to finish the transfer when they need to send money to a bank outside of this network.

Currency Settlement

Currency conversions are a common part of international payments. These conversions and the settlement of transactions in the correct currency are made easier by intermediary institutions.

Global Banking Connectivity

Due to their broad global banking connections, large international banks frequently act as intermediaries. These organisations serve as hubs that link smaller banks in different parts of the world.

Hidden Costs of Intermediary Banks

Although intermediary banks facilitate international transfers, many senders and recipients are unaware of the hidden expenses they intermediary banks may impose.

Intermediary banks expenses are one of the most frequent causes of deductions from international transfers.

Intermediary Bank Fees

In order to route the transaction, intermediary institutions may impose a processing fee.

For each intermediary bank, these costs usually fall between $10 and $50.

Multiple deductions may take place when a transfer involves two or three intermediary banks.

Currency Conversion Markups

Banks may add exchange rate markups if the transfer involves currency conversion. The total cost of the transfer may rise as a result of these markups.

A bank might, for instance, give an exchange rate that is somewhat lower than the market rate, thereby imposing an extra, hidden cost.

Receiving Bank Charges

Fees may also be subtracted by the receiving bank prior to the money being credited to the recipient's account. The recipient can receive less money than expected since these fees are frequently imposed throughout the transfer process.

How to Identify If an Intermediary Bank Was Used

The involvement of intermediary banks in the transaction is typically unknown to both senders and recipients. Nonetheless, there are a number of methods to determine if an international payment went via intermediary banks.

SWIFT Payment Receipt

Information about the intermediary bank that is involved in the international transaction may be included in the sending bank's payment receipt or confirmation.

Bank Transaction Statement

Intermediary banks name may be mentioned in the bank statement's remarks or transaction description.

SWIFT Tracking

The SWIFT reference number can be used to track some international transfers. This enables banks to track the payment's route.

How to Reduce Intermediary Bank Charges

There are a few ways to reduce the fees related to intermediary banks, even though they are occasionally unavoidable.

Choose Transparent Payment Methods

One way to prevent surprise expenses is to use payment platforms that clearly show currency rates and transfer fees.

Avoid Multiple Currency Conversions

Costs may increase if the money is converted more than once during a transfer. Transfers should be made in the recipient's preferred currency wherever possible.

Use Platforms With Direct Banking Relationships

Some financial platforms like Infinity reduce the requirement for intermediary banks by maintaining direct banking ties across multiple nations.

How Infinity Helps Reduce Intermediary Bank Costs

Hidden intermediate fees may drastically reduce the amount earned by businesses, freelancers and exporters who receive international payments.

Traditional SWIFT transfers frequently require several banks, each of which may charge a fee of its own. Businesses find it challenging to predict the total amount they will get due to this lack of transparency.

By offering a more efficient method for cross-border transactions, Infinity makes international payments easier. Businesses can reduce unnecessary intermediary deductions and increase payment transparency by utilising modern payment technology and optimised banking connections.

Businesses and freelancers who often engage with foreign clients can make sure that a greater share of their earnings can reach their accounts by using modern fintech solutions like Infinity.

Conclusion

Businesses require more effective solutions to handle international payments as global commerce grows. Conventional bank transfers frequently depend on complex financial networks with numerous intermediary institutions.

By increasing transparency and cutting unnecessary intermediary fees, modern financial platforms like Infinity help in the streamlining of cross-border transactions. Infinity helps speed up, estimate, and reduce the cost of international payments for exporters, freelancers, and multinational corporations in India.

FAQ on Intermediary Banks

What is an intermediary bank in international transfers?

An intermediary bank is a financial institution that acts as a middle bank between the sending bank and receiving bank when they do not have a direct relationship.

Why do banks use intermediary banks?

Banks use intermediary banks to route international payments when they do not maintain direct accounts with the recipient’s bank.

What are intermediary bank charges?

Intermediary bank charges typically range between $10 and $50 per bank involved in the transfer.

Can intermediary banks delay international transfers?

Yes, each intermediary bank may add processing time, which can increase the overall transfer time.

How do I avoid intermediary bank fees?

Using payment platforms with direct banking relationships and transparent fee structures can help reduce intermediary bank charges.