Global payments

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

TL;DR

There is more to HDFC Bank's forex rates than just the obvious exchange rate. Even while the bank offers forex and foreign transfer services, the real cost often includes hidden fees like GST, intermediary taxes, and and forex markup (1%–3.5%).

These have the potential to dramatically raise a transaction's overall cost. Freelancers, companies, and exporters can cut expenses and select better options for international payments by knowing how these rates operate.

Introduction

More Indian companies and individuals than ever before are handling cross-border payments because to the rapid expansion of foreign trade, SaaS exports, and freelancing. Forex rates have a direct effect on how much you pay or receive, whether you're transferring money overseas or receiving payments from clients abroad.

A lot of people believe that the exchange rate that banks display is quite close to the "real" rate. In actuality, though, institutions like HDFC Bank impose extra fees and taxes in addition to a markup above the base rate. These unstated expenses may subtly lower the total amount you get or increase the amount you have to pay.

One of the biggest private sector banks in India, HDFC Bank, provides a variety of foreign exchange services, such as external remittances, forex cards, and overseas wire transactions. Even if it is a reputable organisation, it is crucial to understand the entire framework of its foreign exchange pricing in order to prevent unforeseen expenses.

This blog will explain how HDFC Bank currency rates operate, the related charges, any hidden costs, and useful tips on how to save money on international transactions.

What Are Forex Rates in HDFC Bank?

The price at which one currency is traded for another is known as a forex rate. The worldwide or interbank rate, however, differs from the rate that a bank offers.

You must be aware that each forex transaction comprises three essential elements in order to fully understand this.

Interbank (Mid-Market) Rate

When international banks trade currencies with one another, they use this actual exchange rate. Additionally, it is the rate that appears on financial sites or Google. There are no fees or markups included in this rate.

Bank Applied Rate

Over the interbank rate, HDFC Bank adds a margin, sometimes referred to as a forex markup. The type of transaction, consumer profile, and product used all affect this markup.

Final Rate Paid by Customer

When a transaction is finished, you actually receive this rate. The base rate, bank markup, and any relevant taxes are all included. The transaction is more costly because this rate is often greater than the interbank rate.

How HDFC Bank Forex Rates Work: Step-by-Step Explanation

It is easier to understand where expenses are added and how the final rate is determined when you follow the process step-by-step.

Step 1: Reference to Global Currency Markets

To find the basic exchange rate, HDFC Bank first examines international interbank currency markets. Due to supply and demand in international marketplaces, this rate is always changing.

Step 2: Application of Forex Markup

This base rate is then marked up by the bank. Because it is incorporated into the exchange rate itself, this markup is one of the largest contributors to the total cost and frequently goes unnoticed.

Depending on whether you are using a bank transfer, credit card, or forex card, this markup can vary from 1% to 3.5% for the majority of transactions.

Step 3: Additional Charges

Additional expenses, including remittance fees, forex card fees, and cross-currency fees, may be imposed after the markup.

Step 4: GST Application

The overall cost of the transaction is further increased by the application of 18% GST on service fees and forex conversion expenses.

Types of Forex Charges in HDFC Bank

It's crucial to break down all of the fees in order to fully understand HDFC forex rates.

Forex Markup Charges

The bank's hidden margin over the interbank rate is known as the "forex markup." Although it isn't often stated clearly, it has a big influence on the total amount.

For example, the markup is ₹1.5 if the bank offers ₹84.5 and the true exchange rate is ₹83 per USD.

Depending on the product:

Markups on credit and debit cards can range from 2% to 3.5%.

For cross-currency transactions, forex cards may have a markup of about 2%.

Because of this, the biggest hidden expense in the majority of transactions is FX markup.

Read more about HDFC forex markup here.

Remittance Fees

HDFC Bank levies a set remittance fee when sending money overseas.

Typically:

For smaller transfers, around ₹500

For larger transfers, around ₹1000

Intermediary bank costs are not included in these fees, which are evaluated separately.

Forex Card Charges

When travelling abroad, forex cards are frequently utilised. They are convenient, however they have a number of fees.

These could include costs for issue, reloading, withdrawals from ATMs, and inactivity. Cross-currency transactions may also result in additional markup.

Cross Currency Charges

Additional fees apply when a transaction combines multiple currencies, like converting INR to USD and then USD to EUR. Because of the double conversion, this may significantly increase the overall cost.

GST on Forex Transactions

Depending on the amount being converted, 18% GST is levied to foreign exchange transactions. The GST may be computed as a percentage for lower amounts, while a set structure is used for higher amounts.

Even though 18% GST might not seem like much on its own, when combined with markup and fees, it adds up.

Hidden Costs in HDFC Forex Rates

One of the biggest challenges with traditional banking forex services is the lack of transparency. Several costs are not clearly visible but still affect the transaction.

Forex Spread (Invisible Cost)

The Forex spread is the difference between the bank's rate and the interbank rate. This is where banks generate a large amount of their income.

The spread guarantees that the consumer pays more than the actual exchange rate even in the absence of an explicit fee.

Intermediary Bank Charges

Intermediary banks are frequently involved in international transactions, particularly when SWIFT is used. Fees may be deducted by these institutions throughout the transfer procedure.

These fees are unpredictable since HDFC Bank has no control over them and they are typically not mentioned up front.

Double Conversion Loss

Every conversion stage in a transaction involving different currencies could have a markup. The total amount received reduces as a result of multiple or even triple charges.

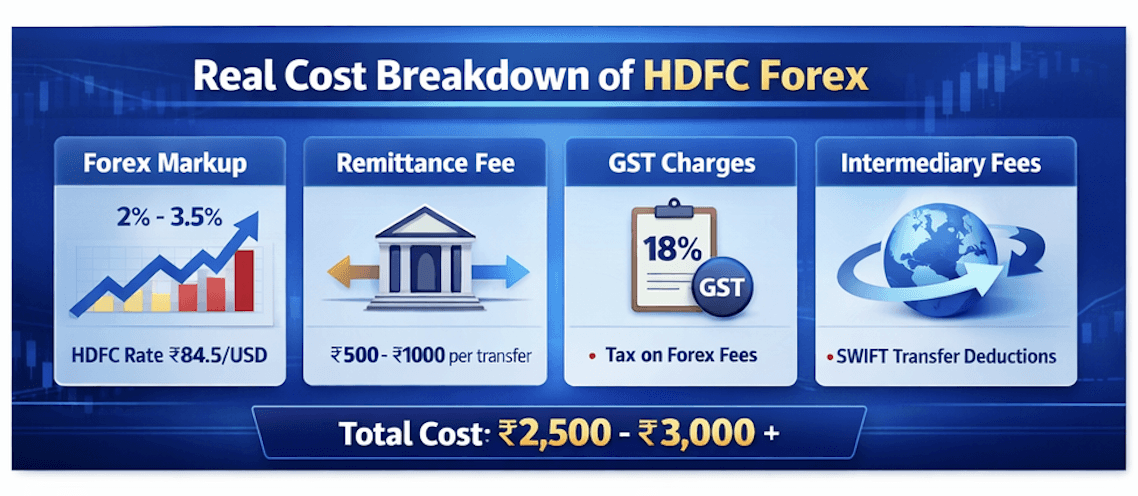

Example: Real Cost of an HDFC Forex Transaction

To understand the true importance of these charges, let's look at a real-world example.

Let's say you are sending $1,000 abroad.

Forex markup (~2%) → around ₹1,600

The transfer charge is ₹1000.

GST and other fees → extra

The total cost, excluding intermediate deductions, may reach ₹2,500–₹3,000.

This example shows how actual FX transaction costs might be far greater than anticipated.

Why HDFC Forex Rates May Be Higher

Traditional banks like HDFC charge higher foreign rates for a number of reasons.

Traditional Banking Infrastructure

Banks depend on outdated systems such as correspondent banking connections and SWIFT networks. Multiple parties are involved in these systems, which increases operating expenses.

Risk Management

Banks include a margin to protect themselves from currency fluctuations and market volatility.

Operational Costs

The expense of maintaining infrastructure, compliance procedures, and international banking networks is increased and passed on to clients through markup.

Limited Transparency

Because many consumers are unaware of how currency pricing operates, banks are able to include hidden expenses without making them obvious.

Tips to Reduce Forex Charges with HDFC Bank

Although HDFC Bank provides dependable services, there are ways to cut expenses.

Compare Exchange Rates

Before completing a transaction, always check the interbank rate and the bank's rate. This helps in your understanding of the markup.

Avoid Double Currency Conversion

To prevent multiple conversions, try to do transactions in the base currency wherever feasible.

Use Forex Cards Strategically

For some transactions, particularly when travelling, forex cards could provide better rates than debit or credit cards.

Negotiate for Large Transactions

For high-value transfers, banks may offer better rates if you negotiate.

How Infinity Helps You Save on Forex Costs

Due to hidden fees and slow procedures, traditional banking systems frequently make international payments costly. By providing a more effective and transparent method of cross-border payments, Infinity is built to address these issues.

Transparent Pricing

Infinity charges a flat 0.5% transaction fee, which is inclusive of all costs. This eliminates uncertainty and helps businesses clearly understand their expenses.

Zero Forex Markup

Infinity guarantees that customers receive exchange rates free of hidden margins by offering 0% FX markup, in contrast to typical banks.

No Hidden Charges

There are no intermediary deductions or surprise fees, making the entire process predictable.

Faster Settlements

With 24-hour settlement, businesses can access funds much faster compared to traditional bank transfers.

Instant and Free FIRA

Infinity provides instant and free FIRA, simplifying compliance for exporters and freelancers without additional costs.

Conclusion

In India, HDFC Bank offers a dependable and popular platform for foreign exchange operations. But there is more to using its services than just the obvious costs. The cost of foreign payments can be greatly increased by additional taxes, intermediary fees, and forex markup.

Making wise judgments requires an understanding of how FX rates operate. Particularly for companies with high transaction volumes, even a slight fluctuation in the exchange rate can result in significant losses.

Why Infinity Is a Smarter Alternative for Forex Transactions

Infinity provides the following solutions to the main issues with traditional FX systems:

Transparent pricing

There is no markup

24-hour settlements

streamlined compliance

This makes handling international payments more economical and efficient for independent contractors, exporters, and large businesses.

FAQ on HDFC forex rate

What is HDFC Bank's foreign exchange markup?

Depending on the kind of transaction, forex markup usually falls between 2% and 3.5%.

Why is the Google rate lower than the HDFC FX rate?

Because banks raise the final rate they provide to clients by adding a markup over the interbank rate.

Does HDFC impose fees on inward remittances?

Intermediary banks may deduct fees during the transfer, but HDFC may not charge directly.

How can I reduce my HDFC foreign exchange fees?

By checking rates, avoiding double conversions, and negotiating for big transfers, you can cut expenses.

Is a debit card more expensive than a forex card?

Yes, forex cards typically have a lower markup than credit or debit cards.

What is the GST on forex transactions?

18% GST is applied on forex conversion charges and varies based on the transaction amount.