Global payments

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

sign up with Infinity

India’s digital ecosystem has grown at a tremendous level over the last decade. Today, everyone relies on effective online payment solutions to accept money from customers, be it small businesses, freelancers or large enterprises in India.

Payment aggregators are the centre point of this digital ecosystem. A payment aggregator is a platform that simplifies the process of how businesses collect payments from their customers without the need to build a complex banking infrastructure.

But with so many options available in the market, businesses and freelancers are often confused about which payment aggregator to choose. They often struggle to understand:

What exactly is a payment aggregator?

How is a payment aggregator different from a payment gateway?

Which is the best payment aggregator available in India?

And is there a better alternative for receiving international payments in India from foreign clients?

In this blog, we will break down everything that you need to understand about PA (Payment Aggregators) in India. From what a payment aggregator is, to how it works, and a basic comparison between all the platforms available in India, we will simplify everything for you in this blog.

What is a Payment Aggregator?

A payment aggregator is a financial service provider that enables Indian freelancers and businesses to receive payments from their clients. A PA offers this service without the need for setting up a dedicated merchant account with a bank.

Instead of dealing with banks individually, businesses can simply integrate with a payment aggregator and start accepting payments via:

UPI

Debit/Credit cards

Net Banking

Payment Wallets

So basically, a payment aggregator acts as a merchant that handles the entire payment process securely between customers, merchants and banks.

What are the key components of a payment aggregator?

The following are the key components of a payment aggregator:

Merchant (Business that is accepting payment)

The merchant is the seller or service provider who wants to accept payments from customers online. Payment aggregators allow merchants to start quickly without heavy banking processes.

Customer (User making the payment)

A customer is the end user who has to make the payment to the business/merchant. A payment can be made using a preferred payment option like UPI or cards.

Payment Aggregator Platform

A PA is a financial service provider that initiates the payment process, routes it to the bank, ensures security, and manages final settlement.

Banking Network

Banks that authorise and process transactions behind the scenes.

Is GPay (Google Pay) a payment aggregator in India?

Yes, GPay acts as a payment aggregator in India. Google Pay has met the necessary qualifications, and with regulatory developments, it has received approval from the RBI to act as a payment aggregator in India.

However, GPay also acts as a UPI app. People are somewhat confused at this point. While GPay is widely used as a UPI app for peer-to-peer transfers, it also enables businesses collect payments using the payment aggregator capabilities.

How Payment Aggregators Work in India

It is very important to understand how payment aggregators work in India. This helps businesses to evaluate reliability, speed, and efficiency.

Step-by-step payment flow:

Payment initiated by customer: A user selects a product and then chooses a payment service like UPI, netbanking or card payment at the checkout.

Payment request processed by the PA: The payment request made by the customer is processed by the payment aggregator using the appropriate bank or network.

Bank authorisation: The payment request is sent to the bank to verify the transaction and then either approve it or decline it.

Settlement to merchant: Once the payment is approved by the bank, it is then settled into the merchant's account by the payment aggregator within a defined timeframe(usually T+1 or T+2 days).

Merchant onboarding process for payment aggregator

Here is how the payment aggregator onboarding process looks for merchants:

Sign-up and KYC: Businesses submit documents such as PAN, GST details, and bank account information for verification.

API or Plugin Integration: Developers integrate payment APIs or use plugins for platforms like Shopify or WordPress.

Live website & Start Accepting Payments: Once approved, businesses can start accepting payments across multiple channels.

What are the key features of payment aggregators in India?

The following are a few important key features of the payment aggregators in India:

Multiple Payment Options (UPI, Cards, Wallets, Net Banking)

Payment aggregators support a wide range of payment methods, ensuring customers can pay using their preferred mode. In India, UPI dominates, but cards and wallets still play a crucial role.

Quick Onboarding & Minimal Documentation

Unlike traditional banking systems, payment aggregators simplify onboarding, which makes it easier for startups and freelancers to get started quickly.

Dashboard & Real-Time Reporting

Most payment aggregators provide a centralised dashboard. This helps businesses in tracking transactions, making settlements, refunds, and analytics in real time.

Developer-Friendly APIs & Integrations

APIs allow seamless integration with websites, mobile apps, and SaaS platforms. This helps businesses with automation and scalability.

Security & Fraud Prevention

Payment aggregators follow strict compliance standards such as PCI-DSS, and they use encryption to ensure safe transactions.

Recurring Payments & Subscription Support

Essential for SaaS businesses and subscription-based models, allowing automated recurring billing.

International Payment Support

Some payment aggregators in India support cross-border payments. Although this is limited, expensive, and comes with poor FX rates, it is an important limitation for Indian freelancers and exporters.

Payment Aggregator vs Payment Gateway: What’s the Difference?

Both payment aggregators and payment gateways enable businesses to accept online payments. Although they operate very differently in terms of infrastructure, responsibility, and complexity.

A payment gateway is primarily a technology layer that securely transfers payment data. On the other hand, a payment aggregator is a full-stack solution that handles onboarding, processing, and settlement of funds.

Key Differences Explained

Ownership of Merchant Account

Payment aggregators allow businesses to operate under a shared merchant account. This eliminates the need to open a separate account with a bank.

In contrast, a payment gateways usually require businesses to have their own merchant account.

Role in Transaction

A payment gateway only facilitates the transfer of payment data between the customer, merchant, and bank.

A payment aggregator, however, handles the entire transaction lifecycle, which includes fund collection and settlement.

Ease of Setup

Payment aggregators are much easier to set up and are ideal for startups and SMEs.

Payment gateways often involve more complex banking relationships and approvals.

Compliance & Responsibility

Payment aggregators take on compliance and regulatory responsibilities on behalf of merchants.

And in the case of payment gateways, much of this responsibility lies with the business itself.

Comparison Table: Payment Aggregator vs Payment Gateway

Feature | Payment Aggregator | Payment Gateway |

Definition | Full-stack solution to accept and process payments | Technology layer to transfer payment data |

Merchant Account | Shared account provided | Separate merchant account required |

Role | Handles processing + settlement | Only routes transaction data |

Setup Time | Quick onboarding | Longer setup |

Compliance | Managed by aggregator | Managed by business |

Best For | Startups, freelancers, SMEs | Large enterprises |

Different Types of Payment Aggregators in India

Payment aggregators in India can be categorised based on their use cases and capabilities.

Domestic Payment Aggregators

These platforms focus on enabling payments within India. It can be done using UPI, cards, and net banking.Cross-Border Payment Aggregators

These enable businesses to accept payments from international customers. This often comes with higher fees and FX markups.Industry-Specific Aggregators

Some payment platforms are designed specifically for SaaS, freelancers, or eCommerce businesses.

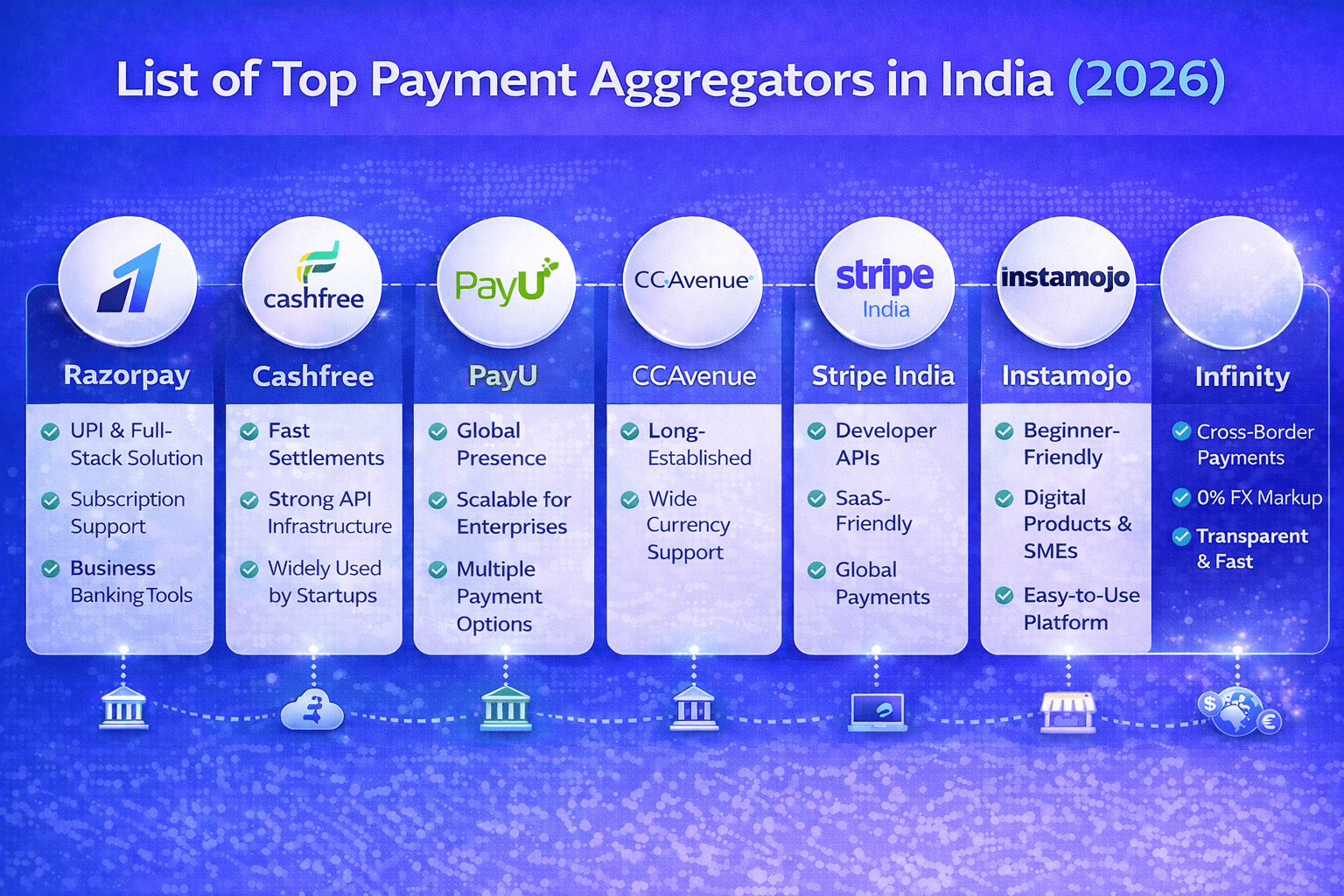

List of Top Payment Aggregators in India (2026)

Here is the list of some of the most popular payment aggregators used by businesses in India:

Razorpay

Razorpay in India is one of India’s leading payment aggregators. Razorpay offers a full-stack solution with support for UPI, cards, subscriptions, and business banking tools.

Cashfree

Cashfree is known for fast settlements and strong API infrastructure. Cashfree is widely used by startups and growing businesses.

PayU

It is a global payment solutions provider with a strong presence in India. PayU offers a scalable solution for enterprises.

CCAvenue

One of the oldest players in the market, CCAvenue is known for supporting a wide range of payment options and currencies.

Stripe India

Stripe India is popular among developers and SaaS companies in India. Stripe offers robust APIs and global payment capabilities.

Instamojo

Instamojo is a beginner-friendly platform designed for small businesses and freelancers.

Infinity

Even though Infinity is not a traditional payment aggregator, it is built specifically for Indian freelancers, exporters, and agencies dealing with international clients. It focuses on solving cross-border payment inefficiencies such as high FX markups, slow settlements, and limited transparency, which makes it a strong alternative for global payments.

Best Payment Aggregator for Your Business Type

There’s no one-size-fits-all option when it comes to choosing the best payment aggregator in India. The right choice depends on your business model, customer geography, and how you receive payments.

Here’s a more practical way to look at it:

If you’re a startup selling in India → Razorpay or Cashfree

Razorpay and Cashmere platforms offer quick onboarding, strong integrations, and support for all major Indian payment methods. This makes them ideal for early-stage businesses.If you’re a freelancer working with both Indian and international clients → Razorpay + Infinity

Razorpay works well for domestic collections. On the other hand, Infinity helps in optimising international payments with better FX rates and faster settlements.If you’re primarily dealing with international clients → Infinity

Traditional payment aggregators often fall short on cross-border efficiency. Infinity is built specifically for global payments.If you’re building a SaaS product → Stripe or Razorpay (Subscriptions) + Infinity

Stripe is ideal for global SaaS businesses due to its APIs and subscription support. Infinity helps reduce losses on international collections by saving on FX markup and transaction fees.If you’re an exporter or agency → Infinity + PayU / CCAvenue

Platforms like PayU or CCAvenue can help with regular collections. Infinity ensures you receive better value through transparent FX and faster settlements.If you’re a D2C or eCommerce brand → Razorpay or Cashfree

These platforms offer high success rates, easy integrations, and support for multiple payment methods within India.If you’re just starting and want a no-code solution → Instamojo

Instamojo supports easy setup and payment links. This makes it ideal for individuals and small businesses.If your business is scaling globally → Stripe + Infinity

Stripe handles global checkout experiences, while Infinity ensures efficient fund collection and conversion.

In most cases, businesses today don’t rely on just one platform; they usually combine tools to optimise both domestic and international payment flows.

Challenges with Payment Aggregators in India

Payment aggregators in India have a simplified digital payment system. But still, they come with certain limitations. This is especially for businesses that are scaling or working with international clients-

High transaction costs, especially for international payments

As we all know, domestic transactions are relatively affordable. But international payments often come with significantly higher charges. These include transaction fees, currency conversion markups, and hidden costs that directly impact your profit margins.Delayed settlement cycles

Most payment aggregators follow a T+1 or T+2 settlement cycle. This may work for some businesses, but it can create cash flow challenges for freelancers, exporters, and small businesses that rely on faster access to funds.Limited optimisation for cross-border payments

Most payment aggregators in India are built primarily for domestic transactions. As a result, international payment flows often feel like an add-on rather than a core feature.Complex dispute and refund handling

Chargebacks and refunds can sometimes take longer to process. Due to this, businesses may not always have full visibility into the process.Integration limitations for specific use cases

Even though API exists, not all platforms are equally flexible or tailored for niche business models like SaaS, agencies, or exporters.

Is There a Better Alternative to Payment Aggregators in India?

The problem with traditional payment aggregators is that, as long as your business operates within India, payment aggregators work well. But the moment you start dealing with international clients, the cracks begin to show up.

Businesses in India dealing with foreign clients often struggle with:

High FX markups that silently eat into profits

Delayed cash settlements that affect the cash flow

Lack of transparency during currency conversion

This creates a gap for freelancers, exporters, and agencies who rely heavily on cross-border payments.

Introducing a Smarter Alternative for Global Payments: Infinity

This is where Infinity comes in. Infinity is not positioned as a traditional payment aggregator. Instead, Infinity is built specifically to solve the challenges Indian businesses face when receiving international payments.

How Infinity Solves These Problems

Infinity focuses on optimising the entire international payment experience. Starting from receiving funds to converting and settling them.

Better and transparent FX rates

Unlike traditional platforms that include hidden markups, Infinity offers more competitive and transparent exchange rates. This helps businesses in retaining more of their earnings.Faster settlement cycles

Infinity offers quicker access to funds. Due to this, businesses can manage cash flow more efficiently without waiting for extended settlement timelines.Multi-currency support

Infinity enables businesses to receive payments in multiple currencies. This makes it easier for them to work with global clients.Built for freelancers, exporters, and agencies

The platform is designed keeping in mind real-world use cases. So, whether you're invoicing a client in the US or receiving payments from Europe, Infinity handles it all.Simplified international collections

Instead of dealing with complex banking processes or fragmented tools, Infinity offers a streamlined experience.

The Bottom Line

Payment aggregators are great for getting started. But as your business grows globally, you need solutions that are built for international scale, transparency, and efficiency.

Conclusion: Choosing the Right Payment Solution in India

Payment aggregators have played a crucial role in simplifying digital payments in India. They offer convenience, scalability, and ease of use. This makes them a go-to solution for many businesses.

However, as your business grows—especially globally—it’s important to evaluate whether a traditional payment aggregator is enough.

The right choice ultimately depends on:

Your customer base (domestic vs international)

Transaction volume

Cost sensitivity

Need for global expansion.

FAQs on Payment Aggregators in India

What is a payment aggregator?

A payment aggregator is a platform that enables businesses in India to accept online payments from their clients without a separate merchant account.

Is Razorpay a payment aggregator?

Yes, Razorpay is one of the leading payment aggregators in India.

Are payment aggregators in India regulated by the RBI?

Yes, all payment aggregators in India must comply with RBI guidelines. Any payment aggregator needs a proper license to operate in India.

What are the common fees charged by payment aggregators in India?

Payment aggregator fees typically include transaction charges, MDR, and additional costs for international payments.

![9 Best Cross Border Payment Platforms in India [Based on Real User Reviews]](https://framerusercontent.com/images/ZOzvHCU1ezQxfPmG2hFSGdvRrWE.png?width=1536&height=1024)