Discover infinity

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

When you start searching for ways to receive GBP payments in India, you’re likely to stop at "PayPal" or "Wise." But that is not enough if you are running a business or freelance practice in India.

When a UK client sends you GBP, there are a lot of things that happen simultaneously.

Firstly, the payment travels across regulated banking rails.

After that, it gets converted to INR at a rate that may or may not be disclosed to you upfront.

In this process, fees are deducted at one or more points in the chain. After the amount reaches your platform or bank account, the bank or payment platform generates documentation that is needed by you for FEMA compliance.

If you get any one of these wrong, like choosing a platform with no FIRC support, or accepting a payment into someone else's account, or using the wrong purpose code, you are not just losing money. But also, you are creating a compliance gap.

This blog covers all 7 safest ways to accept GBP payments and explains which one is right for your use case.

Best Way to Receive GBP Payments in India (2026)

If you need to act fast, here is the short version:

Best Option | Use Case |

Infinity | Best overall for freelancers, agencies, and exporters |

Virtual GBP account | UK clients who prefer domestic transfers |

Payoneer | Marketplace payouts (Upwork, Fiverr, Amazon) |

PayPal | Client familiarity (despite high cost) |

SWIFT wire | Large B2B bank-to-bank transfers |

Stripe / Razorpay / Cashfree | SaaS subscriptions and online checkout |

Wise | Transparent FX, simpler compliance needs |

Want to know how much exactly you will receive in INR on your next GBP invoice? Use Infinity’s live GBP calculator: tools.infinityapp.in/currency-converter/gbp-to-inr

What Is the Safest Way to Receive GBP in India?

"Safe" means two things: you receive the money reliably, and you receive it in a way that creates no compliance problems down the line.

The safest method combines all of the following:

Regulated payment rails — not informal channels, not cryptocurrency, not third-party accounts.

Clear KYC — both your identity and your client's payment are verified.

Transparent fee and FX disclosure — you know the rate before you agree to the payment.

Correct purpose code — matched to the nature of your export

FIRA/FIRC support — documented proof that foreign exchange entered India legitimately.

Invoice and payment trail — invoice, transaction ID, INR credit, and rate all reconcile.

Direct settlement to your own Indian bank account —it should not be a third-party wallet.

Clean tax records — GST treatment, LUT filing, income tax declaration.

Infinity checks all of these boxes by design. SWIFT does too, but with more manual effort and higher total cost. Wise checks most of them for smaller, simpler transactions.

What Documents Do You Need to Receive GBP in India?

Before you choose a payment method, make sure you can produce and maintain the following:

PAN and GST Details: PAN and GST details are required for tax filing and platform KYC. If you have a GST-registered number, then your GSTIN is needed for zero-rated export classification.

Purpose Code: RBI has made purpose codes important for every foreign remittance. Some of the common codes include: P0802/P0803 for software/IT services, P0805 for consulting. Your bank or platform will ask for this.

FIRA / FIRC / e-FIRC: Your bank or platform issues this after receiving the remittance. It is your proof that foreign exchange entered India through a legitimate channel. Platforms like Infinity provide this as part of their compliance workflow. SWIFT transfers require you to request them manually from your bank.

LUT (Letter of Undertaking): If you are GST-registered and want to invoice without charging IGST (zero-rated without tax payment), file an LUT with your GST authority at the start of each financial year.

Payment Advice or Transaction Reference: This is a transaction number that acts as a confirmation from your clients showing that the payment was sent.

Accounting Record: Log the GBP invoice amount, INR credited, conversion rate, and fees for every payment. This is your reconciliation trail for GST, income tax, and any future audit.

7 Safe Ways to Receive GBP Payments in India

Features | Infinity | SWIFT Bank Wire | Virtual USD Account | Wise | PayPal | Payoneer | Payment Gateways |

|---|---|---|---|---|---|---|---|

Direct USD client invoicing | ✓ | ✓ | ✓ | ✓ | – | – | ✕ |

Local payment experience for US clients | ✓ | ✕ | ✓ | ✓ | ✓ | ✓ | ✓ |

FIRA / FIRC support | ✓ | ✓ | – | – | ✕ | – | – |

Purpose code / GST workflow | ✓ | – | – | – | ✕ | – | ✕ |

Transparent pricing | ✓ | ✕ | – | ✓ | – | – | – |

Low total cost for recurring USD invoices | ✓ | ✕ | – | – | ✕ | – | ✕ |

FX markup risk | Low | High | Medium | Low to medium | High | Medium | Medium to high |

Settlement speed to Indian bank | Fast | Slow | Medium | Medium | Medium | Medium | Medium |

Good for large one-time payments | ✓ | ✓ | – | – | ✕ | ✕ | ✕ |

Good for marketplace income | ✕ | ✕ | ✕ | – | – | ✓ | ✕ |

Good for card payments/checkout | ✕ | ✕ | ✕ | ✕ | ✓ | ✕ | ✓ |

Client trust and familiarity | – | ✓ | – | ✓ | ✓ | ✓ | ✓ |

Main limitation | Not meant for B2C checkout or marketplace payouts | High hidden cost, slow settlement, and manual paperwork | Compliance support varies by provider | India-side business and compliance workflow may not suit every exporter | Very expensive for larger invoices; account holds possible | Better for marketplaces than direct client invoices | Better for checkout, not invoice-based USD receivables |

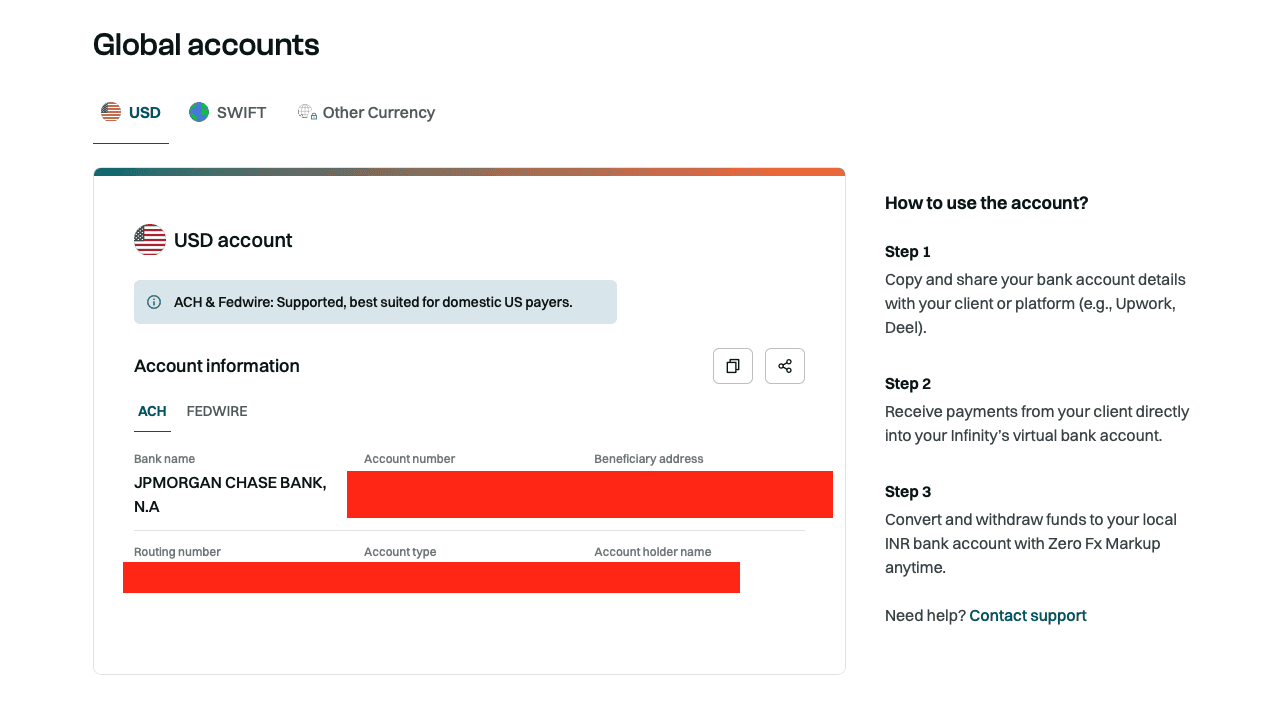

1. Infinity

Best for: Freelancers, agencies, consultants, exporters, and SaaS businesses that invoice UK clients directly

Infinity is built specifically for Indian businesses and professionals receiving international payments. Infinity helps Indian professionals receive international payments in 50+ currencies and across 160+ countries in a seamless way.

How it works:

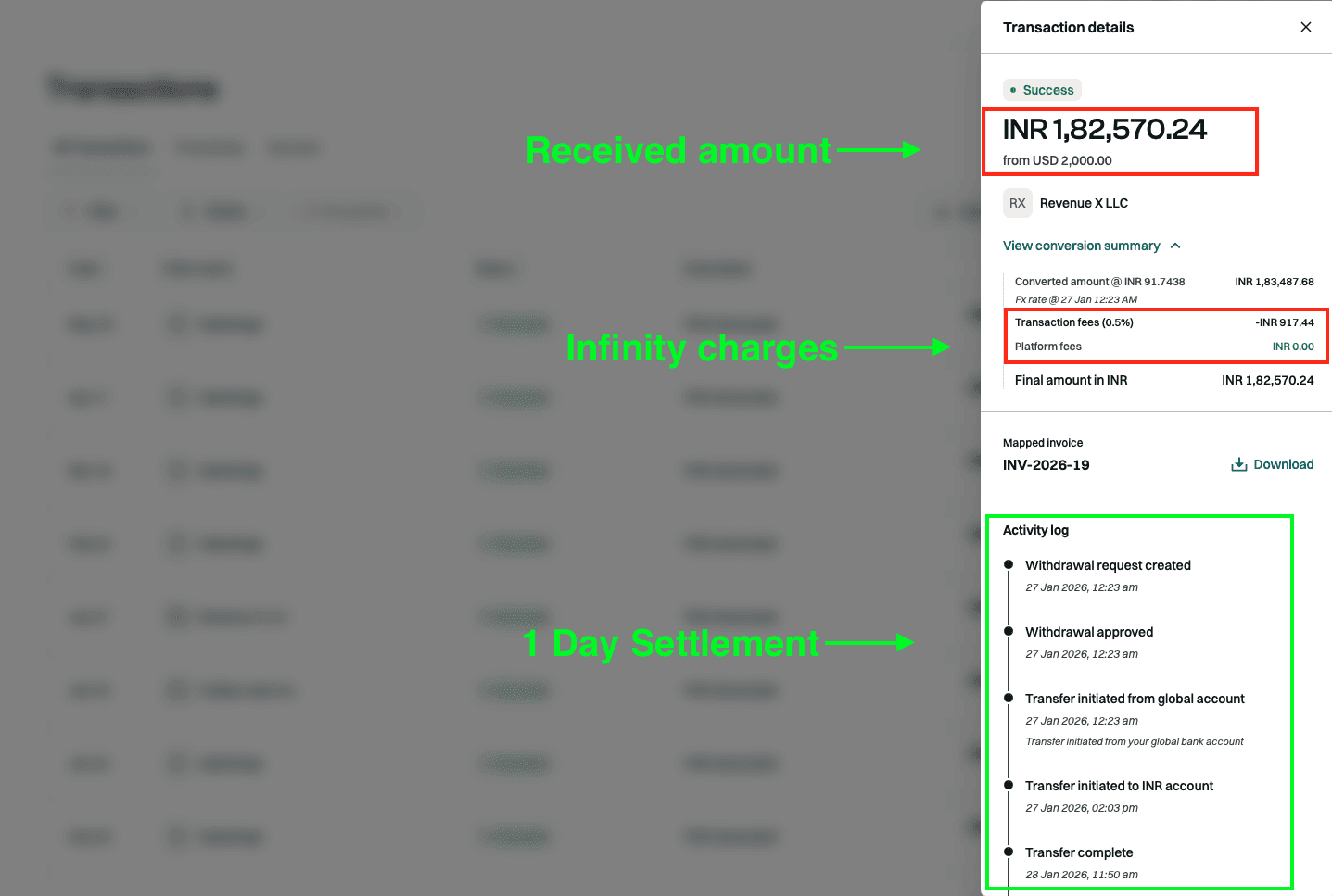

Infinity provides you with a local virtual multicurrency account. Your clients based in the UK can pay you in GBP, like a domestic transfer for them. Your GBP payment lands in the virtual account provided by Infinity.

And then the payment is settled into your Indian bank account within 24 hours. The whole process of receiving and settling your GBP payment into INR is regulated by FEMA and RBI compliance.

Infinity provides you with instant and free-of-cost FIRA for every successful transaction.

What makes it different for Indian exporters:

0.5% all-inclusive transaction fee — no hidden FX markup on top of the conversion rate

Zero FX markup positioning — the rate you see is close to the live mid-market rate

Faster settlement — 24-hour INR settlement for eligible transactions

Automated compliance workflow — Instant FIRA is provided for every successful transaction.

Purpose code and GST support — built into the onboarding and payment flow

Built for the Indian market — freelancer/exporter/agency context is the core use case, not an afterthought

Limitation to note:

Infinity is optimised for invoice-based B2B and not for B2C receivables. For consumer checkout widgets or marketplace payout integration, other options on this list are more appropriate for those specific use cases.

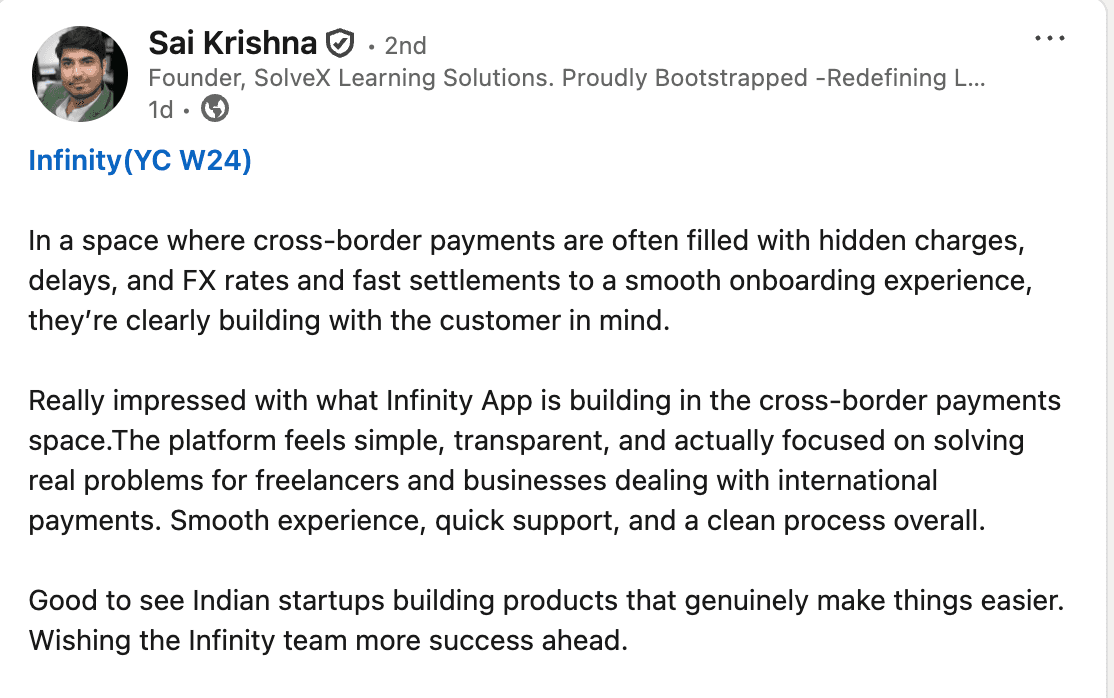

Source: LinkedIn

2. Direct Bank Wire Transfer Through SWIFT

Best For: SWIFT works best for large B2B payments, if the clients prefer traditional wire transfers, or for exporters who have established good banking relationships.

SWIFT is the oldest and original mode of international transactions. It is still preferred for large B2B transactions, where the exporters or businesses have established a good banking relationship. In the SWIFT transfer, when a payment is initiated from a bank in the UK, it travels through multiple intermediaries before it reaches your Indian bank account. Due to this complex process, there are multiple intermediary fees and other FX markups hidden in the process.

Strengths:

SWIFT is universally accepted and understood by most of the banks in the world.

Regulated and traceable with a full audit trail

Bank-issued FIRC for every inward remittance

No third-party platform dependency

Limitations:

The settlement time usually takes 2-5 business days.

Intermediary banks often charge $15–$30 per bank, which is deducted from the principal amount.

FX markup on conversion is rarely disclosed upfront — typically 1.5–3% above mid-market rate.

Incoming wire charge at the Indian bank side — often ₹500–₹2,500

Manual follow-up is required to get FIRC documentation in many cases.

Real-world example: On a £5,000 wire, the wire fee your client pays may appear small. But accounting for correspondent bank deductions, your Indian bank's FX spread, and the incoming charge, you could receive ₹12,000–₹25,000 less than the mid-market rate would suggest.

When SWIFT makes sense: SWIFT payment makes sense for large, infrequent payments (£20,000+) with clients who prefer wire and when you already have an existing banking relationship. For regular invoices under £10,000, newer payment platforms are more economical than SWIFT.

3. Virtual GBP Account

Best for: Virtual GBP accounts work best for contractors, freelancers with recurring UK clients, and businesses who want a local payment experience for UK clients.

There are several payment platforms in India, like Infinity, Skydo, and Xflow, that allow Indian professionals to get a virtual GBP account with an account number and sort code. Your client pays as if they are paying a UK supplier.

They use the domestic UK bank transfer rails (Faster Payments). You can later withdraw or settle the balance to your Indian account in INR.

How it works:

You share UK-style account details with your client. They initiate a domestic GBP bank transfer, cheap and instant from their side. The platform holds the GBP balance, and you choose when to convert and withdraw to India.

Why this matters:

Many UK clients, especially smaller businesses and individual contractors, are reluctant to initiate international wires. This is due to higher charges and slower settlement time. A virtual UK account removes that friction entirely. From their perspective, they are making a local payment. From yours, you are receiving GBP through a compliant channel.

Safety note:

The platform providing your virtual account must be properly licensed, must perform KYC on incoming payments, and must support Indian compliance documentation (FIRA/e-FIRC) at the time of settlement. Not all virtual account providers cover this adequately for Indian exporters. Confirm documentation support before using any platform for business-grade GBP receivables.

4. Wise

Best for: Users prioritising transparent FX pricing, occasional GBP transfers, clients who are already on Wise

Wise (formerly TransferWise) built its reputation on transparent, near-mid-market exchange rates and visible fee disclosures before you confirm a transfer. For many individual freelancers and remote workers, it is a familiar and trusted option.

Strengths:

Clear fee disclosure before payment is sent.

Conversion rate is typically close to mid-market, with a small transparent percentage fee.

Widely trusted by global clients.

Multi-currency account available

Limitations:

Business account availability and feature depth for India can vary — confirm current status before setting this up for regular client invoicing.

Documentation workflow (e-FIRC, purpose code matching) may not be sufficient for every Indian exporter's compliance needs

Less suited to high-volume B2B export compliance scenarios

Customer support for complex India-specific compliance situations is not a core strength.

When Wise makes sense:

For a freelancer receiving occasional GBP payments from a UK client who is already on Wise, and where compliance documentation is straightforward.

For an agency with recurring large invoices and strict FEMA/GST documentation requirements, verify whether Wise's India-side compliance workflow covers everything you need.

5. PayPal

Best for: One-off payments, clients who insist on PayPal, small transactions where client convenience matters more than cost efficiency

PayPal is the most globally recognised name in online payments, and your UK client almost certainly has an account. That familiarity is its main asset.

Strengths:

Instant payment link or email invoice workflow

No learning curve for the client

Widely accepted for small amounts and one-off transactions.

Dispute resolution process for buyer/seller protection

Limitations:

High transaction fees: typically 3.5–4.4% plus a fixed fee for cross-border payments

FX markup on GBP to INR conversion: PayPal adds approximately 3–4% above the mid-market rate

Combined cost (transaction fee plus FX spread) can exceed 7–8% of the payment amount.

Account holds and payment reviews are common on Indian accounts, especially for large amounts.

Documentation for Indian export compliance (FIRA/purpose codes) is limited.

My honest assessment:

PayPal is safe and familiar, but it is consistently the most expensive method on this list for Indian exporters when the total cost is measured. On a £5,000 invoice, you could lose £350–£400 to fees and FX spread versus what Infinity would cost. Use PayPal when your client insists, but price it into your invoice.

6. Payoneer

Best for: Payoneer works best for freelancers and professionals receiving payments from marketplaces like Upwork, Fiverr, Amazon, or Toptal.

Payoneer's core strength is marketplace integration. Payoneer is the most natural and frictionless method of receiving international payments if your payments come through marketplaces.

Strengths:

Payoneer’s deep integrations with major freelance and commerce marketplaces

You receive multi-currency receiving accounts in USD, EUR, GBP, and more.

It is widely used and understood across the Indian freelancer community.

It charges a reasonable fee for marketplace-sourced income.

Limitations:

Fees and FX spread on withdrawal to an Indian bank account can add up — typically 2–3% combined.

Account holds and customer support escalation paths can be frustrating for Indian users.

For direct client-to-freelancer invoicing (no marketplace involved), Payoneer is less competitive than Infinity on total cost.

India-specific compliance documentation, like FIRA/FIRC, should be verified before using it for high-invoice payments.

When Payoneer makes sense:

If the majority of your GBP income comes through a marketplace that integrates with Payoneer, use it. For direct client billing, compare the total cost carefully before defaulting to it.

7. Payment Gateways like Stripe

Best for: SaaS businesses, ecommerce operators, subscription products, and any business needing card-based checkout

This category works differently from invoice-based methods. A payment gateway processes card transactions at the point of checkout, the customer enters their card details on your website or app, and the money is settled to your Indian account.

Stripe is widely used by Indian SaaS founders for international card acceptance. Razorpay is India's largest payment gateway with international card options. Cashfree is a strong alternative with local support.

Strengths:

Card acceptance: credit, debit, and international cards

Stripe allows recurring and subscription billing.

Developer-friendly APIs and checkout SDKs

Limitations:

International card transaction fees are high, typically around 2.9–3.5% plus currency conversion fees.

These are checkout tools, not invoice tools — they do not replace invoice-based GBP receivables for B2B clients.

Eligibility and onboarding depend on your business category.

Export compliance documentation is not designed around FEMA/FIRC workflows.

When to use gateways:

If you run a SaaS product and your UK customers pay by card on your website, use a gateway. If you are a freelancer or agency invoicing a UK business, a gateway is not the right tool for that job.

Cost Comparison: How Much INR Do You Actually Receive?

Let's use a £5,000 GBP payment as the baseline. The numbers are approximate figures, and they can vary by date, volume, and account type.

Method | Visible Fee | FX Markup | Settlement | FIRA/FIRC | Approx. Impact on £5,000 |

Infinity | 0.5% | 0% | ~24 hours | Supported | Highest — use live calculator |

Bank SWIFT | Fixed + charges | 1.5–3% typical | 2–5 days | Manual FIRC | ₹12,000–25,000 less |

Wise | ~0.5–0.8% | Transparent, near mid-market | 1–2 days | Route-specific | Competitive |

Payoneer | 1–2% | ~1.5–2% spread | 2–3 days | Varies | Mid |

PayPal | 3.5–4.4% + fee | ~3–4% markup | 1–3 days | Limited | Often lowest |

Stripe/Gateway | 2.9–3.5% | Conversion spread | 2–7 days | Not designed for it | N/A for invoice receivables |

For a live INR figure based on today's rate: https://tools.infinityapp.in/currency-converter/gbp-to-inr

The key insight: FX markup is where most platforms quietly take the largest share. A 3% FX spread on £5,000 costs £150, which is more than most visible transaction fees.

Before receiving any international payment, you should compare the total cost of the transaction and not just the headline/visible cost.

Which Method Should You Choose?

Your Situation | Best Option | Why |

Freelancer billing UK clients directly | Infinity | Low total cost, fast INR settlement, compliance support |

Freelancer on Upwork / Fiverr / Toptal | Payoneer | Marketplace integration is seamless |

Agency billing UK clients on an invoice | Infinity | Invoice workflow, settlement, FIRA, payment tracking |

Exporter of goods or services | Infinity or SWIFT, depending on volume | Documentation and FEMA-compliant realization |

SaaS company with UK subscribers | Stripe/Razorpay for checkout; Infinity for invoices | Different payment jobs need different tools |

Remote contractor wanting easy UX for UK client | Virtual GBP account | Client pays domestically; you receive INR |

Client insists on PayPal | PayPal | Accept it; factor cost into your pricing |

Occasional freelancer, small amounts | Wise | Transparent, simple, no heavy setup |

What Is the Safest Way to Receive GBP in India?

"Safe" means two things: you receive the money reliably, and you receive it in a way that creates no compliance problems down the line.

The safest method combines all of the following:

Regulated payment rails: not informal channels, not cryptocurrency, not third-party accounts.

Clear KYC: both your identity and your client's payment are verified.

Transparent fee and FX disclosure: you know the rate before you agree to the payment.

Correct purpose code: matched to the nature of your export

FIRA/FIRC support: documented proof that foreign exchange entered India legitimately.

Invoice and payment trail: invoice, transaction ID, INR credit, and rate all reconcile.

Direct settlement to your own Indian bank account; it should not be to a third-party wallet.

Clean tax records: GST treatment, LUT filing, and income tax declaration.

Infinity checks all of these boxes by design. SWIFT does too, but with more manual effort and higher total cost. Wise checks most of them for smaller, simpler transactions.

Mistakes to Avoid When Receiving GBP in India

Accepting business payments into a personal savings account or someone else's account creates FEMA violations and makes documentation impossible.

Ignoring purpose codes - your bank or platform will ask for one. The wrong code (or no code) can delay payment and create compliance flags.

Not collecting FIRA/FIRC - many freelancers only realise they need it when their CA asks for it at tax time. Getting it retrospectively from a bank can take weeks.

Comparing only the transaction fee and ignoring the FX markup - a "1% fee" with a 3% FX spread costs you 4% total.

Choosing PayPal out of habit for serious B2B invoices, it is not wrong; it is just expensive. On recurring invoices, the cost compounds quickly.

Using crypto or stablecoins casually for business income, these typically lack the FEMA documentation trail required for compliance and income tax.

Not filing LUT when required, if GST-registered, not having an active LUT means charging IGST and claiming a refund, which is slower and more complex.

Not matching invoices with payments, each INR credit should match a specific GBP invoice. Mismatches cause problems at GST filing and IT assessments.

Ignoring GST/tax treatment on foreign income, export of services can be zero-rated, but that requires the right documentation, purpose coding, and LUT filing.

Frequently Asked Questions

Do I need FIRA/FIRC for GBP payments?

Yes. FIRA (Foreign Inward Remittance Advice) is issued by your bank or payment platform for every inward foreign remittance. Platforms like Infinity provide these automatically, whereas with traditional banks, you are required to do manual follow-ups.

What is the cheapest way to receive GBP in India?

When total cost is measured, which includes visible fee plus FX markup plus settlement charges, Infinity at 0.5% all-inclusive with zero FX markup is currently the most cost-efficient option for direct client invoice payments.

Is PayPal good for receiving GBP in India?

PayPal is familiar and safe for receiving GBP payments in India. But it is the most expensive option on this list for regular business income. Total cost (transaction fee plus FX conversion markup) typically runs 7–8% per payment. It is acceptable for occasional or one-off payments where client convenience is the priority.

Is Payoneer safe for Indian freelancers?

Yes, Payoneer is a legitimate and generally safe option for Indian freelancers. It is particularly well-suited for freelancers who receive payouts through integrated marketplaces like Upwork, Fiverr, and Amazon. For direct client billing without a marketplace, you should compare its total cost with Infinity before making it your default payment method.

What is the best way for agencies to receive GBP from UK clients?

For agencies invoicing UK clients, Infinity is the strongest all-round option. It offers low cost, fast settlement, FIRA compliance documentation, and clean B2B invoicing.

What documents are needed to receive GBP payments in India?

At minimum: a commercial invoice, client agreement or work order, PAN (and GSTIN if registered), bank account details for settlement, purpose code for the remittance, and FIRA/FIRC from the platform or bank is needed to receive GBP payments in India. If you are GST-registered and exporting services zero-rated, you also need an active LUT filing for the current financial year.