Discover infinity

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

If you are a freelancer, agency, exporter, consultant, SaaS founder, or remote contractor in India, receiving international payments in USD, then it is not just about choosing the fastest app.

You will have to think about the fees, FX markup, settlement time, documentation like FIRA/FIRC, purpose codes, GST/LUT filing, and clean tax records.

It's not that the wrong choice will cost you money on every transaction. It's just that it can leave you without any proper documentation at the end of the financial year.

It can create compliance gaps with FEMA regulations and make reconciliation painful.

This blog will compare the 7 most safest ways to receive USD payments in India. It explains exactly when each method makes sense, and shows how much INR you are going to receive after fees and conversion.

Best & Safest Way to Receive USD Payments in India

Infinity - RBI Approved Framework, 1 Day Settlement, and 0% FX Markup. It fits best for Indian freelancers, consultants, agencies, and exporters.

ACH (Virtual USD Account) - US clients who prefer domestic transfers

Your Situation | Best Option | Why |

Indian freelancer, agency, or exporter | Infinity | Low cost, compliance support, faster INR settlement |

US clients who prefer domestic transfers | Virtual USD Account (ACH) | Client pays like a US vendor |

Marketplace payouts (Upwork, Fiverr) | Payoneer | Deep marketplace integrations |

Client insists on a familiar name | PayPal | Convenient, but expensive |

Large B2B bank wires | SWIFT | Regulated, but slow and cost-heavy |

SaaS or ecommerce checkout | Stripe / Razorpay / Cashfree | Card acceptance, subscriptions |

Transparent FX with simpler needs | Wise | Mid-market-style pricing |

Do you want to know how much you will receive in INR? Use Infinity's live USD to INR calculator: tools.infinityapp.in/currency-converter/usd-to-inr

What Is the Safest Way to Receive USD in India?

The safest method is not the one with the lowest headline fee. Safety for Indian USD recipients means all of the following, together:

Regulated payment rails — the platform is authorised and operates within the FEMA/RBI framework

Clear KYC — your identity and business are verified, reducing account hold risk

Transparent FX rate — you see the rate before the transaction, not after

Correct purpose code — inward remittance is reported with the right RBI purpose code

FIRA/FIRC support — the platform provides or supports documentation of inward remittances

Invoice and payment trail — every payment can be matched to an invoice

Direct settlement to your Indian bank account — funds land in your own account, not a third-party wallet.

Clean records for tax — INR amount, USD original, rate, fee, and date are all logged and downloadable

According to the above definition, Infinity is the strongest fit for most Indian freelancers, agencies, and exporters in 2026 who receive international payments in India. This is because compliance is built into its workflow rather than requiring any manual follow-ups.

Can You Legally Receive USD Payments in India?

Yes. Indian freelancers, businesses, exporters, consultants, and service providers can legally receive USD payments from foreign clients.

The payments must go through regulated banking or payment channels that comply with FEMA (Foreign Exchange Management Act) and RBI rules.

The key distinction is usually between legal compliance and low cost.

There are so many options available, but not every option gives the documentation needed at the time of GST filings or export realisation reporting.

What compliance requires in practice:

Payments must arrive through an RBI-authorised channel.

Your invoices must match each inward remittance.

For every inward remittance, the correct purpose code must be assigned (export of services, software exports, professional fees, etc.)

FIRA or FIRC (or e-FIRC) must be obtained for every international payment

GST treatment must be determined: if you export services under GST without paying IGST, you need to file a Letter of Undertaking (LUT)

All USD received must be reported correctly in your ITR and GST returns.

What Documents Do You Need to Receive USD in India?

This checklist is very important before the payment arrives in your account. These documents will protect you across tax filing, GST audits, export realisation records, and client disputes.

Commercial invoice — issued to the foreign client, in USD, with invoice number, date, description of services, and amount

Client agreement or work order — the contract or SOW that supports the invoice

PAN — mandatory for all income, TDS, and tax filing

GST registration — if your turnover crosses the threshold or you are voluntarily registered

Bank account / KYC details — for the receiving account with your bank or payment platform

Purpose code — RBI-defined code describing the nature of the inward remittance (e.g., P0802 for software services, P1004 for consulting)

FIRA / FIRC / e-FIRC — proof of inward remittance; issued by your bank or payment platform

LUT (Letter of Undertaking) — if you export services under GST without charging IGST on your invoice

Payment advice/transaction reference — the confirmation from the client's bank or payment platform

Accounting record — log of USD amount received, INR credited, exchange rate applied, platform fee, and net amount

7 Safe Ways to Receive USD Payments in India

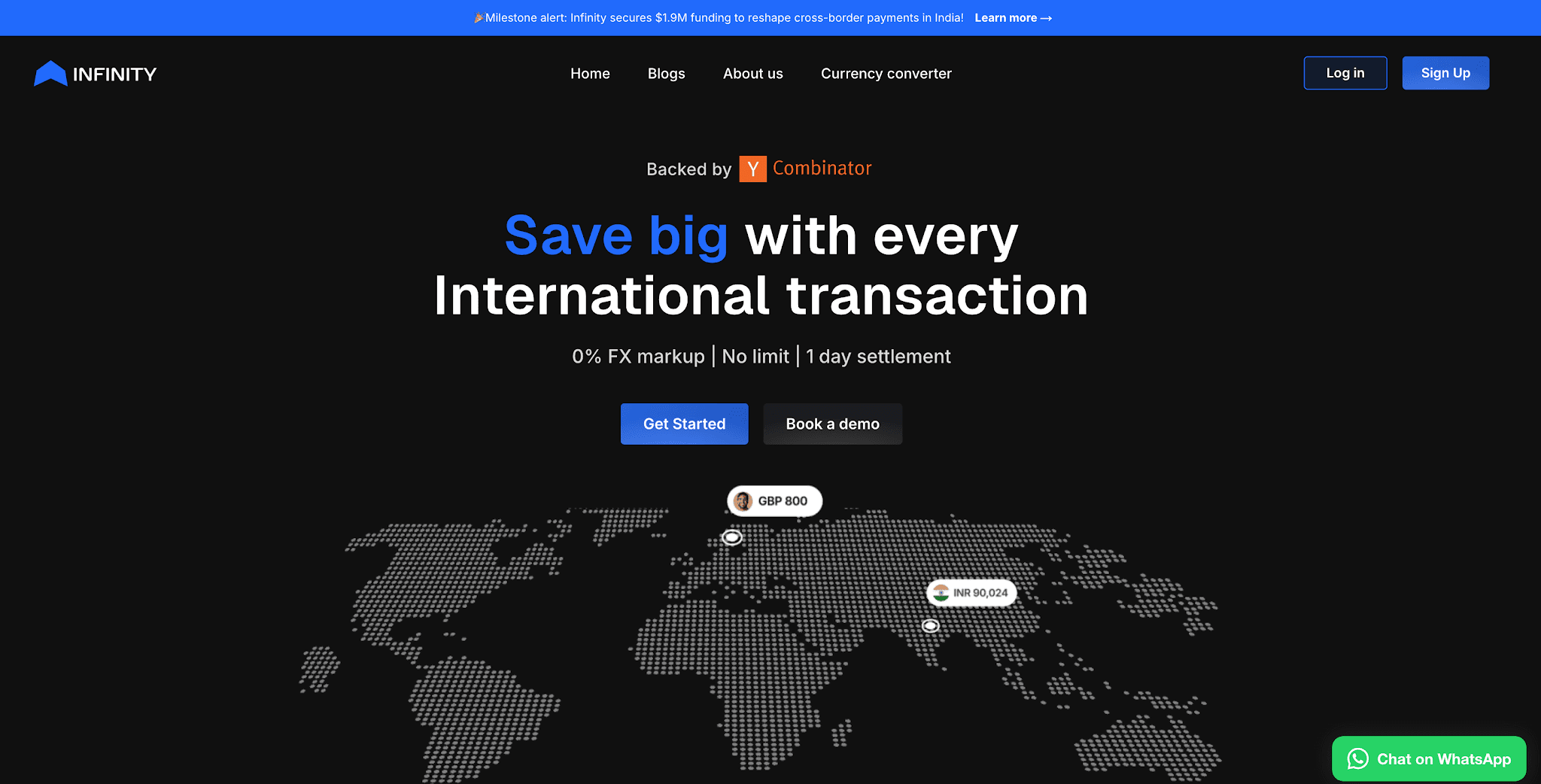

#1. Infinity: India-First Cross-Border Payment Platform

Best for: Infinity is best for freelancers, agencies, consultants, exporters, and SaaS/service businesses receiving international payments in India.

Infinity is built for Indian professionals and businesses receiving USD from international clients. The platform handles regulated international payment collection and INR settlement. This means that your client pays in USD and Infinity routes the payment through compliant channels before crediting INR to your Indian bank account.

What makes Infinity different from generic international platforms:

0.5% all-inclusive transaction fee — no hidden charges, split across a visible fee and a separate FX markup

Zero FX markup — the conversion uses a live rate, not an inflated internal rate that quietly reduces your payout

Faster INR settlement — typically within 24 hours once the payment clears

FIRA/compliance documentation support — automated workflow to help you collect the inward remittance records you need for tax and GST

Built for Indian export workflows — purpose codes, invoice matching, and documentation are part of the platform flow, not an afterthought

How it works in practice:

Your US client will receive a payment link or your Infinity payment details. They can pay in USD. Infinity processes the collection on compliant rails, converting the funds at the live rate, deducting 0.5%, and settling INR directly to your bank account. You can download your FIRA and match it to the invoice in your accounting records.

Cost illustration: On a $10,000 invoice, the difference between a 0.5% zero-markup platform and a 4.4% + FX markup platform can be ₹15,000–30,000 in your pocket on a single payment.

Who should consider Infinity: Any Indian freelancer, agency, or SaaS business currently losing 2–4% per transaction to FX markup plus fees on platforms like PayPal or legacy bank wires.

#2. Direct Bank Wire Transfer via SWIFT

Best for: SWIFTs work best for large B2B payments, exporters working with established banking relationships, and clients who are comfortable with international bank wires.

SWIFT is the original method for international USD transfers, and it remains widely accepted. When a foreign client sends you a wire to your Indian bank account, the transfer routes through the SWIFT network. It can possibly have one or more intermediaries before it reaches your bank account.

Pros:

It is universally accepted by Indian banks.

FIRA/FIRC documents issued by banks are well-established

It is suited for larger volume transactions, where a fixed fee like transaction cost becomes proportionally smaller.

Cons:

Settlement time is longer than usual. Mostly 2-5 days.

Fees charged by intermediary banks are unpredictable. No one knows about the intermediary charges.

The bank applies a hidden fee of 1-3% as FX markup, which is not shown upfront.

Manual documentation follow-up requires calling your bank branch.

Real example:

On a $5,000 SWIFT wire, a visible receiving fee of ₹500–1,500 looks modest. But a 2% FX markup on $5,000 at ₹84/USD reduces your payout by approximately ₹8,400 compared to a zero-markup platform. Add correspondent bank charges of $25–50, and the actual loss is higher than the "small fee" your bank quotes.

SWIFT works best when: Your transaction is large enough to absorb fixed costs, and your client is a corporate buyer who is already using SWIFT.

#3. Virtual USD Account - ACH or Fedwire Receiving

Best for: ACH or Fedwire is best for remote contractors, freelancers with recurring US clients, and businesses that receive frequent USD payments from US-based clients.

There are several platforms that now offer Indian users a US virtual bank account. It comes with a US routing number and account number. Your American client pays you as if they are paying a US vendor. What they see is a domestic ACH or Fedwire transfer on their end. The platform then holds the USD and settles INR to your Indian account.

Why US clients prefer this:

Many US businesses find international wires bureaucratic. ACH transfers to a US account feel routine. This removes friction on the client side and can speed up payment significantly.

Key platforms offering this:

Infinity, Payoneer, Wise (where available), and several other cross-border platforms offer US virtual account details to Indian users.

What to verify before choosing a platform for virtual USD receiving:

Is the inward remittance FEMA-regulated?

Do you get FIRA/FIRC once the payment has been settled?

When converting USD to INR, is there any FX markup that has been applied?

Are there any withdrawal fees that have been applied?

Safety note: A virtual USD account is only as safe as the platform behind it. The account number your client sees belongs to the platform, not your Indian bank. Ensure the platform is reputable, regulated, and provides the compliance documentation Indian exporters need.

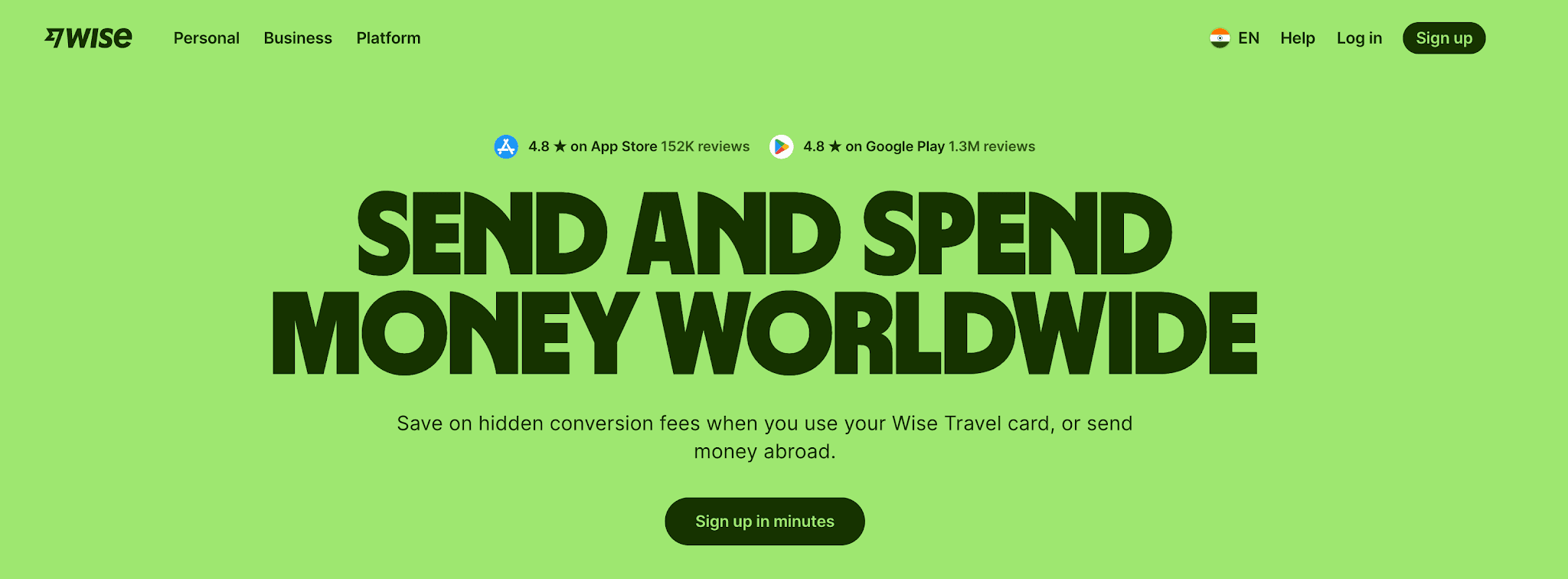

#4. Wise

Best for: Users who prioritise transparent FX pricing, simple client-to-freelancer transfers, and situations where heavy India-specific export documentation is not the primary concern

Wise (formerly TransferWise) built its reputation on transparent FX pricing. Unlike banks that embed their margin in an opaque exchange rate, Wise typically shows you the mid-market rate, the fee separately, and the amount your recipient will receive before you confirm.

Pros:

Transparent fee structure — you see the exchange rate and the fee before confirming.

Mid-market-style exchange rate with a small conversion fee, rather than a hidden markup

Strong global brand recognition; US and European clients are comfortable using it.

Multi-currency account features

Cons:

For Indian businesses, account availability can vary; not all features that are available to US or EU users are available to Indian users.

Documentation workflow for Indian export compliance (FIRA, purpose codes, LUT-related flows) may require additional manual steps.

Not always the best fit for high-volume B2B export with formal compliance requirements

When Wise makes sense:

You have straightforward client transfers, your compliance needs are manageable, and your client is already familiar with Wise. It is a solid option for individual freelancers with simpler setups.

#5. PayPal

Best for: One-off client payments, clients who insist on PayPal, creators and digital product sellers where convenience outweighs cost

PayPal is the most globally recognised name in online payments. If your client has only ever used PayPal, this may be your only option for that specific client relationship.

Pros:

Global client familiarity — almost every international buyer has a PayPal account

Simple payment link and invoice flow

Fast payment from the client's side

Cons:

High transaction fees — PayPal charges a percentage fee plus a fixed fee per transaction for cross-border payments

FX markup — PayPal's currency conversion uses a rate that includes a significant spread above the interbank rate

Combined cost (fee + FX markup) can reach 5–7% of the transaction value in practice.

Account holds and payment disputes can freeze funds without clear resolution timelines.

Not designed for serious recurring B2B USD income at scale

Limited export documentation support for Indian FEMA/GST compliance workflows

Bottom line on PayPal:

It is safe in the sense that it is a legitimate, regulated platform. But it is consistently the most expensive option on this list for Indian recipients, and the documentation it provides is not structured for Indian export compliance.

Use PayPal when your client absolutely insists, and the relationship value outweighs the higher cost. Do not use it as your default method for regular USD income.

#6. Payoneer

Best for: Marketplace payouts (Upwork, Fiverr, Amazon, Shutterstock), freelancers embedded in platforms that pay through Payoneer, users who need multi-currency virtual receiving details

Payoneer is the dominant payment infrastructure for global freelancing marketplaces. If you earn on Upwork, Fiverr, Amazon Marketplace, or similar platforms, then Payoneer is often the default or only withdrawal option available.

Pros:

Deep integrations with 2,000+ marketplaces and platforms globally

Multi-currency receiving accounts (USD, EUR, GBP) for direct client payments.

Widely accepted and trusted by platforms and enterprise clients

Prepaid Mastercard option for spending

Cons:

Fees and FX spread can accumulate: account fees, withdrawal fees, and currency conversion costs.

Customer support and account holds have historically been frustrating for some users.

For direct client billing outside marketplace contexts, the experience is less polished than purpose-built invoice platforms.

FIRA/compliance documentation for Indian export requirements requires manual coordination

When Payoneer is the right choice:

You are already on marketplaces that pay through Payoneer, or your clients are accustomed to Payoneer's Global Payment Service. For direct billing relationships outside marketplaces, compare total cost with alternatives before committing.

#7. Payment Gateways and Checkout Tools - Stripe, Razorpay, Cashfree

Best for: SaaS subscriptions, ecommerce products, digital downloads, online courses, and any business that needs a checkout or card payment experience

Payment gateways solve a different problem from invoice-based USD receivables. They let you accept card payments online, from any country, in multiple currencies, through a hosted checkout or API integration.

Stripe is widely accepted and globally trusted for card payments. Stripe is eligible to process payments in USD and settle in INR.

Razorpay and Cashfree are India-first gateways with strong local support. They integrate with UPI and NEFT for domestic payments, and for USD inbound payments, they integrate with international cards. They are easier to set up for Indian entities.

Pros:

Card acceptance (Visa, Mastercard, Amex) from international clients

Recurring billing and subscription management

Checkout API, payment links, and embeddable widgets

Cons:

Not a substitute for invoice-based USD receivables from B2B clients - a corporate US client will not pay a checkout page the way a consumer does

Usually, the card transaction fees are higher than the bank-to-bank transfer fees.

Not all Indian business entities are qualified immediately; there could be problems related to onboarding eligibility or account activation.

Documentation for export compliance may not be as clean as a dedicated cross-border receivables platform.

Who should use these:

SaaS companies with subscription products, ecommerce stores selling internationally, and course/digital product creators. If you are billing a US company for services on an invoice, these tools are not the right fit.

How Much INR Do You Actually Receive? (Cost Comparison)

This table compares estimated outcomes for three common invoice values. FX rate used: ₹84/USD (approximate). Use Infinity's live calculator for exact figures: tools.infinityapp.in/currency-converter/usd-to-inr

For a $1,000 USD Invoice

Method | Visible Fee | FX Markup | Est. INR Received | Settlement |

Infinity | $5 (0.5%) | 0% | ~₹83,580 | ~24 hours |

Bank SWIFT | $15–25 + bank charges | 1.5–2.5% | ~₹80,000–81,600 | 2–5 days |

PayPal | ~$44 (4.4%) | ~2.5% | ~₹76,200–78,000 | 1–3 days |

Payoneer | ~$20–30 | ~1–2% | ~₹80,000–82,000 | 2–3 days |

Wise | ~$10–15 | ~0.5% | ~₹82,500–83,000 | 1–2 days |

For a $5,000 USD Invoice

Method | Visible Fee | FX Markup | Est. INR Received | Settlement |

Infinity | $25 (0.5%) | 0% | ~₹4,17,900 | ~24 hours |

Bank SWIFT | $30–60 + charges | 1.5–2.5% | ~₹3,98,000–4,06,000 | 2–5 days |

PayPal | ~$220 (4.4%) | ~2.5% | ~₹3,78,000–3,85,000 | 1–3 days |

Payoneer | ~$100–150 | ~1–2% | ~₹4,00,000–4,08,000 | 2–3 days |

Wise | ~$50–75 | ~0.5% | ~₹4,12,000–4,14,000 | 1–2 days |

For a $15,000 USD Invoice

Method | Visible Fee | FX Markup | Est. INR Received | Settlement |

Infinity | $75 (0.5%) | 0% | ₹12,53,700 | ~24 hours |

Bank SWIFT | $50–100 + charges | 1.5–2.5% | ₹11,94,000–12,15,000 | 2–5 days |

PayPal | ~$660 (4.4%) | 2.5% | ₹11,34,000–11,55,000 | 1–3 days |

Payoneer | ~$300–450 | 1–2% | ₹12,00,000–12,20,000 | 2–3 days |

Wise | ~$150–225 | 0.5% | ₹12,36,000–12,42,000 | 1–2 days |

Note: All figures are estimates for illustration. Actual amounts vary based on live FX rates, intermediary deductions, and account-specific fee tiers.

Which Method Should You Choose?

Your Profile | Best Option | Reason |

Freelancer billing US clients directly | Infinity or Virtual USD account | Lower cost, easier client payment, better compliance documentation |

Freelancer on Upwork / Fiverr / Amazon | Payoneer | Marketplace integration is built-in |

Agency billing US corporate clients | Infinity | Invoice workflow, INR settlement, FIRA support |

Exporter of goods or services | Infinity or SWIFT, depending on the value and client | Compliance documentation, purpose code, and realization reporting |

SaaS business with subscription product | Stripe / Razorpay / Cashfree for checkout; Infinity for invoices | Different payment jobs require different tools |

Remote contractor with recurring US client | ACH-capable virtual USD account or Infinity | Client-side domestic ease + compliant India settlement |

Client insists on PayPal | PayPal | Convenience, despite higher cost, factor it into your pricing |

Client insists on bank wire | SWIFT | Establish a documentation process with your bank upfront |

Mistakes to Avoid When Receiving USD in India

1. Accepting business payments into someone else's account. Your FEMA compliance is tied to your own KYC. Receiving USD in a family member's or colleague's account creates tax and legal risk for both parties.

2. Ignoring purpose codes. Every inward remittance must have an RBI purpose code. Wrong or missing codes can create reconciliation issues when you file your returns.

3. Not collecting FIRA/FIRC. This is your proof that you received foreign currency. Without it, you cannot substantiate export income claims, GST refunds on zero-rated supplies, or respond to a tax notice.

4. Choosing PayPal just because it is familiar. Familiarity does not equal value. On a $5,000 monthly income, the difference between PayPal and a zero-markup platform can be ₹30,000–40,000 per year. Build that into how you quote or choose platforms.

5. Comparing only the transaction fee and ignoring the FX markup. Always look at the total cost of the transaction. This includes platform fees and conversion fees. Most professionals look up at the platform fees but tend to ignore the markup that could be there in the conversion fees.

6. Using crypto or stablecoins casually for business income. Receiving business income in crypto or stablecoins has FEMA, GST, and income tax implications that are not straightforward. It is not advised to use stablecoins for business income without proper professional advice.

7. Not filing LUT when required. If you export services under GST and want to issue zero-rated invoices without charging IGST, you must file an LUT at the start of each financial year. Missing this means you either charge IGST or lose refund eligibility.

8. Not matching invoices with payments. Every FIRA/FIRC must match a specific invoice. Unmatched remittances create problems during tax audits and FEMA scrutiny.

Step-by-Step: How to Receive USD Payments with Infinity

Create your Infinity account: sign up with your email and basic details.

Complete KYC: submit your PAN, Aadhaar, bank account details, and business documentation. This is mandatory for FEMA-compliant operations.

Generate your invoice or payment link: use Infinity's invoice tool or share your Infinity payment details with your client.

Client pays in USD: your US or international client completes the payment in USD via ACH, card, or wire, depending on the platform's options.

Track payment status: monitor the payment in your Infinity dashboard and see when it clears.

Receive INR settlement: INR is credited to your Indian bank account, typically within 24 hours of clearance.

Download FIRA and compliance documents: access and download your Foreign Inward Remittance Advice from the platform

Record in your accounting/tax files: log the USD amount, INR received, exchange rate, fee, net INR, invoice reference, and FIRA number.

Frequently Asked Questions

What is the cheapest way to receive USD in India?

On a pure cost basis, platforms that charge a minimum transaction fee with zero FX markup are the cheapest. Infinity's 0.5% all-inclusive fee with zero FX markup is among the most cost-efficient options for receiving USD payments in India. d.

Is PayPal good for receiving USD in India?

PayPal is globally known, but it is not the best way to receive USD payments in India. PayPal charges around 7-9% on a single transaction, which can be costly for Indian professionals. For occasional one-off payments, PayPal is still acceptable.

Is Payoneer safe for Indian freelancers?

Yes, Payoneer is safe to use for Indian freelancers. It is recommended to use Payoneer if you receive international payments from platforms like Upwork, Fiverr, and Amazon. Although for direct B2B client invoicing, Payoneer can be a costlier choice.

Can I receive USD through Wise in India?

Yes, you can receive USD payments through Wise in India. Wise is widely known for its transparent pricing and 0% FX markup.

What is the best way for agencies to receive USD from US clients?

For Indian agencies billing US clients, the best method combines a professional invoice experience for the client, low transaction costs, fast INR settlement, and solid FIRA/compliance documentation. Infinity is designed exactly for this use case. SWIFT can work for large one-time projects, but it involves more friction and a higher total cost.