Discover infinity

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

The real question about Wise is not whether it is cheap. It is whether it works end-to-end for Indian users, fees, settlement, documentation, compliance, and support.

Over 12 months, I used Wise to accept international payments from clients across the US, UK, and Europe. I ran USD, GBP, and EUR payments through it. I dealt with account verification, payment documentation, FIRA requests, and at least one support delay that cost me time I did not have.

This review covers 12 months of my experience using WISE: what worked, what did not, what WISE never tells you in the marketing copy, and who should actually use it in India today.

The conclusion is not “Wise is good” or “Wise is bad.” It depends entirely on your use case, such as your invoice size, and how much ease you need with the documentation process.

Review note: Verify current details on Wise’s official India page and Help Centre before initiating a transfer.

Quick Summary: Is Wise Good for Accepting International Payments in India?

Wise works well for Indian freelancers, consultants, and remote workers who need a transparent and predictable way to receive international payments in India. Wise supports multiple currencies and countries to receive international payments from.

It falls short for exporters, larger businesses, and users who need seamless FIRA/eFIRA workflows and the ability to hold foreign currency in Wise accounts.

Wise India: At a Glance

Category | Rating | What It Means |

Fee transparency | ⭐⭐⭐⭐⭐ | Best-in-class. All costs visible before you confirm. |

Exchange rate | ⭐⭐⭐⭐ | Mid-market rate with no hidden FX markup. Although a transaction fee of ~1.65–1.8% is there. |

Transfer speed | ⭐⭐⭐⭐ | 1–3 business days to the Indian bank after conversion |

FIRA/documentation | ⭐⭐⭐ | The e-FIRC is issued automatically. |

India-specific features | ⭐⭐⭐ | No INR balance hold, no domestic card use, limited outward remittance onboarding |

Best Alternative | 0.5% fee per transaction | |

Support | ⭐⭐⭐ | Adequate for routine issues; slow for urgent or complex cases |

Value for money | ⭐⭐⭐⭐ | Strong for small-to-mid invoices; expensive at scale vs flat-fee alternatives |

My 12-Month Wise Setup: How I Used It & What I Used Wise for

Duration: 12 consecutive months of inward payment receipt

Currencies received: USD (primary), GBP, EUR

Typical invoice range: $1500 to $5,000 per payment

Client locations: US, UK, Germany, Australia

Account type: Wise Business account

INR withdrawal bank: Private sector bank (Kotak Mahindra Bank)

Payment frequency: 3-4 payments per month across different clients

Purpose: Export of professional/consulting services

What I Did Not Use Wise for

I did not use Wise as a full accounting system. I did not use it for every client; for some clients, I used SWIFT transfer, and for some, I used different platforms.

I did not test the Wise card for India (unavailable for domestic use). I did not attempt outward remittance from India via Wise (currently paused for new users as of 2026). This review focuses specifically on receiving international payments and settling in INR.

What Is Wise, and How Does It Work in India?

Wise (formerly TransferWise) is a global money movement platform that lets users send, receive, convert, and spend money internationally. It has built its reputation on two things: showing the mid-market exchange rate (the same one you see on Google) and making all the fees upfront before initiating a transfer.

In India, Wise operates through partner bank arrangements under RBI authorisation. Wise can facilitate inward international payments for Indian users, but the features available to Indian accounts are limited compared to the features provided to UK and US clients.

Wise Personal Account vs Wise Business Account in India

The personal account suits freelancers, remote workers, and consultants receiving payments for individual services.

“Business” does not necessarily mean the user must have a private limited company.

But in my opinion, the business account is the right choice for you if you operate as a registered company and need FIRA documentation for each transaction.

For most exporters and agencies, the business account is the one to use.

Receiving Money vs Sending Money from India

These are completely separate functions. Receiving international payments into India via Wise works well for supported currencies and use cases. Sending money outward from India via Wise is a different story; Wise paused onboarding for new outward remittance users as it navigates its revised RBI licence structure.

If outward remittance is your primary need, Wise is not the right tool right now.

Does Wise Work in India for Accepting International Payments?

Yes, Wise works in India for supported currencies. It offers clean account verification. The friction shows up when you hit compliance checks, documentation requests, FIRA needs, or purpose-code questions.

What Worked Well in My Usage

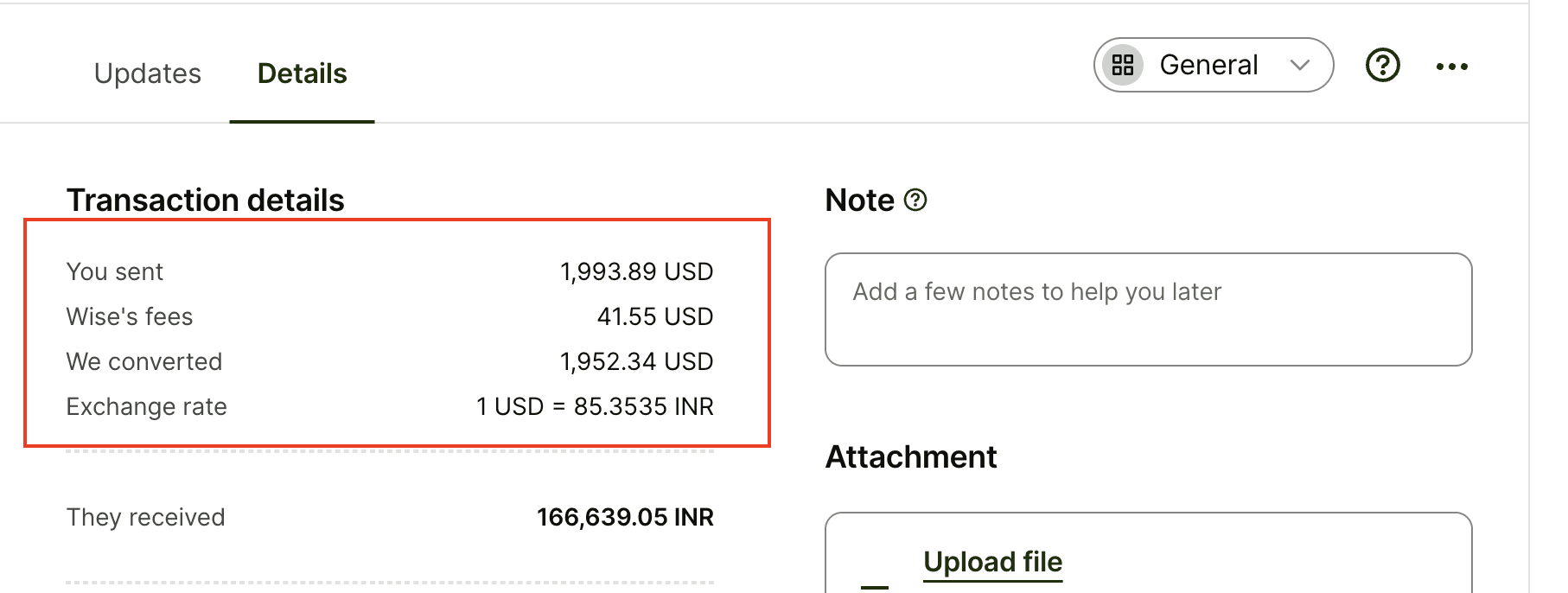

Receiving USD, GBP, and EUR client payments was generally smooth. Wise provides local bank details in USD (US routing + account number), as you can see in the image, GBP (UK sort code), and EUR (IBAN), so your client pays as if they are paying a local account. No SWIFT. No correspondent bank fees are eating into the transfer on the sender's side.

Fee visibility before conversion was genuinely good. Before every conversion, I could see the exact conversion fee, the exchange rate Wise used, and the estimated INR I would receive. No surprises at the end.

Payment tracking was clear. The Wise dashboard showed payment status in real time. This was clearly better than the SWIFT payment, which involved chasing the bank at every step.

Repeat client payments got easier over time. Saved account details, familiar onboarding, and no re-verification for known senders made recurring invoice cycles straightforward.

Where Wise Felt Limited in India

No INR balance holding. Indian Wise accounts auto-convert foreign currency to INR upon receipt. If you want to hold USD and convert when the rate moves in your favour, Wise does not let you do that. The conversion happens on Wise’s timeline, not yours.

Documentation requests came without much warning. Though it never happened to me, a close friend of mine has experienced this lately. The process was not unclear, but the timing was unpredictable, and the support response was slower than the urgency warranted.

Purpose-code alignment required attention. Indian cross-border service payments need the right RBI purpose code. Wise does not make purpose-code selection as prominent as India-focused platforms do, and a mismatch can create delays.

Wise Fees India 2026: What I Actually Paid Over 12 Months

Wise’s cost for Indian users receiving international payments has three layers:

Conversion fee: Approximately 1.65–1.8% of the transferred amount (varies slightly by currency pair and transfer volume)

GST: 18% applied on the conversion fee only, not on the full transfer amount

There is no hidden FX markup on top of this. Wise uses the mid-market exchange rate. The conversion fee is where the cost lives, and it scales with invoice size.

What I Actually Paid: Fee Examples by Invoice Size

These calculations use an illustrative USD/INR rate of ₹84.00 and a 1.7% conversion fee (midpoint of Wise’s stated range for USD). Actual rates vary; verify using the Wise fee calculator before every transfer.

Invoice Amount | Conversion Fee (~1.7%) | GST on Fee (18%) | Total Cost (USD) | INR Received (approx.) | Effective Cost |

$500 | $8.50 | $1.53 | $12.03 | ₹40,989 | ~2.4% |

$1,000 | $17.00 | $3.06 | $22.06 | ₹82,147 | ~2.2% |

$2,500 | $42.50 | $7.65 | $52.15 | ₹2,05,619 | ~2.1% |

$5,000 | $85.00 | $15.30 | $102.30 | ₹4,11,407 | ~2.0% |

$10,000 | $170.00 | $30.60 | $202.60 | ₹8,22,982 | ~2.0% |

Example only. Verify in the Wise calculator at wise.com before transferring.

Was Wise Cheaper Than My Bank?

For most payments in the $500–$5,000 range, Wise was cheaper than a typical Kotak or HDFC SWIFT inward remittance. Here is why:

Cost Component | Traditional Bank SWIFT | Wise |

FX markup | 1–3% hidden in rate | 0%, mid-market rate used |

Transfer fee | ₹500–₹1,500 flat | Included in the conversion fee |

Correspondent bank deduction | $10–$25 (unpredictable) | None (client pays locally) |

FIRA | Usually free | Free |

Total effective cost | 2–4%+ depending on the bank | ~2.0 all-in |

The bank’s advertised rate often looks competitive until you factor in the FX markup embedded in the rate they offer versus the mid-market rate. Wise separates this clearly. That transparency, more than the raw fee, is where Wise earns its reputation.

The Fee Lesson After 12 Months

Wise was often cheaper than my bank for small-to-mid invoices when I compared the final INR received, not the headline fee. But cheapest-per-transfer is not the same as most cost-effective at scale.

At $5,000 per month for 12 months, the ~2% Wise fee amounts to roughly ₹1,00,000 in conversion costs. Flat-fee platforms at that volume cost significantly less. The decision to use Wise should include a projection of your annual transfer volume, not just a single-invoice comparison.

Wise Exchange Rate Review: Did I Really Get the Mid-Market Rate?

Before every conversion, Wise shows you the exchange rate it uses. It labels it as the mid-market rate. You can cross-check it against Google’s currency converter or XE.com.

In my 12 months of use, the rate Wise displayed matched the mid-market rate within a small rounding margin every time. Wise does not embed a spread into the rate itself. The cost is in the conversion fee, separately and clearly shown.

Why Final INR Received Matters More Than the Displayed Rate

Many traditional platforms show a competitive-looking fee but earn through the exchange rate spread. Compare this properly:

The right comparison: Invoice amount → minus all fees (conversion fee + GST + FIRA + any bank charges) → final INR credited to your account.

A platform with a 0% “fee” but a 2.5% embedded FX spread costs more than Wise. A platform with a flat ₹1,500 fee and no FX markup costs less than Wise on larger invoices. The displayed rate and the headline fee are both incomplete; only the final INR number tells you the true cost.

My Exchange Rate Summary

Wise’s exchange rate practice is genuinely transparent and better than most Indian banks'. For users who care about knowing exactly what they pay before they confirm, Wise is hard to beat on clarity. The rate of quality is strong. The question is whether the conversion fee on top of it works out cheaper than alternatives at your specific invoice volume.

Wise Transfer Speed: How Long Did Payments Take?

Payment Route | Typical Settlement | Fastest | Slowest | Main Delay Cause |

USD to INR | 2–3 business days | 1 business day | 5 business days | Compliance review |

GBP to INR | 2–3 business days | 1 business day | 4 business days | Bank processing |

EUR to INR | 2–4 business days | 2 business days | 6 business days | Purpose code check |

These reflect my personal experience across 12 months. Individual transfer times vary based on account status, payment amount, and compliance triggers.

What Made Transfers Faster

Verified Wise business account with all KYC documents submitted upfront

Repeat clients with known payment details

Correct the purpose code on the payment (P0802 for software/IT services is common for freelancers)

Matching sender and recipient names across documents

Client paying via bank transfer, not card (card-funded payments take longer to process)

Payments initiated early in the week, weekend payments processed Monday

What Caused Delays

Compliance holds (unpredictable, happened once in 12 months with my friend)

Bank holidays in the sending country

EUR payments occasionally triggered additional scrutiny

Incorrect purpose code on one early payment (took 5 business days to resolve)

Large payment amounts (above $3,000) sometimes prompted manual review

For freelancers billing monthly, a 2–3 business-day window is workable. For exporters with tight payment cycles or businesses that need same-day or next-day INR credit, Wise’s timeline may not fit. Some India-focused platforms settle in 1 business day as standard.

Wise FIRA/eFIRA India:

For Indian freelancers and exporters, documentation is not a paperwork formality. FIRA (Foreign Inward Remittance Advice) or eFIRC (electronic Foreign Inward Remittance Certificate) connects to GST compliance, ITR filing, LUT submissions, and, in some cases, eBRC generation for goods exporters.

Why FIRA/eFIRA Matters

Every foreign payment that enters India as an export service receipt needs to be documentable. Your accountant, your CA, and your bank may ask for it. Without clear documentation:

You cannot claim GST zero-rating benefits on export services (LUT route)

You face complications during ITR filing when reconciling foreign income

Your bank may not recognise the inward remittance as export income for FEMA purposes

Some clients in regulated industries ask for payment trail documentation

Choosing a payment platform partly on the strength of its documentation workflow is sensible, not paranoid.

My Experience with Payment Documentation on Wise

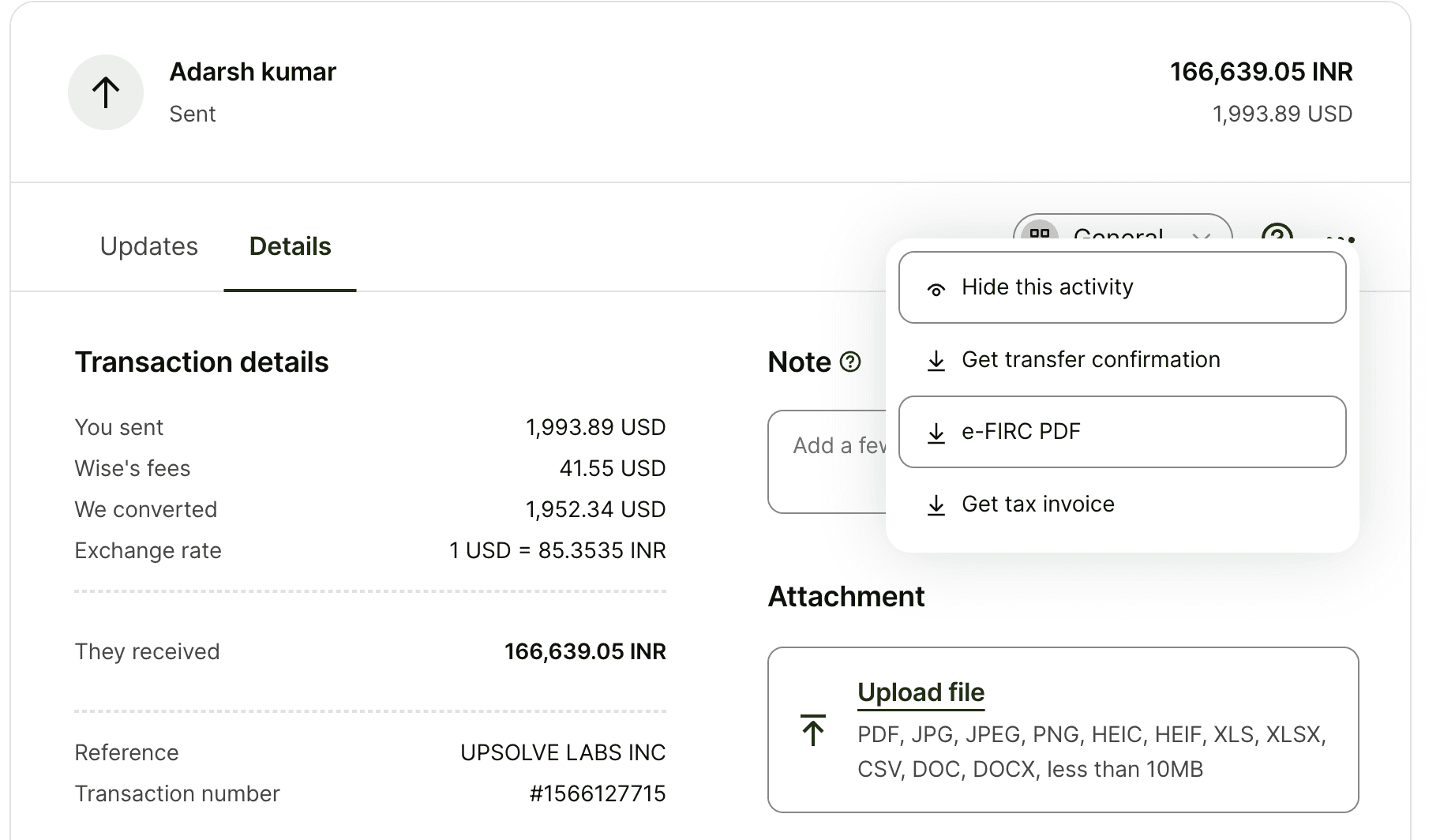

Wise charges approximately USD 2 as part of the INR payout and automatically issues an e-FIRC for the transfer. The document is normally emailed within three working days and can also be downloaded from the Wise account.

Is Wise Safe in India?

Yes. Wise operates in India under RBI authorisation through partner bank arrangements. It uses 2-factor authentication, 256-bit encryption, and continuous fraud monitoring. Wise is regulated in multiple jurisdictions globally (FCA in the UK, FinCEN in the US) and maintains those standards across its Indian operations.

In 12 months, I had no security incidents, no unauthorised access, and no unexplained fund movement. The compliance holds I experienced were standard verification requests, not security issues.

Practical safety checklist for Indian Wise users:

Enable 2FA on your Wise account

Verify your account fully before your first payment (KYC, business documents if applicable)

Use Wise’s official app or website.

Check that client payment references match your invoice details

Keep records of all transaction IDs and FIRA certificates

Wise Limits in India: What Users Should Check Before Using It

#1. Transfer Limits

Wise does not publish a single flat limit for all Indian users. Limits vary by currency, account type, verification level, and regulatory requirements. For outward remittance (sending from India), the RBI’s Liberalised Remittance Scheme (LRS) caps personal transfers at $250,000 per financial year.

For inward receipts, no RBI cap exists on the amount you can receive, but Wise applies its own account-level verification checks for large payments.

Before a large payment (above $5,000), verify your current account limits in the Wise Help Centre and confirm your account verification status is complete.

#2. Purpose-Code Restrictions

Every Indian inward remittance needs a purpose code that tells the RBI why the money is coming in. Common codes for service exporters:

P0802 – Software and IT services

P0899 – Other professional services

P1004 – Business services

P0101 – Education (if applicable)

Wise does not surface purpose-code guidance prominently in its India-facing UX. If you use the wrong code, expect delays. Your CA or accountant can confirm the right code for your specific service category.

#3. Business and Account Verification Limits

For a Wise Business account in India, you need to provide:

PAN card

Certificate of Incorporation (for companies) or registration documents

Business address proof

Director/owner identity and address proof

Business description and expected transaction volume

Sample invoices or client contracts

KYC is thorough. Wise does not rush this, and nor should you. Incomplete verification could lead to payment delays.

#4. Bank-Side Limits

I used Kotak Mahindra Bank for my payments. Other users may have different experiences with HDFC, ICICI, or SBI. Some cooperative or small-finance banks have asked for additional documentation for international credits.

If you bank with a less commonly used institution, confirm that it accepts inward remittances from payment aggregator platforms before you set up Wise as your collection method.

What I Liked About Wise After 12 Months

#1. Transparent Fees

Wise showed me: conversion fee amount in dollars, GST on the fee, FIRA cost, exchange rate, and expected INR credit, before any conversion. I never had to calculate what I paid. This was genuinely refreshing for someone who has chased banks for years to know the final amount.

#2. Clean Payment Tracking

The Wise dashboard showed payment status in real time. When a client said, “I sent the payment,” I could see within hours whether it had hit the Wise account or not. No waiting 2 days to see if a SWIFT had cleared, or calling the bank. At each and every step, I was notified.

#3. Better FX Clarity Than Most Banks

Wise uses the mid-market rate and shows the conversion fee separately. HDFC’s telegraphic transfer rate, by contrast, includes an FX spread that is not disclosed as a standalone cost.

On a $3,000 invoice, the difference between Wise’s all-in cost and a bank’s all-in cost (including their embedded spread) was consistently ₹1,500–₹3,000 in my favour on Wise. That is not a small number across 12 months.

#4. Easy Enough for Overseas Clients

My US and UK clients found Wise simple. They received local bank details (US ACH routing + account, or UK sort code) and paid as a domestic transfer. No SWIFT codes to fill in. No correspondent bank uncertainty. So, this made the whole payment process seamless and hassle-free.

#5. Good for Repeat Payment Workflows

After the first two payments from a client, the process was almost invisible. No new verification steps, no re-uploading documents, no changes to payment details.

What I Did Not Like About Wise After 12 Months

#1. India-Specific Availability Can Be Confusing

Wise’s India feature set is not the same as its UK or US feature set. Outward remittance onboarding is paused. The domestic debit card is unavailable. You cannot hold INR or foreign currency balances and choose when to convert.

#2. Documentation Can Become the Real Bottleneck

Wise is not designed around Indian documentation workflows. FIRA is manual and paid. Purpose codes are your responsibility to manage. The invoicing tool inside Wise is generic; it is not GST-compliant and cannot serve as your tax invoice. If your accountant asks you for transaction-wise FIRA every quarter, you are generating that manually from the Wise dashboard, one certificate at a time.

#3. Support Is Not Always Fast Enough for Urgent Payments

The Wise support experience over chat and email was responsive to simple queries. For held-payment situations, where a client is waiting, a deadline exists, and the payment is stuck in compliance review, the response time was adequate in one case and frustratingly slow in the other. I waited 36 hours for a resolution that could have been 4 hours. For a platform used for business-critical payments, that is a real risk.

#4. Larger Payments Need More Caution

Three of my payments above $3,000 triggered a manual review. This is not unusual; all international payment platforms apply compliance checks at higher amounts. But Wise’s review process is not clearly defined in advance. You do not know ahead of time which payment will get flagged, what documents you will need, or how long the review will take. Building buffer time into large payment cycles is essential.

#5. Not the Best Fit for Every Indian Business

Wise is a global-first product. Indian exporter workflows, FIRA per transaction, GST-compliant invoicing, purpose-code management, eBRC generation, FEMA compliance documentation were not the design centre of Wise’s product. For freelancers with simple payment needs, this gap is manageable. For exporters, agencies with high monthly volumes, or businesses that need full compliance automation, the gap becomes a recurring overhead.

Wise vs Infinity vs Banks: Which Was Better?

Feature | Wise | Infinity | Traditional Bank (SWIFT) |

Fee structure | ~2% all-in (conversion fee + GST + FIRA) | 0.5% Fee, 0 FX Markup | 2–4% (hidden FX spread + transfer charges + correspondent bank deductions) |

Exchange rate | Mid-market, no markup | Mid-market, no markup | Bank TT rate (includes embedded spread) |

FIRA | Free, automated | Free, automated | Usually free via bank |

India-specific compliance | Partial — purpose codes are user-managed | Built-in India-first workflow | Varies by bank |

Settlement speed | 2–3 business days | Within 24 hours | 3–5 business days |

GST-compliant invoicing | No | Yes | Not applicable |

Domestic card use | No | Not applicable | Not applicable |

Outward remittance | Paused for new users | In process | Yes |

Best for | Simple inward payments, transparent FX | Indian exporters and freelancers need a compliance-ready workflow | Large institutional transfers where a bank relationship is established |

Wise is strong as a global money movement product. If your priority is transparent fees and a clean client payment experience, it delivers. If your priority is India-specific compliance support, free FIRA, GST-aligned invoicing, and faster INR settlement, India-first platforms like Infinity are built for what you need.

Wise Alternatives in India

Platform | Best For | FIRA | Fee Model | Settlement Speed |

Infinity | Indian exporters, freelancers needing compliance-ready inward payments | Free, automated | 0.5%, 0 FX Markup Fee | Fast |

Payoneer | Freelancers on global platforms (Upwork, Fiverr, etc.) | Via partner bank | ~2% on withdrawals to INR | 2–3 business days |

PayPal | Clients who insist on PayPal, small freelance payments | Limited | High (3–5% all-in) | 3–5 business days |

SWIFT bank transfer | Large institutional or one-off payments | Yes (free) | 2–4% effective | 3–5 business days |

Who Should Use Wise in India?

Use Wise If…

You value knowing the exact fee and rate before you confirm every transfer

Your invoices fall in the $500–$5,000 range, where the ~2% all-in cost is competitive

Your clients prefer paying via local bank transfer (ACH in US, Faster Payments in UK) rather than SWIFT

You are a freelancer, consultant, or solo agency with straightforward, recurring payment needs

You can manage your own purpose codes and FIRA requests

You do not need domestic card use or a foreign currency balance holding

You have confirmed that your specific payment type and currency pair are currently supported on Wise India

Avoid Wise (or Compare First) If…

Your invoice values are consistently above $5,000; flat-fee platforms cost less at that volume

You need GST-compliant invoicing built into your payment workflow

You are an exporter who needs eBRC-compatible documentation or tight FEMA compliance support

You need to send money outward from India (paused for new Wise users as of 2026)

Same-day or next-day INR settlement is a requirement for your cash flow

My Final Verdict After 12 Months

Wise earned its place in my payment workflow for specific use cases and lost out in others. Here is the honest summary:

Wise won on: Fee transparency, exchange rate clarity, clean payment experience, and a reliable tracking system for routine payments.

Wise lost on: India-specific compliance support and cost efficiency at higher volumes. When I compared the final INR received on a $5,000 invoice against a flat-fee India-first platform like Infinity, Wise cost roughly ₹5,000–₹6,000 more per payment. This adds up to a larger amount annually.

If you are an Indian freelancer or consultant receiving moderate international payments and your priority is transparent, low-effort FX conversion with a clean client experience, Wise is worth using.

If you are an exporter, agency, or business receiving larger payments regularly, build a comparison with India-first platforms like Infinity that includes FIRA cost, settlement speed, compliance workflow, and annual fee projection.

Wise is a strong global product. For India-specific payment workflows, it is not the only answer, and for many users, it is not the best one.

![9 Best Cross Border Payment Platforms in India [Based on Real User Reviews]](https://framerusercontent.com/images/ZOzvHCU1ezQxfPmG2hFSGdvRrWE.png?width=1536&height=1024)