Global payments

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

Receiving international payments in India involves more than just getting money from a client abroad. Every transaction usually goes through a number of systems, such as banks, payment networks, and layers for currency conversion, all of which have an immediate effect on the amount you will receive.

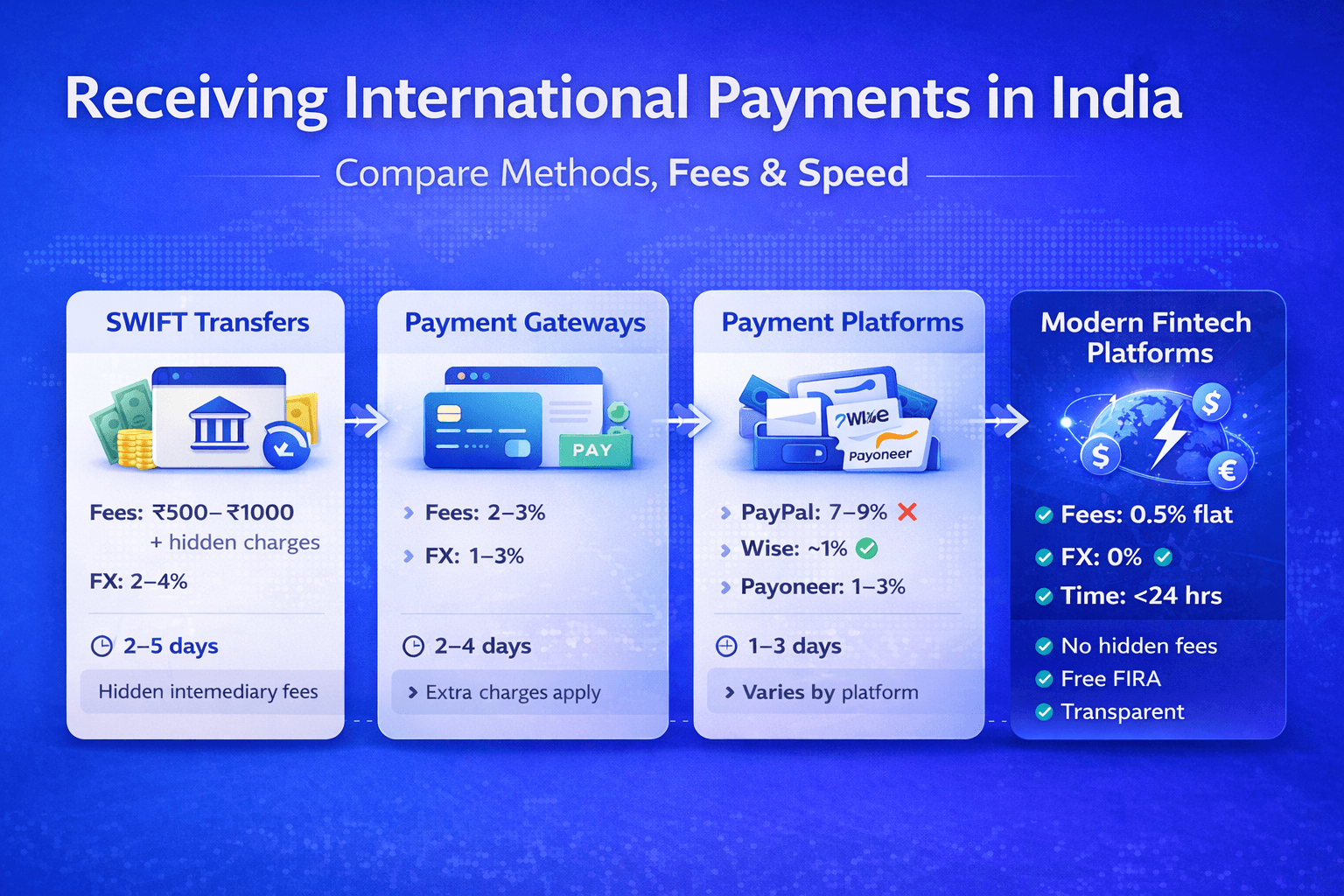

The four primary methods for receiving international payments in India usually include traditional bank transfers (SWIFT), international payment gateways, global payment platforms like PayPal, Wise, and Payoneer, and modern fintech options like Infinity, which are specifically made for cross-border transactions.

Depending on the method, there are differences in the structure of transaction fees, forex (FX) markup, intermediary bank charges, and settlement days. Even though some solutions are more convenient, they could have higher hidden costs. Others might offer better exchange rates but have more complex processes.

The least expensive choice: platforms with zero FX markup and minimal flat fees- Infinity

Global payment platform with minimum fees and mid-market exchange rate- Wise

Payment gateway with a good brand name, but expensive transaction fees and FX conversion fees- PayPal

Important takeaway: Using the appropriate strategy that suits your business needs and helps you save more money over time while receiving international payments.

Even a slight variation in fees and conversion rates can result in monthly savings of thousands of rupees for freelancers, agencies, and exporters that regularly receive international payments.

How to Receive International Payments in India?

There are several ways to receive international payments in India. Although the cost, speed, transparency, and convenience of each option vary. The most popular methods consist of bank transfers (SWIFT), international payment gateway, global payment platforms and modern fintech platforms built in India. Let's have a look at each of these methods:

Bank transfers via SWIFT, where funds move directly between banks across countries.

International payment gateways allow businesses to accept payments via cards or online checkout systems.

Global payment platforms such as PayPal, Wise, and Payoneer simplify cross-border transactions but have higher fees.

Modern fintech platforms, like Infinity, are designed to reduce costs and improve the efficiency of receiving international payments.

International payments are made possible by all of these methods mentioned above, but their efficiency varies. The actual difference is in the amount of money you get after deductions and the speed at which the payment is cleared.

Introduction to International Payments in India

India's participation in the global digital economy has grown significantly during the last ten years. Customers in the US, Europe, the Middle East, and other locations are increasingly interacting with exporters, SaaS companies, agencies, and freelancers.

India contributes billions of dollars in service exports annually, making it one of the world's leading freelance markets, according to industry reports. For many professions, cross-border payments are now a daily need due to this increase.

The procedure for accepting international payments is still complicated; nonetheless, despite this expansion. Common problems that most users experience include:

Unexpected deductions in payments

Delays in settlement

Lack of clarity on exchange rates

Compliance requirements like FIRA

These difficulties result from the fact that receiving payments internationally is a multi-step procedure. Rather, they use several middlemen, each of whom adds time and expense.

Knowing how these systems operate and selecting the best approach can have a big impact on your income.

What Are International Payments?

Transactions involving the transfer of funds between individuals or businesses situated in different nations are referred to as international payments.

Unlike domestic payments, which are managed by a single banking system, international payments involve international financial networks, conversion of currency and adherence to regulations.

Because these transactions involve multiple financial systems, they are inherently more complex and often result in additional costs.

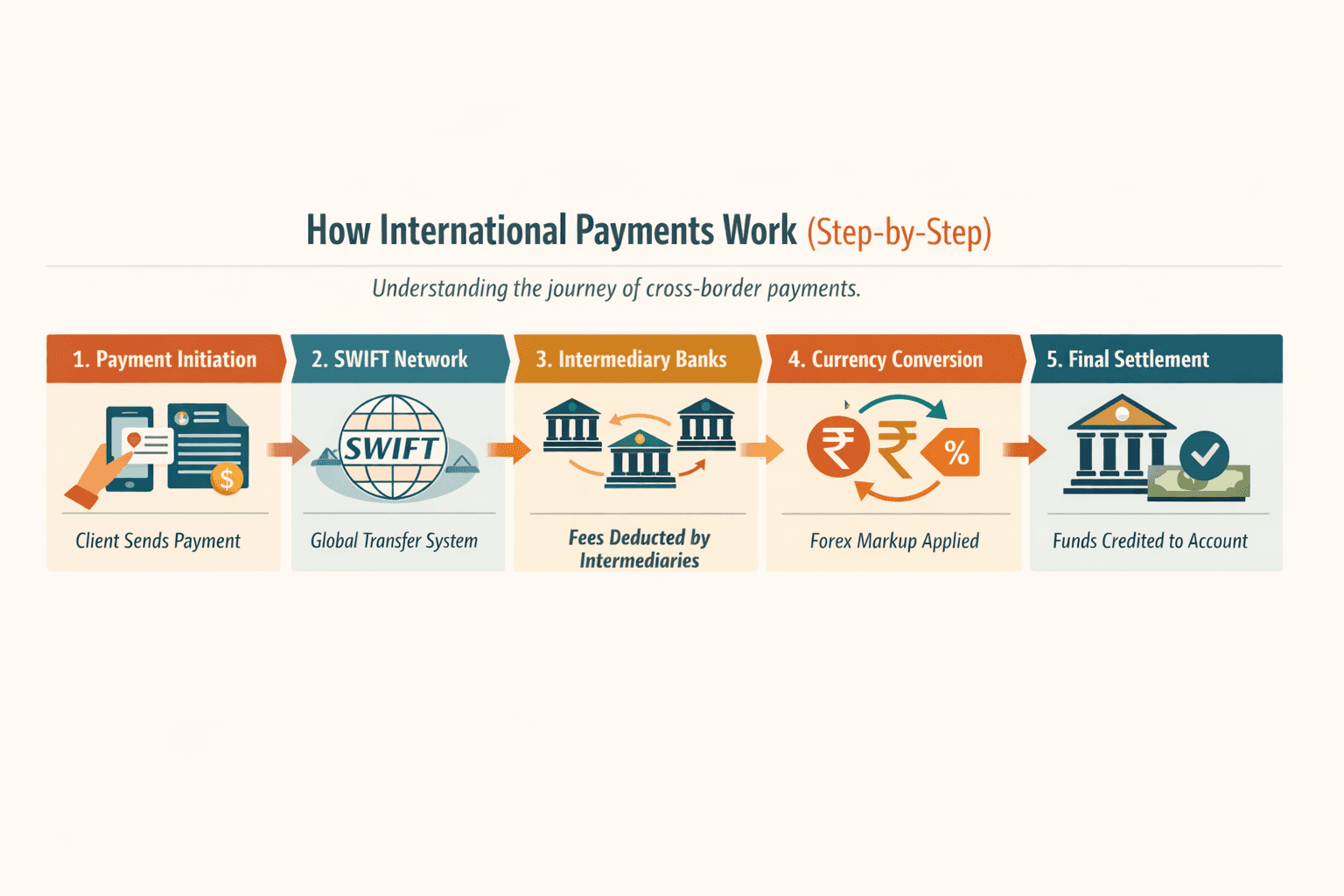

How International Payments Work (Step-by-Step)

It's crucial to examine the actual flow of international payments in order to understand where expenses occur.

1. Payment Initiation

When your client uses a payment platform or their bank to initiate a payment, that is when the procedure starts. They offer information about your platform account, bank account, and SWIFT code.

2. Routing Through the SWIFT Network

After that, the payment is sent via the SWIFT network, which serves as a global messaging system that links banks.

3. Intermediary Banks

The payment goes through one or more intermediary banks if there is no direct connection between your bank and the sender's bank.

Each intermediary may deduct a processing fee, which is often not visible upfront.

4. Conversion of Currency

Before the money gets to your account, it is converted into Indian rupees. Banks and platforms usually apply a markup that is higher than the real exchange rate.

This FX markup is typically the highest hidden cost, which typically falls between 2 and 4%.

5. Final Settlement

The remaining amount is credited to your bank account following any deductions. Depending on the method chosen, this process may take one to five business days.

Why this matters

Every step in this procedure adds money and time, even though it takes place in the background. You can find areas for optimisation and cost savings by understanding this cycle.

Methods to Receive International Payments in India

One of the most crucial choices for Indian businesses, agencies, and freelancers is how to accept international payments in India. Although receiving money from overseas is technically possible with any of these ways, they vary greatly in terms of cost, timeliness, transparency, and use case.

You can select a strategy that suits your goals and save unnecessary losses by being fully aware of these variations.

1. Bank Transfers (SWIFT)

The most traditional and popular way to receive international payments in India is through bank transfers via the SWIFT network. Using information like your account number, bank branch, and SWIFT/BIC code, the sender uses this technology to transfer money straight from their bank account to your Indian bank account.

Although this approach is regarded as trustworthy, it is also among the most complex in terms of the actual flow of money.

It's very rare for a payment to go directly from the sender’s bank account to the receiver’s bank account. Rather, the payment typically goes via one or more banks that act as intermediaries. These banks serve as intermediaries between organisations that are not directly connected to one another. A processing fee may be charged by each intermediary at each step.

Currency conversion is another crucial element. The live exchange rate is not charged by most banks. Rather, they immediately lower the amount you receive by applying a forex markup, usually between 2% and 4%.

Fees & Charges involved:

Bank receiving fee (₹500–₹1,000 approx.)

Intermediary bank charges (variable, often hidden)

Forex markup (2–4%)

Settlement Time:

Usually 2 to 5 business days, sometimes longer, depending on routing

Pros:

Because of their high reliability, bank transfers are frequently chosen for big transactions where documentation and confidence are essential. Additionally, they are widely used in many countries and industries.

Cons:

The absence of transparency is the main disadvantage. Until you receive your payment, you usually have no idea how much will be deducted. Additionally, the combination of multiple fees and forex markup can significantly reduce your final payout. The settlement time is also slower compared to newer alternatives.

2. International Payment Gateways

Businesses that accept payment online via their website, payment links, or checkout systems often use international payment gateways. From the sender's point of view, these platforms make it easier for customers to pay with credit cards, debit cards, or digital wallets.

Payment gateways serve as a layer of middleman between the client and the bank for Indian users. They receive the payment, process it, convert the currency, and then deposit the money into your account.

Payment Gateways are helpful for companies with international clients and are simple to incorporate, but they are not always the most economical choice.

Fees & Charges involved:

Transaction fees (typically 2% to 3%)

Forex markup (1% to 3%)

Additional charges depending on the payment method

Settlement Time:

• Usually 2 to 4 business days

Pros:

Payment gateways are quite practical for companies that want their clients to have a smooth payment experience. They are appropriate for SaaS and e-commerce businesses since they accept a variety of currencies and payment options.

Cons:

Because of the mix of transaction fees and currency markup, the total cost may be somewhat higher. Furthermore, these systems are not designed for freelancers or service-oriented companies receiving direct transfers.

3. Payment Platforms (PayPal, Wise, Payoneer)

Global payment platforms are the most popular choice among freelancers and small firms, because they simplify the process of receiving international payments. But every platform has its own pricing structure and operates in a different way.

PayPal

One of the most popular platforms in the world, PayPal is usually the first option for new freelancers.

Clients can send money with ease, and the money is received in your PayPal account right away.

But there is a price for this convenience.

Fees & Charges:

Transaction fee: 4% to 5%

Forex markup: 3% to 4%

This implies that the overall cost per transaction may reach 7%–9%, which is among the highest of all the options.

Settlement:

Instant to PayPal wallet

2-5 days to transfer to the bank

Pros:

PayPal is widely recognised, simple to use, and requires little setup. When working with clients who are not familiar with other platforms, it is particularly helpful.

Cons:

Cost is the main disadvantage. The high costs and poor exchange rates have the potential to drastically lower your earnings over time.

Wise

Wise (previously TransferWise) is renowned for using real exchange rates and clear pricing.

In contrast to many platforms, Wise makes it easy for its users to understand the fee structure by openly disclosing the fee before the transaction is finalised.

Fees & Charges:

Transfer fee: ~0.5% to 1%

Uses real exchange rate (minimal markup)

Settlement:

Typically 1–2 business days

Pros:

Compared to traditional platforms, Wise provides greater transparency and more affordable exchange rates. It is a good choice for those who value pricing clarity.

Cons:

Even though Wise is inexpensive, Indian consumers might not always have a completely smooth compliance experience with it, particularly when it comes to paperwork like FIRA.

Payoneer

Freelancers who operate on international marketplaces like Upwork, Fiverr, and Amazon often use Payoneer.

It enables users to accept payments like a local business in other countries by giving them virtual receiving accounts in several currencies.

Fees & Charges:

Receiving fee: ~1% to 3%

Forex markup: ~2%

Withdrawal charges may apply.

Settlement:

Usually 1–3 business days

Pros:

Payoneer is very adaptable, integrates easily with marketplaces and supports a variety of currencies, which makes it helpful for freelancers with clients in other countries.

Cons:

Because there are several tiers of payments, the cost structure may be complicated. The total cost of each transaction may not always be fully visible to users.

4. Modern Fintech Platforms (Infinity)

To address the shortcomings of traditional cross-border payment systems, modern fintech platforms like Infinity have been designed. Platforms like Infinity are designed especially for exporters, agencies, and freelancers who regularly receive payments internationally.

Infinity, in contrast to conventional methods, eliminates unnecessary intermediaries, increases fee transparency, and provides quicker payments. Infinity is one such platform designed especially for Indian users handling international payments.

The main issues with cross-border payments that are addressed by Infinity:

Hidden fees

Forex markup

Slow settlement

Compliance complexity

Fees & Charges (Infinity):

0.5% flat fee (all inclusive)

0% FX markup

No intermediary deductions

Settlement:

Within 24 hours

Additional Features:

Instant & free FIRA

Transparent pricing

Centralised dashboard

Pros:

Infinity provides complete transparency in pricing, ensuring that users know exactly how much they will receive. The absence of FX markup significantly increases the final payout. 24-hour settlement provided by Infinity also improves the cash flow for users.

Cons:

As Infinity is a newer platform compared to traditional systems, awareness is still growing among Indian users.

Charges Involved in Receiving International Payments in India

It's important to know that there are multiple fees associated with receiving international payments in India. There are several charges and fees involved in the whole transaction process when receiving the payment.

One of the highest charges and usually the hidden one is the FX markup. This is the difference between the rate provided by banks or platforms and the actual exchange rate. Particularly for larger transactions, even a little markup of 2-3% can cause a significant loss.

Platforms also impose a transaction fee, which is typically a small percentage fee charged by the platforms, in addition to FX markup. Even though this fee is evident, it frequently does not account for the majority of the entire cost.

Intermediary bank fees are another hidden expense. Each bank may charge a fee when payments are sent through them. These fees are hard to track because they are rarely stated up front. Additionally, some platforms also impose withdrawal fees when you move money from their platform to your bank account.

It is very important to understand each of these fees collectively, as many users just concentrate on one price rather than considering the whole picture.

Documents Required to Receive International Payments in India

In India, accepting international payments is not only a financial procedure but also a regulated activity. This implies that in order to guarantee adherence to Indian legislation, specific documentation is needed.

The invoice is one of the most crucial documents since it serves as evidence of the goods or services rendered. It contains information about the client, the transaction's nature, the amount, and the currency.

The Foreign Inward Remittance Advice (FIRA) is another important document. This paper serves as evidence that foreign exchange has been received in India. Accounting, taxation, and regulatory requirements frequently call for it.

A purpose code, which describes the type of transaction (such as the export of services, consultation fees, etc.), may also be required.

To guarantee seamless processing, you must also provide accurate bank information, including your SWIFT code.

It's crucial to understand and keep these papers ready not only for compliance purposes but also for avoiding delays and complications in receiving international payments.

Common Mistakes to Avoid while Receiving International Payment

Ignoring forex markup and concentrating solely on transaction fees is one of the most frequent mistakes individuals make. In actuality, forex markup often accounts for a larger portion of the whole cost than the visible fee.

Selecting a platform only on the basis of brand familiarity is another mistake. A platform is not always the most economical just because it is commonly utilised.

Additionally, a lot of consumers neglect to figure out the entire cost of receiving payments. They examine each fee separately, but they do not assess the overall cost of all the fees.

Ignoring compliance standards, such as keeping accurate records, can also lead to problems down the road, particularly when it comes to tax filing or audits.

Lastly, not considering your options before selecting a platform may eventually lead to unnecessary losses.

How Infinity Simplifies International Payments in India

Traditional cross-border payment methods are often complicated, slow, and filled with hidden expenses. By providing a clear and effective solution designed especially for Indian freelancers and companies, Infinity streamlines this entire process. Users of Infinity benefit from:

0.5% transaction fee (all inclusive)

0% FX markup

No hidden charges

24-hour settlements

Instant & free FIRA

Centralised dashboard for full visibility

Infinity guarantees you that you will not only receive your international payments within 24 hours, but also that you will keep the maximum portion of your earnings, ensuring 100% transparency.

Conclusion

Receiving international payments in India involves multiple steps, from banking systems and currency conversion to compliance requirements and platform fees. Making wise selections requires an understanding of how these elements work. Your revenue, settlement time, and overall experience can all be directly impacted by the method you select. So make your decision wisely!

FAQ on Receiving International Payments in India

How can I receive international payments in India?

Bank wire transfers (SWIFT), international payment gateways, platforms like PayPal, Wise, and Payoneer, or modern fintech solutions like Infinity are all options to accept international payments in India. Fees, speed, and convenience of use are some of the elements that determine which option is ideal.

What is the most effective method for accepting international payments in India?

The best way depends on your needs. Platforms like PayPal are popular if convenience is your top priority. Platforms with little forex markup are more effective if you want fewer expenses and better exchange rates. For frequent payments, choosing a solution like Infinity with transparent pricing can significantly improve your earnings.

What are the charges for receiving international payments?

Transaction costs, forex (FX) markup, intermediary bank fees, and occasionally withdrawal fees are examples of charges. Forex markup, which typically ranges from 2 to 4%, is frequently the biggest hidden expense among these.

What documents are required to receive international payments in India?

An invoice, purpose code, and Foreign Inward Remittance Advice (FIRA) are typically required. These records are necessary for accounting, taxation, and compliance.

Is PayPal safe for receiving international payments in India?

Yes, PayPal is safe and extensively utilised throughout the world. But compared to other options, it has comparatively higher costs and currency markup, which can lower your final reward.