Discover infinity

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

Payoneer has been a fixture in the Indian freelancer and exporter ecosystem for years. If you have ever received payments from Upwork, Fiverr, or Amazon Global Selling, there is a chance that Payoneer was your first port of call. Payoneer is globally accepted and works really well.

If you have been using Payoneer lately, you might have noticed the erosion. In a $1, 000 invoice, Payoneer takes around 1% as receiving fees, and on top of that, Payoneer applies 2-3% as conversion fees.

Payoneer also charges a $29.95 annual inactivity fee that sits in the background waiting to strike during a slow month. If you add all of it, you will find out that you are paying a 4-7% of fees on every international payment that you receive.

Beyond fees, Indian Payoneer users consistently report account freeze issues, slow customer support for non-standard queries, and limited direct B2B flexibility for businesses. Indian users also face compliance friction when they need documents like FIRC/FIRA for GST filings.

In this blog, we will cover the alternatives to Payoneer that are available in India.

This article will be very specific with honest guidelines on fees, compliance documentation, and settlement speed, and which option fits your use case.

We have evaluated each platform against those criteria that actually matter for Indian inward remittances.

Also Read - Payoneer Review (2026): Fees, User Complaints, and Alternatives

TL; DR: Best Payoneer Alternatives

Use Case | Best Platform | Why |

Best overall Payoneer alternative | Infinity | 0.5% all-in, zero FX markup, 24-hr settlement, free auto-FIRA |

Best for transparent FX rates | Wise | Mid-market rates, clear fee disclosure, multi-currency wallet |

Best for global buyer familiarity | PayPal | Recognised globally, easy client onboarding |

Best for checkout infrastructure | Stripe | Powerful APIs, subscription billing, SaaS card payments |

Best for domestic + international | Razorpay | Unified India stack plus international bank transfers |

Best for multi-currency + investing | Airwallex | Multi-currency wallet, competitive FX, hold foreign currency |

Best digital wallet for freelancers | Skrill | Quick setup, prepaid card, works for P2P and small amounts |

Best for paying contractors globally | Deel | Contractor management, multi-currency payouts, and compliance tools |

Marketplace payouts still need Payoneer | — | No alternative fully replicates 500+ platform integrations |

Why Users Look for Payoneer Alternatives

These are concrete friction points that affect real business operations and not just a general "fees are high" complaint.

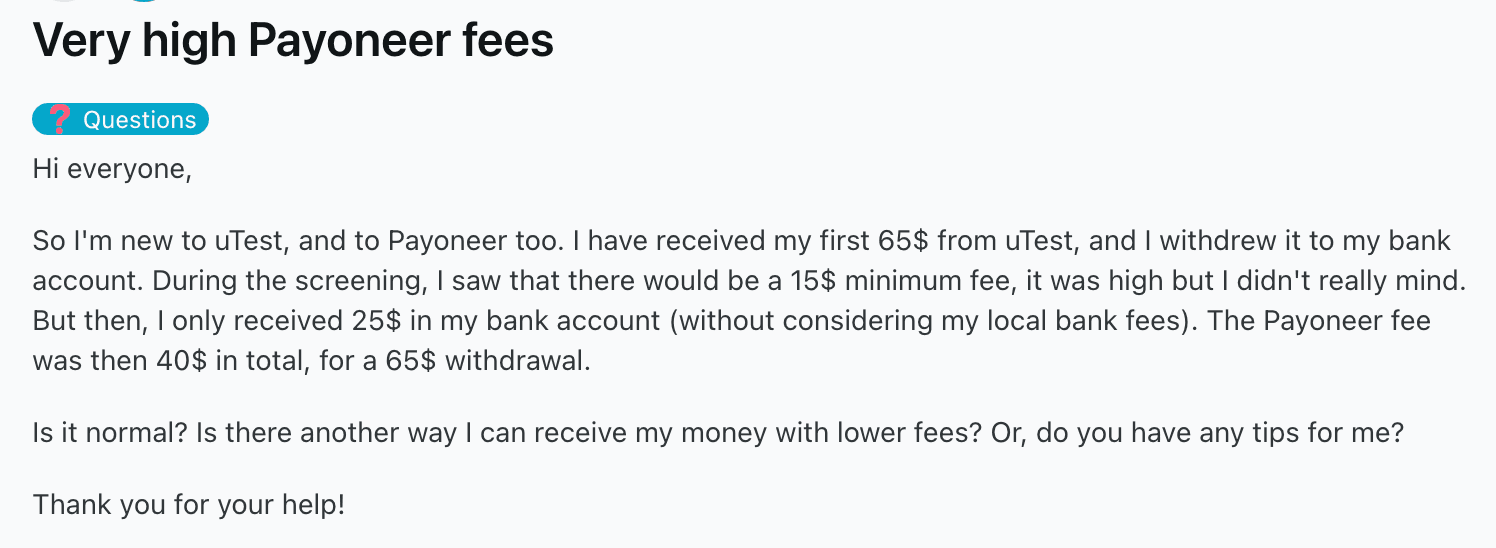

1. High fees on every transaction.

The 1% receiving fee from marketplaces is only the starting point. The higher cost is the FX markup, which is up to 3% above the mid-market rate. Indian Payoneer users routinely pay 4–7% in effective costs per transaction.

Source: Reddit

2. FX markup that is not disclosed upfront as a fee.

As the FX margin is buried in the conversion rate, many users don’t realise that they are paying an extra 2-3% on INR withdrawals.

3. Account holds and freezes.

Payoneer's automated compliance systems flag accounts for unusual activity. This can highly affect the real business operation for Indian users. Funds are held for days or weeks while verification processes play out, disrupting cash flow.

4. Slow INR settlement: 2 to 5 business days.

For a business managing monthly expenses on a tight timeline, waiting 2–5 days for funds is a meaningful constraint. Platforms like Infinity settle funds in 24 hours as a standard timeline.

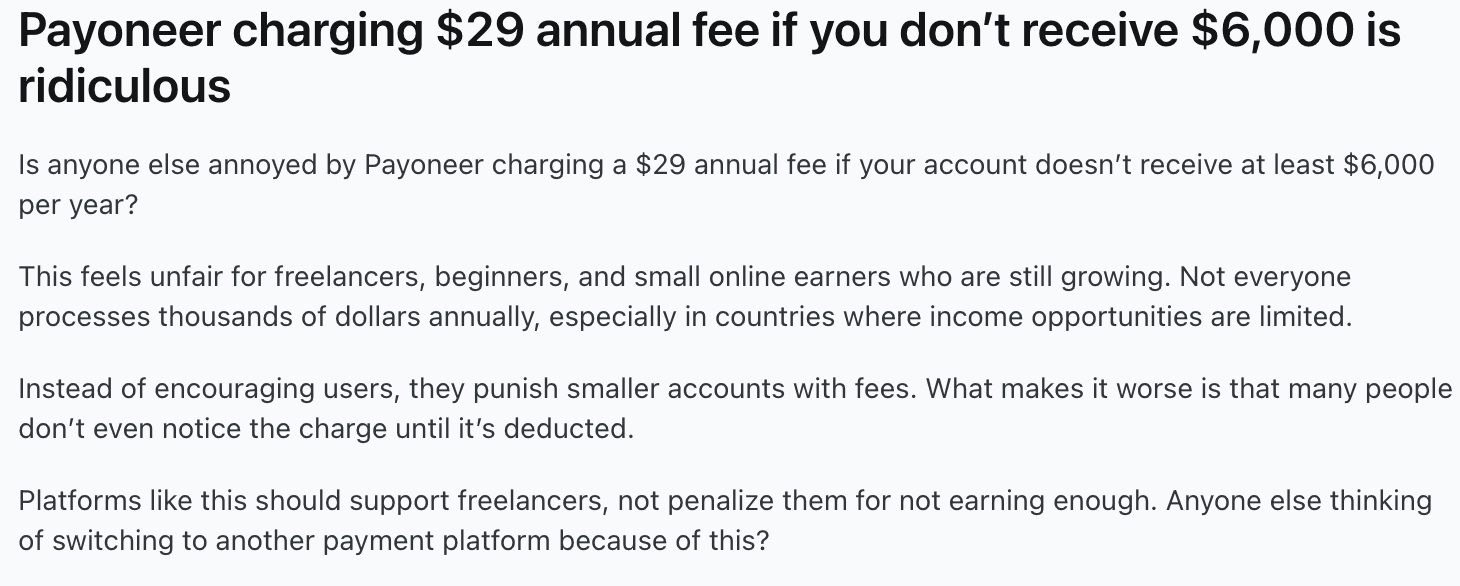

5. $29.95 annual inactivity fee.

If your account receives less than $2,000 in any 12-month period, Payoneer applies a $29.95 inactivity fee.

Source: Reddit

6. Limited direct B2B payment flexibility.

Payoneer works well within its marketplace ecosystem. For businesses that work directly with clients or enterprises via bank transfers, Payoneer is comparatively less user-friendly.

7. FIRA documentation is available, but not always seamless.

Payoneer provides FIRA for Indian users, but the per-transaction compliance experience is not very automated or instant.

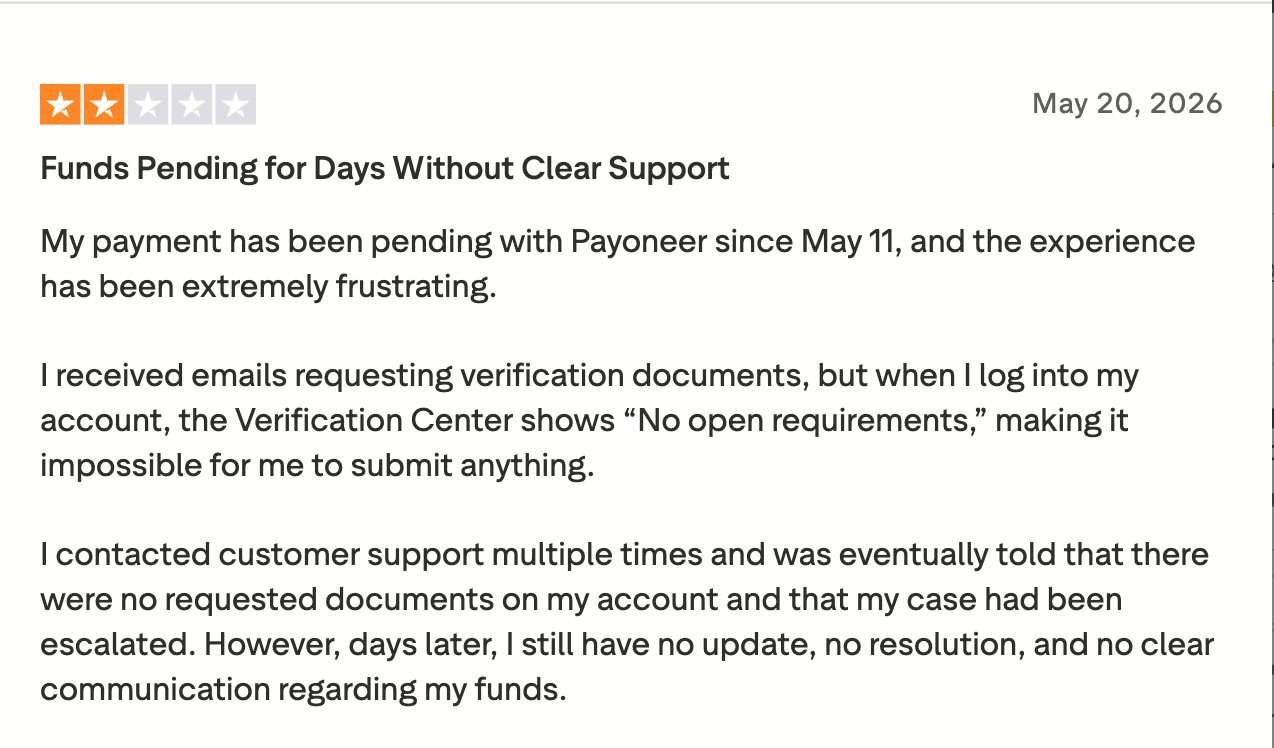

8. Customer support gaps.

Many Indian users report difficulty in reaching out to customer support, particularly for account limitation queries, which are often the most urgent situations.

Source: Trustpilot

How We Evaluated Each Alternative

Every platform on this list was assessed against the same criteria relevant for Indian professionals who receive international payments.

Total effective fee: platform fee plus FX markup plus any compliance document charges, expressed as a true all-in percentage

FX policy: Does the platform convert at the live mid-market rate, or apply a hidden spread?

INR settlement speed: hours or business days to your Indian bank account

FIRA/eFIRC: automatic, free, and per-transaction vs manual, paid, or batched

India entity support: freelancers, other business types, including Pvt Ltd and LLPs.

Receiving methods: local rails (ACH, SEPA, Faster Payments) vs SWIFT only

Invoice or transaction limits: any caps that would block large payments?

RBI and FEMA compliance: PA-CB licence, AD-1 bank partnerships, or equivalent

Direct B2B use: Can you invoice clients directly, or only receive from integrated platforms?

Practical limitations: what the platform does not do well, stated plainly

7 Best Payoneer Alternatives For International Payment

Platform | Best For | Fees | FX Markup | Settlement | Free FIRA | Invoice Cap | India Entity Types | Receiving Methods |

Direct invoicing, all businesses | 0.5% all-in | Zero | 24 hours | Auto | None | All | Local rails + Payment Link | |

FX transparency, multi-currency | ~1.65% + GST | Zero | 1–2 days | $2/cert | ₹25L (new limit) | Freelancers/sole props | Local rails | |

Global buyer familiarity | 4.4% + $0.30 | 3–4% | 2–5 days | Monthly batch | $10,000 | All | Card + bank | |

SaaS/card checkout | 4.3% + 2% FX | 2% | 7+ days | No | None | All (invite-only) | Card payments | |

Domestic + international combo | 1–3% + GST | Zero (export a/c) | T+7 days | Available | None | All | Bank transfer + card | |

Multi-currency wallet, enterprise | ~0.5–1.0% + FX | ~0.5–1% | 1–2 days | Not confirmed | None | Companies (Singapore entity) | Local rails + SWIFT | |

Digital wallet, P2P, small amounts | 1.45% + 3.99% FX | 3.99% | 1–3 days | No | Varies | Individuals/freelancers | Wallet + bank |

#1. Infinity - Best for Indian Businesses Receiving International Payments

Infinity is a YC-backed, international payment platform built for businesses for Indian inward remittances. Unlike Payoneer, which was designed around marketplace ecosystem payouts, Infinity was built for direct client invoice collections. This is where most Indian professionals actually lose most of their money on fees.

The working of Infinity is very simple: you will get a virtual multi-currency account in 50+ currencies (USD, GBP, EUR, AUD, CAD, SGD). Your overseas client will pay into your Infinity virtual account using their domestic payment rails. Infinity converts at the live mid-market rate with zero markup, and settles INR to your Indian bank in 24 hours, with free and automated FIRA. The entire process costs you 0.5% (inclusive of GST, platform fee, FX conversion, and FIRA).

Who it is for:

Infinity is ideal for Indian freelancers, agencies, IT exporters, SaaS businesses, consultants, and exporters receiving international payments.

Who should not use it for:

Marketplace-dependent professionals receiving payment from Upwork, Fiverr, or Amazon, where Payoneer's integration is the best.

Pricing and Fees of Infinity and Payoneer

Fee Component | Infinity | Payoneer |

Platform / receiving fee | 0.5% (all-in) | 1–3% |

FX markup on INR withdrawal | Zero | Up to 3% |

FIRA | Free, auto, per transaction | Free but less automated |

Inactivity fee | None | $29.95/year |

Settlement | 24 hours | 2–5 business days |

Effective total cost | 0.5% | 4–7% |

Fee Examples: Three Payment Scenarios

Scenario 1: $1,000 invoice (typical freelance project)

Infinity | Payoneer | |

Fee deducted | $5.00 | $10 (1%) + $25 FX (2.5%) = $35 |

You receive | ~$995 | ~$965 |

Difference | — | $30 less |

Scenario 2: $3,000 agency retainer

Infinity | Payoneer | |

Fee deducted | $15.00 | $30 (1%) + $75 FX (2.5%) = $105 |

You receive | ~$2,985 | ~$2,895 |

Difference | — | $90 less |

Scenario 3: $10,000 B2B export invoice

Infinity | Payoneer | |

Fee deducted | $50.00 | $100 (1%) + $250 FX (2.5%) = $350 |

You receive | ~$9,950 | ~$9,650 |

Difference | — | $300 less |

On $10,000/month in regular international income, Infinity saves approximately ₹25,000–₹30,000 per month versus Payoneer.

#2. Wise - Best for Transparent FX and Multi-Currency Transfers

Wise (formerly TransferWise) is a UK-based payment platform that serves 16 million+ customers globally. The real USP of Wise is the real mid-market exchange rate with a clearly disclosed fee. In India, Wise received in-principle RBI approval to operate as a Payment Aggregator – Cross Border in early 2026. This has opened the door to higher transaction limits (up to ₹25 lakh for freelancers and businesses).

Wise is a better payment method over Payoneer in terms of cost for many use cases. Its limitations for Indian users are specific and worth understanding before committing.

Who it is for:

Wise is ideal for individual freelancers and sole proprietors receiving international payments in multiple currencies. This is a good option for users who want a multi-currency wallet and transparent, zero-markup FX conversion.

Who should look elsewhere:

Private limited companies and LLPs (Wise's India business account currently supports freelancers and sole proprietors only). Businesses need GST-compliant invoicing. Users who need per-transaction FIRA at no cost.

Also Read: 5+ Best Wise Alternatives For International Payments in India

Pricing and Fees of Wise and Payoneer

Fee Component | Wise | Payoneer |

Conversion fee | ~1.65% | 1% receiving + up to 3% FX |

FX markup | Zero (mid-market rate) | Up to 3% |

FIRA | $2 per certificate | Free |

GST on conversion fee | 18% | N/A |

Settlement | 1–2 business days | 2–5 business days |

Effective all-in cost | ~2% (incl. FIRA + GST) | 4–7% |

Real-world cost on a $3,000 payment:

Wise | Payoneer | |

Fee deducted | ~$60 (~2%) | ~$90–$120 (3–4%) |

You receive | ~$2,940 | ~$2,880–$2,910 |

Wise is cheaper than Payoneer on a pure cost basis for most direct payment scenarios. But at ~2% all-in (including GST and FIRA), it is still 4x the cost of Infinity's 0.5%.

#3. PayPal - Global Recognition, High Cost

PayPal is the most globally recognised online payment platform. It is used by 400 million+ accounts in 200+ countries. Its primary value for Indian professionals is familiarity. This means that overseas clients in the US and Europe often default to PayPal because they already have an account and can pay in seconds. For occasional, low-value invoices where client friction is the biggest concern, PayPal can still serve a purpose.

The Fee reality, however, is stark. PayPal's combined effective cost for Indian users is equal to the transaction fee (4.4% + $0.30) plus 3–4% FX markup on forced INR conversion that sits at 7–9% per transaction. Although Indian accounts cannot hold foreign currency, all incoming payments are automatically converted to INR within 24 hours at PayPal's rate.

Who it is for:

PayPal is good for small invoices (under $300–$500) where the client specifically insists on PayPal.

Who should not use it:

Anyone receiving regular international payments. The effective 7–9% cost has no business justification when platforms like Infinity charge 0.5% for a better overall experience.

Read -

Pricing and Fees of PayPal and Payoneer

Fee Component | PayPal | Payoneer |

Transaction fee | 4.4% + $0.30 | 1–3% |

FX markup | 3–4% | Up to 3% |

FIRA | Monthly batch | Free |

Account freeze risk | Widely documented | Documented |

Effective total cost | 7–9% | 4–7% |

Real-world cost on a $1,000 payment:

PayPal | Payoneer | Infinity | |

Fee deducted | $74–$84 | $35–$40 | $5 |

You receive | ~$916–$926 | ~$960–$965 | ~$995 |

#4. Stripe - Payment Infrastructure, Not a Receiving Account Replacement

Stripe is the world's most powerful payment infrastructure platform, used by over 1 million businesses globally. It is known for API-driven checkout flows, subscription billing, and SaaS payment integration. It is important to understand what Stripe is and is not: Stripe is a payment gateway for accepting card payments from customers, and not just a receiving account for collecting client invoices via bank transfer. Comparing it directly to Payoneer is like comparing a checkout system to a bank account.

Stripe is genuinely useful if you are building a SaaS product, marketplace, or e-commerce platform that charges international customers by card. This is because Stripe's API capabilities and subscription management infrastructure are the gold standard. It operates in India on an invite-only basis.

Who it is for:

Stripe is best for developer-led SaaS companies, subscription businesses, and e-commerce platforms that need powerful payment APIs, custom checkout flows, and international card acceptance as part of their product.

Who should not use it:

Freelancers, exporters, or agencies looking for a simple way to receive bank-transfer payments from clients. Stripe does not provide FIRA, which is a critical compliance gap for Indian exporters.

Pricing and Fees of Stripe and Payoneer

Fee Component | Stripe | Payoneer |

International card transaction | 4.3% | 1–3% receiving fee |

FX conversion | 2% | Up to 3% |

FIRA | Not provided | Free |

India availability | Invite-only | Open |

Effective total cost (card) | ~6–7% | 4–7% |

Stripe's effective cost for Indian merchants on international card payments (~6–7%) is comparable to Payoneer's effective cost, but Stripe earns its premium through developer tooling and checkout quality, not as a cost-efficient receiving account.

#5. Razorpay - Best for Businesses Needing Both Domestic and International

Razorpay is India's largest payment gateway, serving 10 million+ Indian merchants. Its domestic infrastructure- UPI, net banking, cards, EMI, Pay Later, is the most comprehensive in India. For international payments, Razorpay has launched MoneySaver Export Account (via RazorpayX) that allows Indian businesses to receive cross-border bank transfers at 1% + GST and zero FX markup.

The key limitation of RazorpayX is the settlement speed. Razorpay takes T+7 business days for international payments to settle in INR. This is the slowest of any platform in this comparison. For businesses that are already integrated with the Razorpay ecosystem for domestic commerce, adding the MoneySaver Export Account is a logical move. For businesses looking for fast and cheap international payments, Infinity is a better choice.

Who it is for:

RazorpayX is ideal for indian businesses that need both domestic payments (UPI, cards, net banking) and international collections on one integrated platform.

Who should not use it:

RazorpayX is not suitable for businesses whose primary pain point is settlement speed.

Pricing and Fees of Razorpay and Payoneer

Fee Component | Razorpay | Payoneer |

International bank transfers | 1% + 18% GST (~1.18%) | 1% receiving |

International card payments | 3% + 18% GST (~3.54%) | 1–3% |

FX markup | Zero (MoneySaver Export A/c) | Up to 3% |

Settlement | T+7 business days | 2–5 business days |

FIRA | Available | Free |

Effective cost (bank transfer) | ~1.18% | 4–7% |

Real-world cost of a $5,000 bank transfer:

Razorpay | Payoneer | Infinity | |

Fee deducted | ~$59 (1.18%) | ~$150–$200 (3–4%) | $25 (0.5%) |

You receive | ~$4,941 | ~$4,800–$4,850 | ~$4,975 |

#6. Airwallex - Best for Multi-Currency Wallets and Enterprise FX

Airwallex is a global fintech payment platform headquartered in Australia, supporting 60+ currencies. Indian businesses can onboard under Airwallex Singapore Pte. Ltd. This means you will operate under Singapore licensing rather than Indian banking regulation. This is an important distinction: automatic FIRA/eBRC issuance is not confirmed for Indian users, and the product availability follows Singapore entity rules rather than Indian compliance frameworks.

Airwalllex genuinely stands out in its multi-currency wallet capabilities. Just like Infinity, Airwallex allows Indian businesses to hold foreign currency that they receive in USD, EUR, or GBP and convert to INR when rates are favourable to them. This eliminates forced conversion. This is particularly useful for businesses with USD-denominated expenses or for those managing FX exposure strategically.

Airwallex pricing that has been disclosed publicly shows a 0.5% above interbank rate for major currencies and ~1.0% for others. Although its exact fees depend on entity type and plan.

Who it is for:

Airwallex is suitable for Indian companies (particularly Pvt Ltd entities and larger exporters) that need multi-currency wallets and want to hold foreign currency.

Who should look elsewhere:

Businesses that need confirmed automatic FIRA for every transaction, or sole proprietors and freelancers who want a simpler India-native compliance workflow. Verify FIRA availability directly during onboarding before committing.

Pricing and Fees of Airwallex and Payoneer

Fee Component | Airwallex | Payoneer |

FX conversion | ~0.5–1.0% above interbank | Up to 3% |

Receiving (local rails) | No setup fee is typical | 1% |

FIRA | Not confirmed (verify at onboarding) | Free |

Settlement to INR | 1–2 days | 2–5 days |

Foreign currency holding | ✅ Yes | Limited |

Approximate effective cost | ~0.5–1% | 4–7% |

Real-world cost on a $5,000 payment (approximate):

Airwallex | Payoneer | Infinity | |

Fee deducted | ~$25–$50 (0.5–1%) | ~$150–$200 (3–4%) | $25 (0.5%) |

You receive | ~$4,950–$4,975 | ~$4,800–$4,850 | ~$4,975 |

#7. Skrill - Consumer Digital Wallet, Limited Business Depth

Skrill, part of the Paysafe Group since 2015, is a digital wallet platform operating in 120+ countries, supporting ~40 currencies. It is best understood as a consumer-oriented digital payment tool. Skrill is mostly useful for receiving small payments, spending online globally, and sending money between accounts.

For Indian freelancers doing occasional international work, Skrill offers a low-friction way to receive small payments. You can access funds via a prepaid Mastercard and transact across borders without complex onboarding. However, its India-specific limitations are significant. This includes- Skrill charges a 3.99% FX markup on Skrill-to-Skrill transfers, does not provide FIRA for Indian users, and has no compliance infrastructure tailored to Indian FEMA requirements.

Who it is for:

Skrill is best for individual freelancers receiving occasional small payments from international clients who need a quick digital wallet. It is also suitable for gaming platform users, digital nomads, and users who need a simple P2P payment option.

Who should not use it:

Skrill is not suitable for any Indian business or serious freelancer receiving regular international income. The 3.99% FX markup on Skrill-to-Skrill transfers and absence of FIRA make it unsuitable for professional-grade cross-border payment collection or FEMA compliance.

Pricing and Fees of Skrill and Payoneer

Fee Component | Skrill | Payoneer |

Receiving fee | 1.45% typically | 1–3% |

FX markup (Skrill-to-Skrill) | 3.99% above the Reuters rate | Up to 3% |

Prepaid card annual fee | €10 application + €10/year | N/A |

ATM withdrawal | 1.75% | N/A |

FIRA for India | Not provided | Free |

Effective cost (international) | ~5–6% | 4–7% |

Skrill is not meaningfully cheaper than Payoneer, and is significantly worse on compliance documentation. Its primary advantage is the speed of setup and the global prepaid card. This may serve specific use cases, but it does not make it a credible Payoneer replacement for Indian business payments.

Fee Examples: Landed Amount Across Three Real Scenarios

Scenario A: Freelance developer receives a $2,000 project invoice

Platform | Fee/Cost | You Receive | Settlement |

Infinity | $10 (0.5%) | $1,990 | 24 hours |

Wise | ~$40 (~2%) | ~$1,960 | 1–2 days |

Razorpay (bank) | ~$23.60 (1.18%) | ~$1,976 | T+7 days |

Payoneer | ~$60–$80 (3–4%) | ~$1,920–$1,940 | 2–5 days |

PayPal | ~$148–$160 (7–8%) | ~$1,840–$1,852 | 2–5 days |

Scenario B: IT services exporter receives a $5,000 monthly invoice

Platform | Fee/Cost | You Receive | Settlement |

Infinity | $25 (0.5%) | $4,975 | 24 hours |

Airwallex | ~$25–$50 (~0.5–1%) | ~$4,950–$4,975 | 1–2 days |

Wise | ~$99–$102 (~2%) | ~$4,898–$4,901 | 1–2 days |

Payoneer | ~$150–$200 (3–4%) | ~$4,800–$4,850 | 2–5 days |

PayPal | ~$370–$420 (7–8%) | ~$4,580–$4,630 | 2–5 days |

Scenario C: Agency receives a $10,000 enterprise client invoice

Platform | Fee/Cost | You Receive | Settlement |

Infinity | $50 (0.5%) | $9,950 | 24 hours |

Razorpay (bank) | ~$118 (1.18%) | ~$9,882 | T+7 days |

Wise | ~$192–$200 (~2%) | ~$9,800–$9,808 | 1–2 days |

Payoneer | ~$300–$400 (3–4%) | ~$9,600–$9,700 | 2–5 days |

PayPal | ~$740–$840 (7–8%) | ~$9,160–$9,260 | 2–5 days |

The pattern is consistent across all three scenarios: Infinity delivers the highest landed amount at every invoice size, and the gap between Infinity and PayPal widens as invoice values increase.

Which Platform to Choose by User Type

Indian freelancers billing direct international clients. Use Infinity. The 0.5% all-in fee, free auto-FIRA, 24-hour settlement, and zero FX markup deliver the best landed amount on every invoice.

Freelancer earning primarily through Upwork, Fiverr, or Toptal. Use Payoneer for marketplace payouts. The native integrations cannot be fully replicated. Add Infinity for any direct client invoicing outside the marketplace ecosystem. This will help in minimising the total fees across all income streams.

Agency or consultancy receiving B2B invoices from international clients. Use Infinity for direct invoice collections. Consider Razorpay if you also need domestic payment infrastructure (UPI, cards) on one platform.

SaaS company accepting card payments from international subscribers. Use Stripe for your checkout and subscription billing infrastructure. You can add Infinity as well for any direct invoice-based collections from enterprise clients.

IT exporter or goods exporter with large, irregular invoices. Use Infinity in such cases.

Indian companies that need to pay international contractors and a remote team. Use Deel. It is built for contractor payout management across 150+ countries with compliance documentation and contract management included.

Freelancers need a simple digital wallet with a prepaid card for small amounts. Use Skrill for occasional small payments and online spending. Although it's not recommended for receiving regular international payments.

FAQs on Payoneer Top Alternatives in India

Q1. Is Payoneer legal and RBI-compliant in India?

Yes. Payoneer holds in-principle RBI PA-CB (Payment Aggregator – Cross Border) approval for India and operates within FEMA guidelines.

Q2. Payoneer vs Wise - which is better for Indian freelancers?

Wise is better than Payoneer for direct invoice collections, as it is cheaper than Payoneer. Wise also applies zero FX markup. However, Wise only supports freelancers and sole proprietors in India, and it has a per-transaction FIRA charge of $2. Payoneer's 500+ marketplace integrations make it indispensable for platform-dependent income.

Q3. Payoneer vs PayPal - which should Indian exporters use?

Payoneer is cheaper than PayPal for most Indian exporters. Payoneer also provides per-transaction FIRA (versus PayPal's monthly batch), and has a better settlement timeline.

Q4. What is the best Payoneer alternative for Indian freelancers in 2026?

Infinity is the best alternative for freelancers invoicing clients directly. It offers 0.5% all-in fee, zero FX markup, 24-hour settlement, and free automatic FIRA with every transaction.

Q5. Which Payoneer alternative settles to INR the fastest?

Infinity settles INR to your Indian bank account within 24 hours. It is the fastest of any platform in this comparison.

Q6. Can I use Infinity and Payoneer at the same time?

Yes, you can use Payoneer and Infinity at the same time. Use Payoneer for all marketplace integration income (Upwork, Fiverr, Amazon). And use Infinity for all direct client invoicing that is outside the marketplace ecosystem, where Infinity charges just 0.5% on all transactions.