Discover infinity

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

Receiving EUR payments in India is not just about choosing the fastest method. For all the freelancers, exporters, SaaS founders, and agencies receiving international payments in India, receiving EUR payments means considering a lot of factors before you choose the right payment platform. These factors include settlement time, FIRC/FIRA documentation, purpose codes, and tax records.

A lot of guides online compare logos and screenshots. This guide does something different: it compares the safest ways to receive EUR payments in India, explains when each method makes sense, and shows you how much money you may actually receive after fees and conversion.

Whether you are a Bangalore-based consultant billing a German company, or a Mumbai agency with a French client, the INR that lands into your bank account totally depends on the method of payment you choose.

Quick Answer: Best Way to Receive EUR Payments in India

Use Case | Recommended Method |

Best overall for Indian freelancers/agencies/exporters | Infinity |

Best for EU domestic rails (SEPA/ACH) | Virtual EUR Account |

Best for marketplace payouts | Payoneer |

Best for client familiarity | PayPal (but expensive) |

Best for direct bank transfer | SWIFT (slow and cost-heavy) |

Best for checkout/card/SaaS payments | Stripe / Razorpay / Cashfree |

Best for transparent, simple transfers | Wise (where available) |

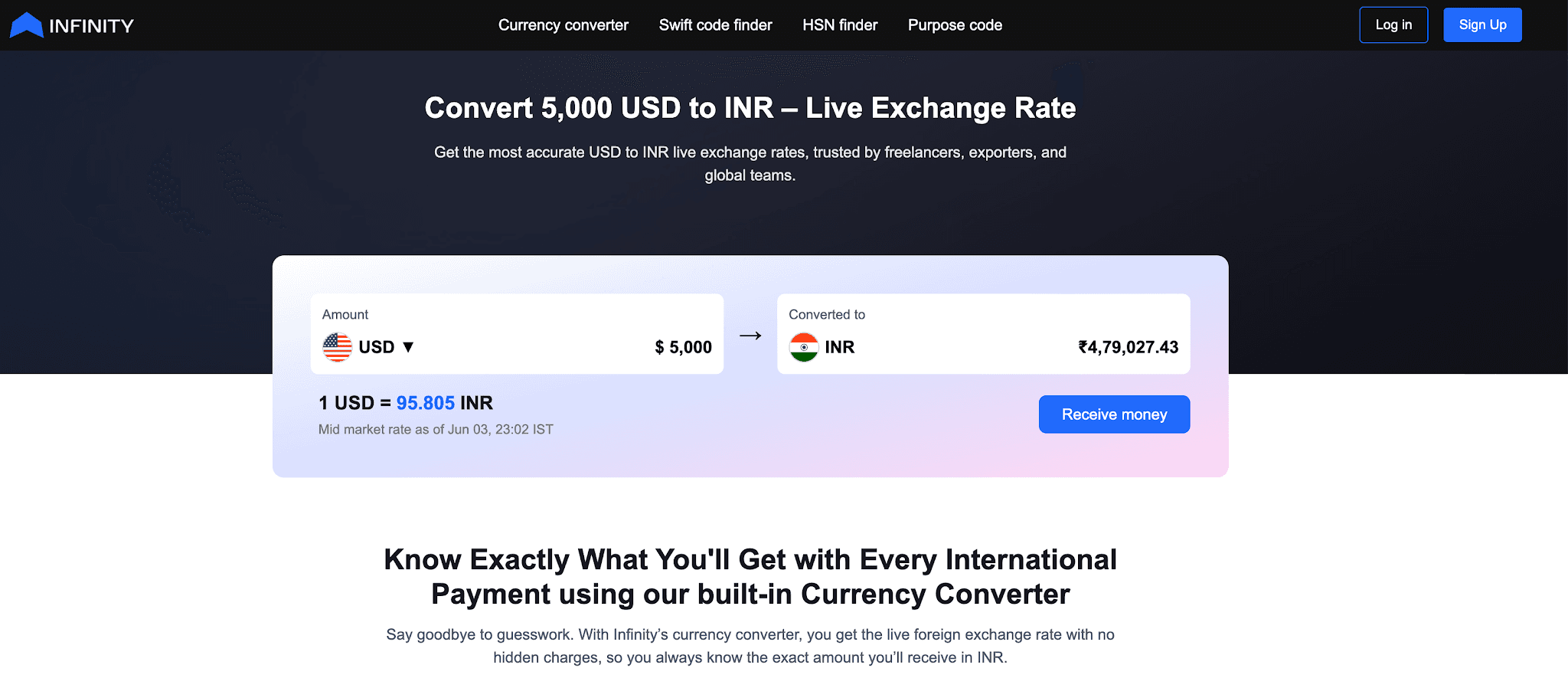

Want to know how much INR you will actually receive? Use Infinity's EUR to INR Calculator at tools.infinityapp.in/currency-converter/eur-to-inr

Can You Legally Receive EUR Payments in India?

Yes, you can receive EUR payments legally in India. However, the payment must travel through regulated banking or payment channels. These payment platforms or banking channels must comply with the FEMA ( Foreign Exchange Management Act) and the RBI (Reserve Bank of India) guidelines.

Let's see how the compliance looks for international payments in India:

Payments must flow through authorised dealer banks or regulated payment platforms.

You must maintain proper invoices, client contracts, and payment records.

Each inward remittance should have a purpose code assigned at the time of receipt.

You must obtain a Foreign Inward Remittance Advice (FIRA) or Foreign Inward Remittance Certificate (FIRC) from your bank or payment platform.

If you export services and are registered under GST, you may need to file a Letter of Undertaking (LUT) to receive payment without charging IGST.

Payment realisation must happen within the prescribed time limits under FEMA.

Affordable and cheap routes do not necessarily mean safe routes for receiving EUR payments in India. It means using compliant rails that give you a clean paper trail, proper FX documentation, and the ability to reconcile payments in your books without risk.

What Documents Do You Need to Receive EUR in India?

Before you compare platforms or payment methods, make sure you have the following documents in order. These apply whether you are a solo freelancer or a registered company.

Commercial invoice with EUR amount, your business details, client details, and purpose of payment.

Client agreement, purchase order, or work order (even a simple email confirmation helps).

PAN card (mandatory for individuals and businesses).

GST registration certificate, if applicable.

Bank account details or a payment platform account for receiving funds.

KYC documents as required by your bank or payment platform.

Purpose code (assigned at the time the payment is received, based on the nature of service or export).

FIRA after every successful transaction.

LUT filing acknowledgement, if you export services under GST without charging IGST

Payment advice or transaction reference from the sender

Accounting record showing EUR amount received, INR equivalent, exchange rate applied, and fees deducted

Create a separate folder for each client's payments. These folders can contain documents like FIRA, invoices, payment references, and bank credit confirmation. This will make the compliance process less stressful.

Also Check:

7 Safe Ways to Receive EUR Payments in India in 2026

Method | Best For | Cost Level | Speed | Compliance Support | Main Benefit | Watch Out For |

|---|

Infinity | Freelancers, agencies, exporters, SaaS founders | Low | Fast | Strong | 0.5% all-inclusive fee, zero FX markup, free FIRA | Newer than legacy options |

SWIFT Bank Transfer | Large B2B payments | High | Slow | Strong | Trusted and accepted by banks globally | FX markup, intermediary deductions, manual follow-up |

Virtual EUR Account | EU clients who prefer local bank transfers | Medium | Fast | Depends on the provider | Gives EU-style IBAN details for easier client payments | Not every provider supports Indian compliance properly |

Wise | Simple EUR transfers with transparent pricing | Medium | Fast | Limited / route-dependent | Clear fees and transparent FX rate | May not fully support Indian export documentation |

PayPal | One-off payments or clients who insist on PayPal | Very High | Medium | Limited | Very familiar to global clients | High fees, FX markup, account holds |

Payoneer | Upwork, Fiverr, Amazon, marketplace payouts | Medium | Medium | Moderate | Strong marketplace integrations | Less ideal for direct client invoices |

Stripe / Razorpay / Cashfree | SaaS, subscriptions, e-commerce checkout | Medium to High | Medium | Moderate | Best for card payments and checkout flows | Not built for invoice-based EUR receivables |

Method 1: Infinity

Best for: Infinity is ideal for Indian freelancers, exporters, Saas founders, agencies and SMBs in India, receiving payments from European clients.

Pros:

Infinity charges 0.5% (inclusive of all), with zero hidden charges.

Infinity provides instant and free-of-cost FIRA for every successful transaction.

Infinity does not charge any FX markup on the currency conversion. This means you can convert your foreign currency at the live FX rate.

Infinity provides you with a payment tracking dashboard so that you can track your money in real-time.

Infinity supports compliance by helping you with the right purpose codes and other information.

Cons:

Newer platform compared to legacy options like PayPal or SWIFT.

Client must be comfortable using the Infinity payment flow.

Note: Infinity's 0.5% all-inclusive fee combined with zero FX markup makes it one of the most cost-efficient ways to receive EUR in India in 2026. On a EUR 5,000 payment, the difference between Infinity and a traditional bank wire (with 2% FX markup) can be INR 8,000 or more in your pocket.

Method 2: Direct Bank Wire Transfer Through SWIFT

Best for: SWIFT is suitable for large B2B invoices. It is preferable for those clients who have a good banking relationship. Or in those cases where the clients insist on traditional wise transfers.

Pros:

SWIFT is universally accepted by every major bank in most countries.

SWIFT is fully regulated and in compliance with RBI/FEMA guidelines.

FIRA/FIRC provided by banks is considered to be the strongest documentation.

SWIFT is generally considered suitable for very large B2B transactions.

Cons:

Slow — typically takes 2 to 5 business days to settle.

Intermediary bank deductions can reduce the amount you receive unpredictably.

FX markup on bank conversion is often 1.5% to 3%, which significantly reduces INR realisation.

The receiving bank may charge additional fees.

Manual follow-up is often required for documentation and FIRC.

No real-time tracking of where the payment is in transit

Note: On a EUR 5,000 wire, the visible fee may look small upfront. But combined FX markup and intermediary deductions can quietly reduce your final INR credit by INR 6,000 to INR 10,000 compared to a zero-markup platform. Always compare the all-in cost, not just the wire fee.

Method 3: Virtual EUR Account

Best for: Virtual EUR accounts are best for EU clients who prefer domestic SEPA bank transfers. It is a good option for freelancers and other businesses that frequently receive payments from multiple EU sources.

Pros:

A virtual EU account gives your client EU-style IBAN routing details. So, this feels like a domestic transfer to your EU clients.

It removes the friction for the EU clients who are not familiar with wire transfers.

The virtual EUR account works well for recurring payments.

Cons:

The platform providing the virtual account must be KYC-compliant and support proper INR settlement.

Not all virtual EUR account providers support the documentation workflow required for Indian export compliance.

Because of the virtual EU account, withdrawal fees and FX spread can vary from platform to platform.

Note: A virtual EUR account is a client experience improvement, not a compliance shortcut. The platform you use still needs to provide proper FIRA-equivalent documentation, KYC, and purpose code support for your payments to be fully compliant in India.

Method 4: Wise

Best for: Wise is preferable to those who prioritise transparent FX pricing with a global name. Wise is a suitable payment mode for those who do not need a complex India-specific compliance workflow.

Pros:

With mid-market-style FX rate communication, you can see exactly what rate you are getting.

Transparent fee structure before you confirm the transfer

Strong global trust and brand recognition

Easy to use for personal and smaller professional transfers

Cons:

Route and account availability for Indian users can vary and are subject to change.

Business support and documentation workflow may not fully cover every Indian exporter's compliance needs.

Not always optimal for high-volume B2B export invoice payments requiring FIRA and purpose code documentation

FX fees, while transparent, can still add up on larger transfers.

Note: Wise is a strong option for straightforward transfers where transparency is the priority. However, if you are running a business, billing EU clients regularly, and need full GST/FEMA compliance documentation, you may need to supplement Wise with additional steps.

Method 5: PayPal

Best for: One-off client payments, clients who insist on PayPal, independent creators, and small transactions where convenience matters more than cost-efficiency.

Pros:

Extremely high global recognition — most EU clients know how to use it.

Easy payment link and email-based payment flow.

Buyer protection features that some clients find reassuring.

Quick setup for new clients with no banking complexity.

Cons:

Transaction fees are among the highest, often 3.5% to 5% of the payment amount.

Significant FX markup on conversion from EUR to INR.

Account holds and payment disputes can freeze your funds without clear resolution timelines.

Currency conversion happens at PayPal's rate, not the market rate.

Not suitable for serious recurring B2B EUR income due to cumulative cost.

Limited documentation workflow for Indian export compliance.

Note: PayPal is safe and globally familiar, but it is rarely the most cost-efficient way to receive EUR in India. On a EUR 5,000 payment, PayPal's combined fee and FX markup can cost you INR 15,000 to INR 20,000 more than a zero-markup platform.

Method 6: Payoneer

Best for: Marketplace payouts from platforms like Upwork, Fiverr, Amazon, or similar ecosystems, and freelancers who need virtual receiving accounts for multiple currencies.

Pros:

Deep integration with major freelance and e-commerce marketplaces.

Multi-currency virtual receiving account details.

Widely used and trusted by the Indian freelance community.

Relatively straightforward withdrawal to Indian bank accounts.

Cons:

Fee and FX spread can accumulate, especially on withdrawal to INR.

Account holds and support issues are frequently reported by Indian users.

Not always the best workflow for direct client-to-freelancer invoice payments outside marketplaces.

Documentation for Indian export compliance may require additional manual effort.

Note: Payoneer is the go-to for marketplace payouts. If you are receiving EUR directly from clients rather than through a marketplace, a platform built specifically for that use case, like Infinity, will usually offer better rates and smoother compliance.

Method 7: Payment Gateways and Checkout Tools (Stripe, Razorpay, Cashfree)

Best for: SaaS businesses with subscription billing, e-commerce platforms, online product sales, and any business that needs card-based checkout flows from European customers.

Pros:

Full card acceptance, including Visa, Mastercard, and European card networks.

Recurring subscription billing support with a robust API.

Strong checkout and developer tooling for product businesses.

Fraud protection and payment security are built in.

Cons:

Not a direct replacement for invoice-based EUR receivables from clients.

International card transaction charges can be 2% to 4% on top of processing fees.

Onboarding eligibility for Indian businesses may vary by platform and business type.

Documentation and compliance flow is designed for checkout, not export invoice realisation.

Currency settlement terms and FX handling vary by platform.

Note: If you are running a SaaS product or selling digital products to European customers, Stripe or Cashfree handles your checkout. If you are billing EU clients on invoices for services, use a platform like Infinity for those receivables. They solve different problems.

Cost Comparison: How Much INR Do You Receive from a EUR Payment?

The table below illustrates the approximate impact of fees and FX markup across the main methods, using EUR 5,000 as the example. Always check live rates before you transact, and use Infinity's EUR to INR calculator for real-time figures.

Method | Client Sends | Visible Fee | FX Markup | Settlement Time | Documentation | Approx INR Received |

Infinity | EUR 5,000 | 0.5% | 0% markup | ~24 hours | FIRA/compliance support included | Highest — use live converter |

Bank Wire (SWIFT) | EUR 5,000 | Fixed + bank charges | 1.5–3% typical | 2–5 business days | Bank FIRA (manual follow-up) | Reduced by FX spread + deductions |

PayPal | EUR 5,000 | High % fee (3.5%+) | Platform FX markup | Varies | Limited export workflow | Often lowest of all options |

Payoneer | EUR 5,000 | Platform fee ~2% | FX spread on withdrawal | Varies | Depends on account type | Mid-range |

Wise | EUR 5,000 | Variable (transparent) | Near mid-market rate | 1–2 business days | Route-specific documentation | Mid to high |

Virtual EUR Account | EUR 5,000 | Withdrawal fee varies | Platform-dependent | 1–3 business days | KYC-compliant platform needed | Mid to high |

Live tool: Use Infinity's currency converter at https://tools.infinityapp.in/currency-converter?eur-to-inr to see exactly how much INR you will receive from your EUR payment, updated in real time.

Which Method Should You Choose?

User Type | Best Option | Why |

Freelancer with direct EU clients | Infinity / Virtual EUR Account | Lower cost, easier client payment, FIRA documentation |

Freelancer on Upwork/Fiverr | Payoneer | Marketplace integrations built-in |

Agency billing EU clients | Infinity | Invoice management, settlement, compliance tracking |

Exporter (B2B) | Infinity or SWIFT (depending on size) | Documentation and compliant payment realisation |

SaaS company | Stripe/Cashfree for checkout; Infinity for invoices | Different payment jobs, match the tool to the use case |

Remote contractor | Virtual EUR Account or Infinity | Client-side ease + smooth India settlement |

Client insists on PayPal | PayPal | Convenience, despite higher cost, is accepted and adjusted |

What Is the Safest Way to Receive EUR in India?

The safest method combines all of the following elements:

Regulated payment rails with RBI/FEMA compliance.

Clear KYC at both account opening and transaction level.

Transparent fee and FX rate — no hidden markup.

Proper purpose code assignment at the time of receipt.

FIRA or FIRC is provided automatically after each payment.

Complete invoice and payment trail for GST and tax records.

Direct settlement to your own Indian bank account — not a third-party account.

Clean accounting records showing EUR received, INR credited, rate applied, and fees deducted.

Infinity is built to deliver all of these in one workflow. Rather than assembling compliance pieces manually across a bank, an accountant, and a payment platform, Infinity handles regulated collection, FIRA documentation, and INR settlement in a single process designed for Indian freelancers, agencies, and exporters.

Mistakes to Avoid When Receiving EUR in India

Accepting business payments into a family member's or friend's account — this is a FEMA violation and creates serious tax complications.

Ignoring purpose codes — every inward remittance must have a purpose code, and leaving it blank or wrong invites scrutiny.

Not collecting FIRA or FIRC — without this, you cannot prove the source and nature of the foreign income.

Choosing PayPal simply because it is familiar — familiarity costs you INR 15,000–20,000 per EUR 5,000 payment compared to better alternatives.

Comparing only the transaction fee while ignoring FX markup — a 0% fee platform with a 2% FX spread is more expensive than a 0.5% fee platform with 0% markup.

Using crypto or stablecoins casually for business income — this creates complex tax reporting obligations and is not a compliant substitute for regulated payment realisation.

Not filing LUT when required — if you export services under GST and do not want to charge IGST, you must file the LUT with your GST authority before raising invoices.

Not matching invoices with payment receipts — every bank credit must correspond to a specific invoice in your records.

Ignoring GST treatment of export income — zero-rated exports still require proper filing and documentation.

Step-by-Step: How to Receive EUR Payments with Infinity

Create your Infinity account at the Infinity website.

Complete KYC — submit your PAN, business details, and bank account for INR settlement.

Generate an invoice or payment link within the platform, or share your Infinity payment details with your EU client.

Your client pays in EUR from their bank account or payment method.

Track payment status in real time on your Infinity dashboard.

Receive INR settlement directly into your linked Indian bank account — typically within 24 hours.

Download your FIRA and compliance documentation from the platform for your records.

Record the payment in your accounting files: EUR amount, INR credited, exchange rate, fees, and invoice reference.

Ready to receive EUR from EU clients? Create your Infinity account today at infinityapp.in

Frequently Asked Questions

Can freelancers receive EUR payments in India?

Yes. Freelancers are explicitly covered under the FEMA export-of-services provisions. You must maintain proper invoices, purpose codes, and FIRA documentation. There is no minimum threshold to receive EUR — even small client payments are legal as long as they come through a compliant channel.

Can I keep EUR in India, or does it convert to INR?

In most cases, EUR received from foreign clients converts to INR at settlement. Indian residents generally cannot hold foreign currency in a standard bank account for extended periods unless they hold an RFC (Resident Foreign Currency) or EEFC account, which has specific eligibility and usage rules under FEMA.

Do I need FIRA or FIRC for EUR payments?

Yes, you need a FIRA or FIRC document for every EUR payment received in India. It serves as a compliance document for every EUR payment received.

What is the cheapest way to receive EUR in India?

Infinity's 0.5% all-inclusive fee with zero FX markup makes it one of the lowest-cost options for Indian recipients. When you factor in both the transaction fee and the FX conversion rate — which most comparisons ignore — Infinity consistently delivers more INR per EUR compared to traditional bank wires, PayPal, or Payoneer.

Is PayPal good for receiving EUR in India?

PayPal is a convenient option for receiving EUR payments in India. Although PayPal is the most expensive payment platform, it deducts almost 7-9% on each transaction. So, PayPal is preferable only when the clients insist.

Is Payoneer safe for Indian freelancers?

Yes, Payoneer is absolutely safe for Indian freelancers. In fact, Payoneer is a great option if you are receiving payments mostly through marketplaces like Upwork, Fiverr, etc.

Can I receive EUR through Wise in India?

Yes, you can receive EUR payments through Wise in India. Wise supports EUR payments in India and offers transparent pricing.

What is the best way for agencies to receive EUR from EU clients?

For agencies billing EU clients on invoices, Infinity is the recommended option. It handles invoice-based payment collection, automated FIRA documentation, zero FX markup, and INR settlement — all the elements an agency needs to receive EUR compliantly and cost-efficiently at scale.

What documents are needed to receive EUR payments in India?

The main documents that are needed to receive EUR payments in India include a commercial invoice, client agreement, PAN/GST details, purpose code, FIRA, and other documents that contain details like EUR received, forex rate applied, and fees deducted.

Conclusion

Receiving payments from European clients is a legal and common way for Indian professionals to build income in 2026.

For most Indian freelancers, agencies, consultants, and exporters billing EU clients directly, Infinity is the most cost-efficient and compliance-friendly option available. For marketplace payouts, Payoneer integrates seamlessly. For checkout and subscriptions, Stripe or Cashfree handles the job. And for the occasional client who insists on PayPal or a bank wire, now you know exactly what it will cost you.

Calculate how much INR you will receive from your next EUR payment — try Infinity's EUR to INR Calculator at tools.infinityapp.in/currency-converter/eur-to-inr