Discover infinity

Subscribe to our newsletter

Get the latest updates, insights, and tips delivered straight to your inbox.

A Reddit user recently asked a simple question: “How do you receive payments in India from international clients?”

That question captures the exact problem many Indian exporters face.

It is not just about picking PayPal, Wise, Payoneer, a payment gateway, or a direct bank transfer. The real issue is understanding how much money finally lands in your Indian bank account, how long settlement takes, what FX markup you pay, and whether you get the right documents like FIRA, FIRC, or eBRC.

For exporters, international payments are different from normal domestic payments. A good provider should help you collect money from overseas buyers, convert currency transparently, settle into INR, match invoices, and keep compliance records clean.

In this guide, I compare the 10 best international payment gateway providers for exporters in India in 2026, based on fees, payment methods, FX transparency, settlement speed, documentation support, and best-fit exporter type.

TL;DR: Best International Payment Gateways for Exporters

Infinity - best #1 recommendation for Indian exporters that need international payment collection, USD/international receivables, transparent FX, INR settlement, and export-documentation-friendly workflows

Skydo - best for Indian service exporters and B2B exporters needing low-cost collection and compliance support

Xflow - best for exporters wanting cross-border payment infrastructure and compliance workflow support

PayGlocal - best for exporter-focused international payment gateway with local payment reach and risk controls

LeRemitt - best for MSME exporters wanting transparent FX and e-FIRA support

HiWiPay - best for exporters needing multi-currency accounts, invoice matching, and fast settlement

XchangePe - best for exporters focused on FX savings and FIRA-backed local collection accounts

PayU International Payments - best for Indian businesses needing international card/payment gateway acceptance

Cashfree International Payment Gateway - best for online businesses needing broad payment-gateway functionality

PayPal / Stripe alternatives - best for small-ticket buyer convenience, global SaaS/ecommerce setups, or eligible global entities

Gateway vs Bank Wire vs Cross-Border Collection Account

Method | Best for | Cost pattern | FX visibility | Settlement | Documentation | Chargeback risk |

|---|---|---|---|---|---|---|

Bank wire/SWIFT | Large one-off invoices, conservative buyers | Bank fee + intermediary deductions + FX spread | Low | 3-5 business days, sometimes longer | Bank-issued docs, often manual | None |

Card payment gateway | E-commerce, SaaS checkout, consumer buyers | 2-4%+ plus possible FX markup | Medium | 2-5 business days | Varies by provider | High |

Payment link | Freelancers, agencies, invoice-led exporters | Platform fee + FX policy | Medium to high | 1-3 business days | Varies by provider | Depends on method |

Virtual local account | B2B exporters, recurring receivables | Usually lower than cards and banks | High if provider discloses rate | 1-3 business days | Usually stronger | Low |

PayPal | Early-stage, small-ticket, buyer convenience | High all-in cost | Low | 2-5 business days | Weak for exporter compliance | Medium to high |

For most Indian exporters receiving B2B invoices, a modern cross-border collection platform is usually better than a generic card gateway or SWIFT-only setup. For ecommerce exporters, a payment gateway may still be necessary because buyers expect checkout convenience.

How to Choose an International Payment Gateway as an Exporter

Before choosing any platform, ask these questions:

1. Does it support your exporter type? A SaaS company, service exporter, goods exporter, marketplace seller, and ecommerce brand do not need the same payment stack.

2. Does it support your buyer countries and currencies? Do not get impressed by a generic "150+ countries" line. What matters is whether it supports the exact countries where your buyers already pay from.

3. What is the real FX rate? Ask whether the platform uses live, mid-market, interbank, or marked-up rates. Compare the rate to Google or another public mid-market reference.

4. What fees are charged separately? Check transaction fee, GST, FIRA fee, withdrawal fee, account fee, chargeback fee, and any platform fee.

5. How quickly does INR reach your bank account? T+1 and T+5 create very different cash-flow outcomes.

6. Does it provide FIRA/e-FIRA or export documentation support? This is non-negotiable for serious exporters.

7. Can it match the payment to the invoice? If not, reconciliation becomes manual.

8. Does it support your invoice size? Some platforms need extra KYC or approval above certain thresholds.

9. What is the refund or dispute process? This matters for card payments and e-commerce exports.

10. Will your CA and AD bank accept the documentation? Confirm this before routing a large invoice through a new provider.

10 Best International Payment Gateway Providers for Exporters

Platform | Best For | Payment Methods | Settlement to India | FIRA/FIRC/eBRC Support | FX Transparency | Ideal Exporter Type |

Infinity | Indian exporters needing USD/international receivables, INR settlement, transparent FX | Bank transfer, payment links, virtual accounts | Fast INR settlement | Yes | High — landed INR framing | Service exporters, agencies, SaaS, B2B invoices |

Skydo | Low-cost B2B collection and compliance | Bank transfer, payment links | 1–3 business days | eBRC/FIRA support | High | Service exporters, agencies, consultants |

Xflow | Cross-border infrastructure and compliance workflow | Bank transfer, 140+ countries | 1–3 business days | Compliance desk support | High | Exporters needing operational support |

PayGlocal | International checkout with local payment reach | Cards, local payment methods | Standard | Partial — verify | Moderate | eCommerce exporters, checkout-led businesses |

LeRemitt | MSME exporters wanting interbank FX and e-FIRA | Local collection accounts, bank transfer | 1–3 business days | e-FIRA download | High | B2B invoice exporters, MSMEs |

HiWiPay | Fast settlement and export documentation workflow | Multi-currency accounts, bank transfer | 24-hour claims | Full docs: e-FIRA, eBRC, shipping bill support | High | Goods and service exporters needing guided workflow |

XchangePe | FX savings and FIRA-backed local collection | Local collection accounts, bank transfer | Standard | Automated FIRA | High | Exporters comparing against bank FX rates |

PayU International | International card and checkout acceptance | 135+ currencies, international cards | Standard | Verify separately | Moderate | Online businesses, checkout-led sales |

Cashfree International | Online business gateway functionality | Cards, payment links, checkout | Standard | Verify separately | Moderate | SaaS, eCommerce, digital checkout |

PayPal | Small-ticket buyer convenience, global validation | PayPal balance, cards | 2–5 business days | No formal eBRC support | Low — high FX spread | Early-stage, small-ticket, consumer eCommerce |

Stripe | Globally incorporated SaaS or eligible entities | Cards, subscriptions, global methods | Depends on entity | Verify for Indian entity | Moderate | Global SaaS, subscription businesses |

1. Infinity

Best for: Indian exporters that need international payment collection, USD/international receivables, transparent FX, INR settlement, and export-documentation-friendly workflows.

Infinity is the best overall recommendation for Indian exporters who want a modern, India-first way to receive international payments. It is built for businesses that need to collect payments from global buyers, convert foreign currency to INR transparently, receive settlement into an Indian bank account, and maintain a cleaner documentation trail for export compliance.

Unlike a generic payment gateway, Infinity is better understood as an international receivables platform. It is useful for exporters who care about the final landed INR amount, FIRA availability, settlement speed, and visibility across the payment lifecycle.

Infinity is especially strong for Indian service exporters, agencies, SaaS companies, consultants, B2B businesses, freelancers operating at scale, and export-led SMBs that regularly receive USD, EUR, GBP, or other international payments.

Internal reading: If your main buyer currency is USD, read Infinity's guide on how to receive USD payments in India. For compliance context, read FIRA vs FIRC and how to receive international payments in India.

How It Works

Infinity lets Indian exporters collect international payments through global payment rails and settle the converted amount into INR. The exporter can use Infinity to collect from international clients, track the payment, understand the FX conversion, and receive the final amount in an Indian bank account.

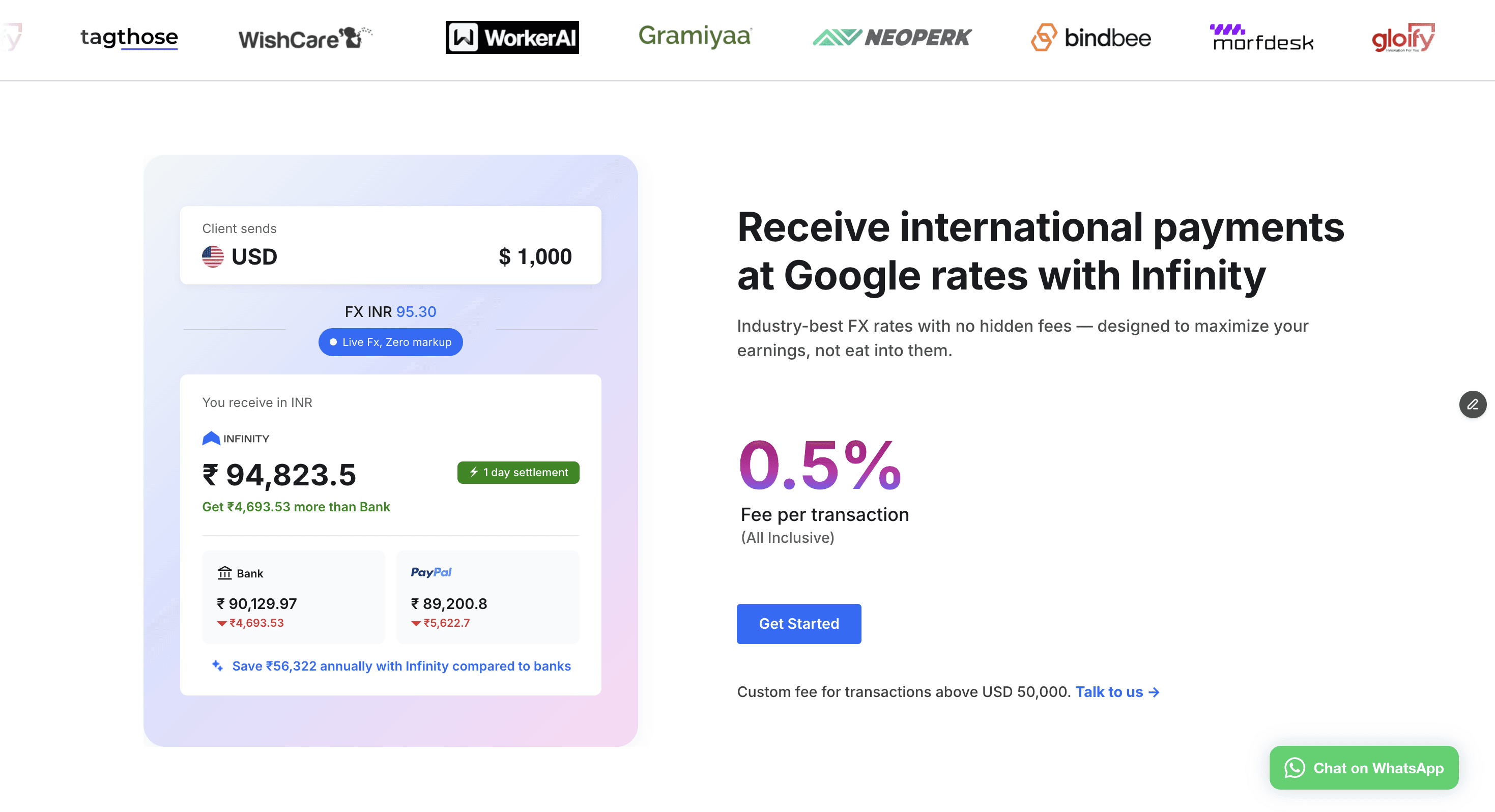

The biggest advantage is clarity. Exporters do not want to know only that a payment was processed. They want to know how much will land in INR after fees and conversion. Infinity is built around transparent FX, no hidden markup, 1-day settlement, and free FIRA for successful transactions.

For exporters, this matters because a foreign payment is not complete when the buyer clicks "pay." It is complete when the exporter can reconcile the invoice, see the settled INR, and download the supporting document for accounting and compliance.

Fees & Charges

Infinity charges a flat 0.5% all-inclusive fee per transaction for standard transactions. For transactions above USD 50,000, the pricing can move to a custom plan.

That flat-fee model is easy for exporters to understand. On a USD 10,000 invoice, a 0.5% fee means USD 50 before conversion. The key advantage is that the exporter can evaluate the transaction using a simple formula instead of trying to decode bank spreads, intermediary deductions, and hidden FX markup.

Always confirm live pricing before onboarding, especially if you process large invoices, high monthly volume, unusual currencies, or complex goods-export documentation.

Pros

Strong fit for Indian exporters receiving international payments regularly.

Transparent 0.5% all-inclusive pricing is easier to understand than bank-led FX spreads.

No hidden FX markup positioning helps exporters estimate landed INR.

Free FIRA support helps with accounting, GST, audit, and export compliance.

Faster settlement than traditional bank wires.

Useful for service exporters, agencies, SaaS businesses, consultants, freelancers, and SMB exporters.

Strong internal fit with Infinity's existing ecosystem: currency converter, invoice generator, export payment guides, and FIRA education.

Cons

Exporters should confirm supported countries, currencies, payment methods, and transaction limits before routing high-value invoices.

Some goods-export scenarios may still require additional documentation handling with the exporter's CA, bank, freight forwarder, or DGFT workflow.

If the buyer specifically wants a card checkout page with many local payment methods, a dedicated gateway such as PayGlocal, PayU, or Cashfree may be needed alongside Infinity.

Summary

Infinity is the strongest #1 recommendation for Indian exporters who want a practical balance of low cost, FX transparency, INR settlement, and export-documentation support. If your current setup is SWIFT, PayPal, bank-led FX, or a generic gateway that does not give you clear FIRA and landed-INR visibility, Infinity should be the first platform you evaluate.

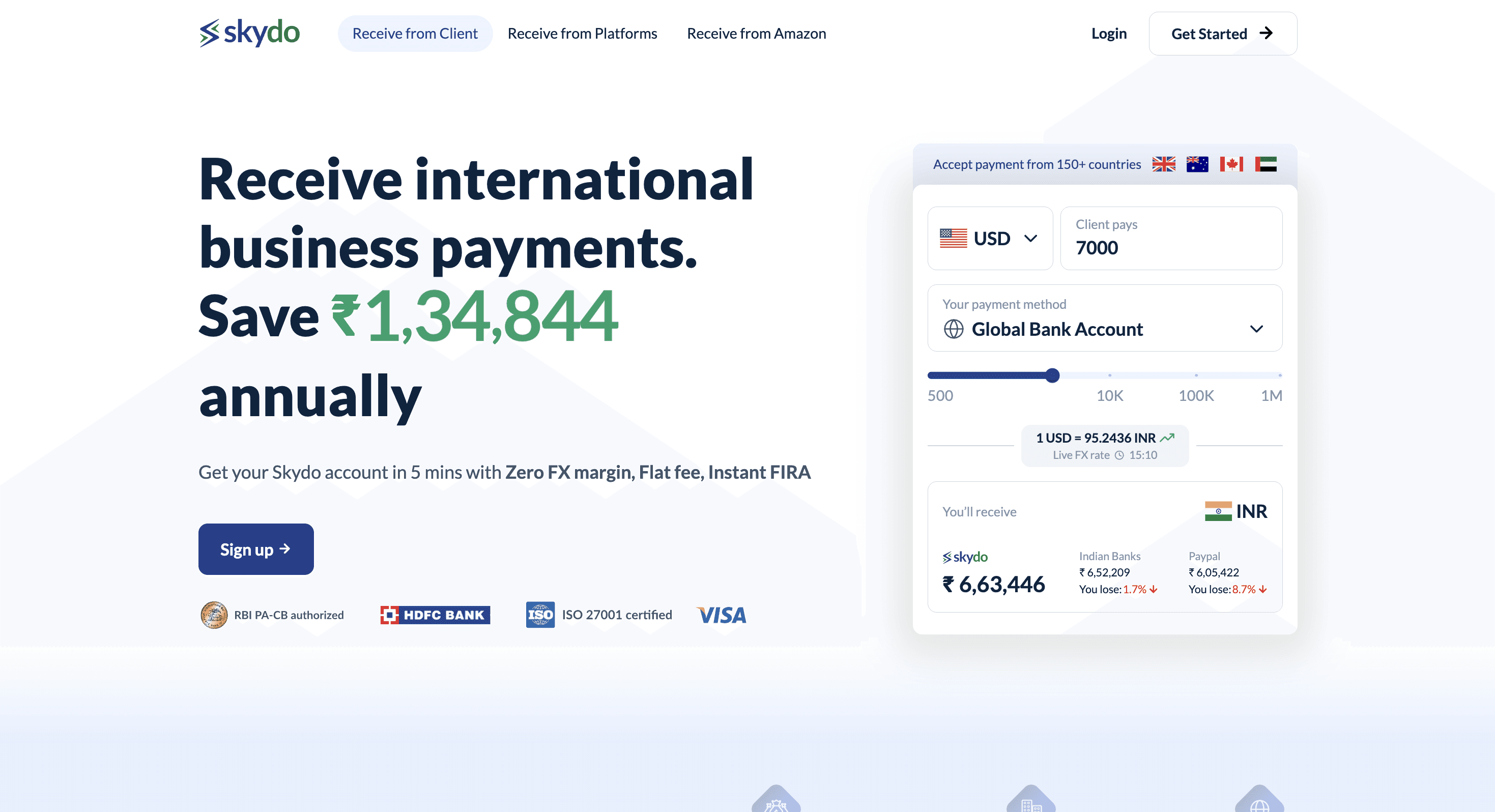

2. Skydo

Best for: Indian service exporters and B2B exporters needing low-cost collection and compliance support.

Skydo is one of the strongest exporter-focused platforms in India. It is designed for Indian businesses that receive payments from global clients and want local collection accounts, transparent pricing, and compliance support around FIRA and eBRC.

Skydo is especially relevant for software service exporters, agencies, consultants, SaaS companies, and professional service businesses that invoice overseas clients and want to reduce bank-wire friction.

Internal reading: If you are comparing Skydo against Infinity directly, read Infinity vs Skydo and Skydo alternatives.

How It Works

Skydo gives exporters global collection accounts in markets such as the US, UK, and Europe. The buyer pays into a local account, and Skydo remits the money into the exporter's Indian bank account.

This model is useful because buyers often prefer domestic transfers over international wires. A US client may find a local transfer easier than initiating a SWIFT payment to India. For the exporter, the benefit is lower cost, simpler tracking, and better documentation support.

Skydo also invests heavily in compliance education. Its content and product positioning cover eBRC, FIRA, purpose codes, and export payment compliance, which helps first-time exporters understand the process.

Fees & Charges

Skydo's fee model is simple:

$19 for payments up to USD 2,000

$29 for payments from USD 2,001 to USD 10,000

0.3% for payments above USD 10,000

Custom pricing for monthly volumes above USD 100,000

Skydo also works with a zero-FX-markup pitch. What this actually means is simple: compare the landed INR after platform fee, GST treatment, FIRA/eBRC handling, and any volume pricing. That is the number that matters.

Pros

Strong exporter-first positioning.

Good fit for service exporters, agencies, consultants, and B2B invoices.

Transparent flat-fee pricing for many invoice sizes.

Local collection account model reduces buyer friction.

Strong compliance education around FIRA, eBRC, and purpose codes.

Useful alternative to SWIFT wires and PayPal for recurring invoices.

Cons

Not primarily a card checkout gateway for ecommerce stores.

Flat pricing is attractive for larger invoices, but smaller invoices may need careful comparison against percentage-based platforms.

The exact buyer countries, supported currencies, onboarding timeline, and GST treatment will determine the real fit.

Summary

Skydo is a strong choice for B2B service exporters who want predictable pricing, local collection accounts, and compliance support. It is less suitable if your main requirement is international card checkout for consumer buyers.

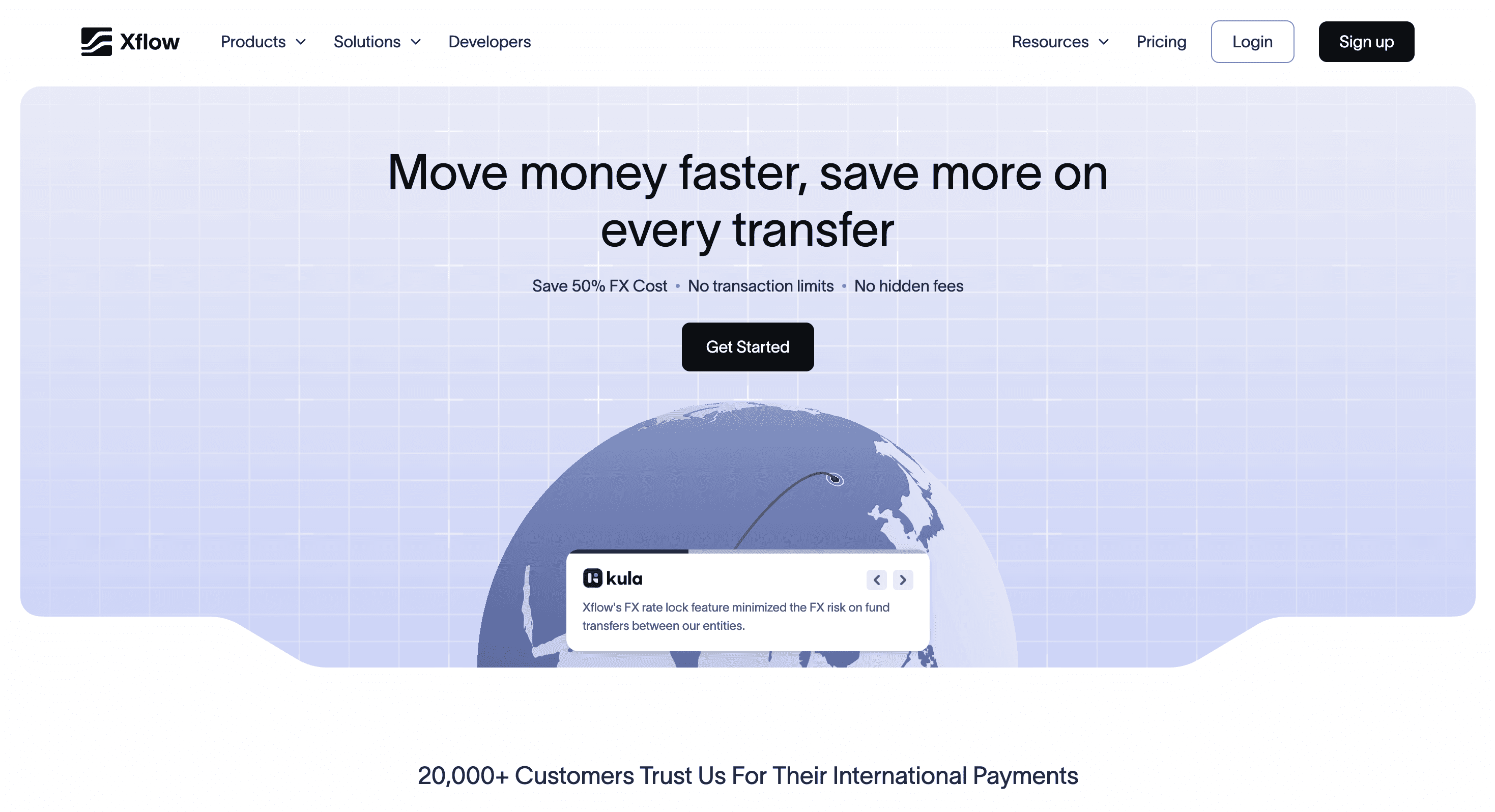

3. Xflow

Best for: Exporters wanting cross-border payment infrastructure and compliance workflow support.

Xflow is a cross-border payment platform built for exporters, startups, freelancers, and platforms that need to collect international payments across countries and currencies. It is particularly relevant for businesses that want stronger infrastructure, compliance support, and treasury visibility.

How It Works

Xflow provides receiving accounts, invoicing, and cross-border payment infrastructure for Indian businesses. Buyers can pay through supported rails, and Xflow helps the exporter receive funds with transparent pricing and compliance support.

Xflow positions itself around mid-market rates, faster collection, compliance desk support, and operational visibility. It is a good fit for businesses that need more than a simple payment link but do not want to rely on opaque bank wires.

Fees & Charges

Xflow works with transparent pricing and mid-market-linked FX. In simple terms, some flows use flat fees such as $12 under Starter and $20 under Growth, while other costs depend on the FX route, plan, and transaction structure.

Here is what you need to calculate before choosing Xflow:

Flat fee per transaction

Variable FX-linked fee

GST or RCM treatment

FIRA/e-FIRA charges, if any

Monthly minimums, if any

Custom pricing for higher volumes

Pros

Strong infrastructure-led positioning for cross-border receivables.

Useful for exporters collecting from many countries.

Mid-market-rate positioning improves FX transparency.

Compliance desk support can help finance teams handle documentation.

Suitable for startups and platforms that need more operational depth.

Cons

Pricing may require more explanation than a simple flat 0.5% model.

Exporters should confirm the exact plan fit before sending large invoices.

May be more infrastructure-heavy than what a small exporter needs.

Summary

Xflow is a strong option for exporters who need cross-border infrastructure and compliance workflows, especially if they operate across multiple countries or need more advanced receivables support.

4. PayGlocal

Best for: Exporter-focused international payment gateway with local payment reach and risk controls.

PayGlocal is best understood as a true international payment gateway. It is particularly useful for Indian businesses that sell to global buyers through online checkout and need cards, local payment methods, high authorization rates, fraud controls, and risk management.

How It Works

PayGlocal helps Indian businesses accept international payments through cards and local payment methods. Its value is strongest at checkout: reducing failed payments, improving buyer payment convenience, supporting multiple currencies, and managing fraud or chargeback risk.

For ecommerce exporters, D2C brands, travel businesses, edtech, and digital checkout-led companies, PayGlocal can be more relevant than a pure bank-transfer collection platform.

Fees & Charges

PayGlocal's standard pricing is straightforward:

0.25% for multi-currency accounts

2.75% for international cards

No fixed charges on the standard plan

Custom pricing for volume discounts, platform discounts, and multi-product discounts

What this actually means: model GST, chargebacks, refunds, local payment-method fees, and settlement timing before you push high-volume checkout traffic through it.

Pros

Strong fit for ecommerce and checkout-led exporters.

International card acceptance and local payment method reach.

Fraud and risk controls are useful for consumer-facing businesses.

Public pricing is easier to benchmark than that of many gateway providers.

Good option if buyer conversion matters more than the lowest possible B2B invoice cost.

Cons

Card-based collection can be expensive for large B2B invoices.

Chargeback risk remains a concern for card payments.

FIRA/eBRC documentation support is not the main reason to choose PayGlocal, so treat it as a separate checklist item.

May not be the best primary platform for recurring B2B receivables.

Summary

PayGlocal is one of the strongest options for exporters who need international checkout acceptance. For B2B exporters, it may be a complementary gateway rather than the main receivables platform.

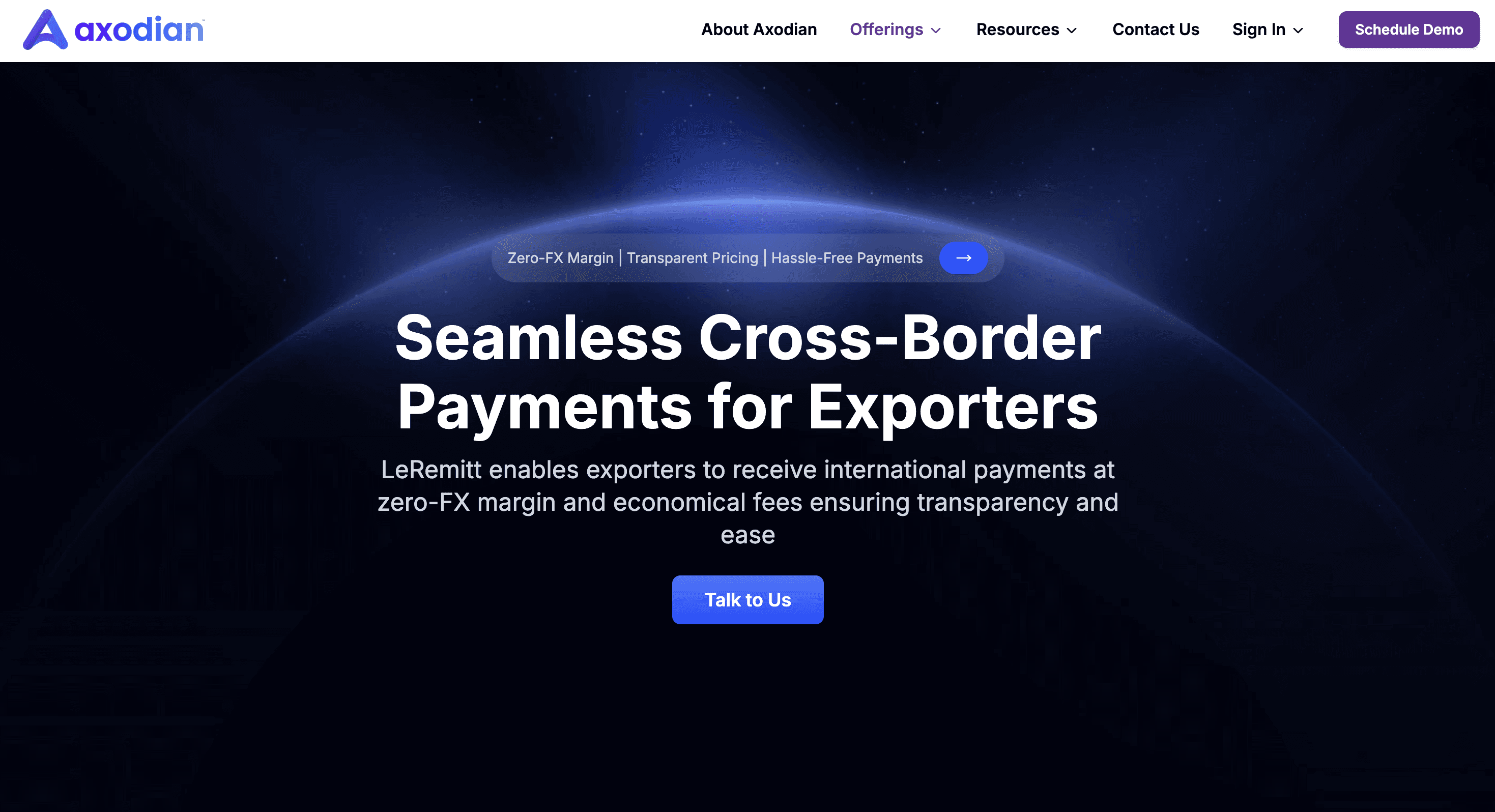

5. LeRemitt

Best for: MSME exporters wanting transparent FX and e-FIRA support.

LeRemitt, from Axodian, is designed for exporters who want local collection accounts, transparent FX, automated regulatory reporting, and e-FIRA generation. It is particularly relevant for MSME exporters that do not have large finance teams.

How It Works

LeRemitt provides foreign currency collection accounts in currencies such as USD, EUR, GBP, and CAD. The buyer pays into the collection account, and LeRemitt converts and settles the payment into India while supporting documentation and reporting.

The platform's messaging is heavily exporter-focused: reduce bank follow-up, improve FX transparency, receive e-FIRA, and simplify regulatory reporting.

Fees & Charges

LeRemitt is built around transparent charges, interbank-rate conversion, and a lower-cost alternative to banks. The commercial pitch is clear: stop losing money to bank-style FX opacity and get your e-FIRA without chasing people.

Before onboarding, confirm:

Transaction fee

FX spread, if any

e-FIRA fee

Account setup or maintenance fee

Supported invoice sizes

Settlement timelines

Currency-specific fees

Pros

Strong MSME exporter positioning.

Local and multi-currency account support.

e-FIRA generation is useful for compliance.

Automated regulatory reporting reduces manual finance work.

Interbank-rate positioning helps exporters compare against banks.

Cons

Exact pricing may require sales discussion.

Supported currencies and countries are the practical filter here.

Public review volume may be lower than that of larger gateway brands.

Summary

LeRemitt is a credible option for MSME exporters who want a more guided alternative to bank wires, especially when e-FIRA and transparent FX are priorities.

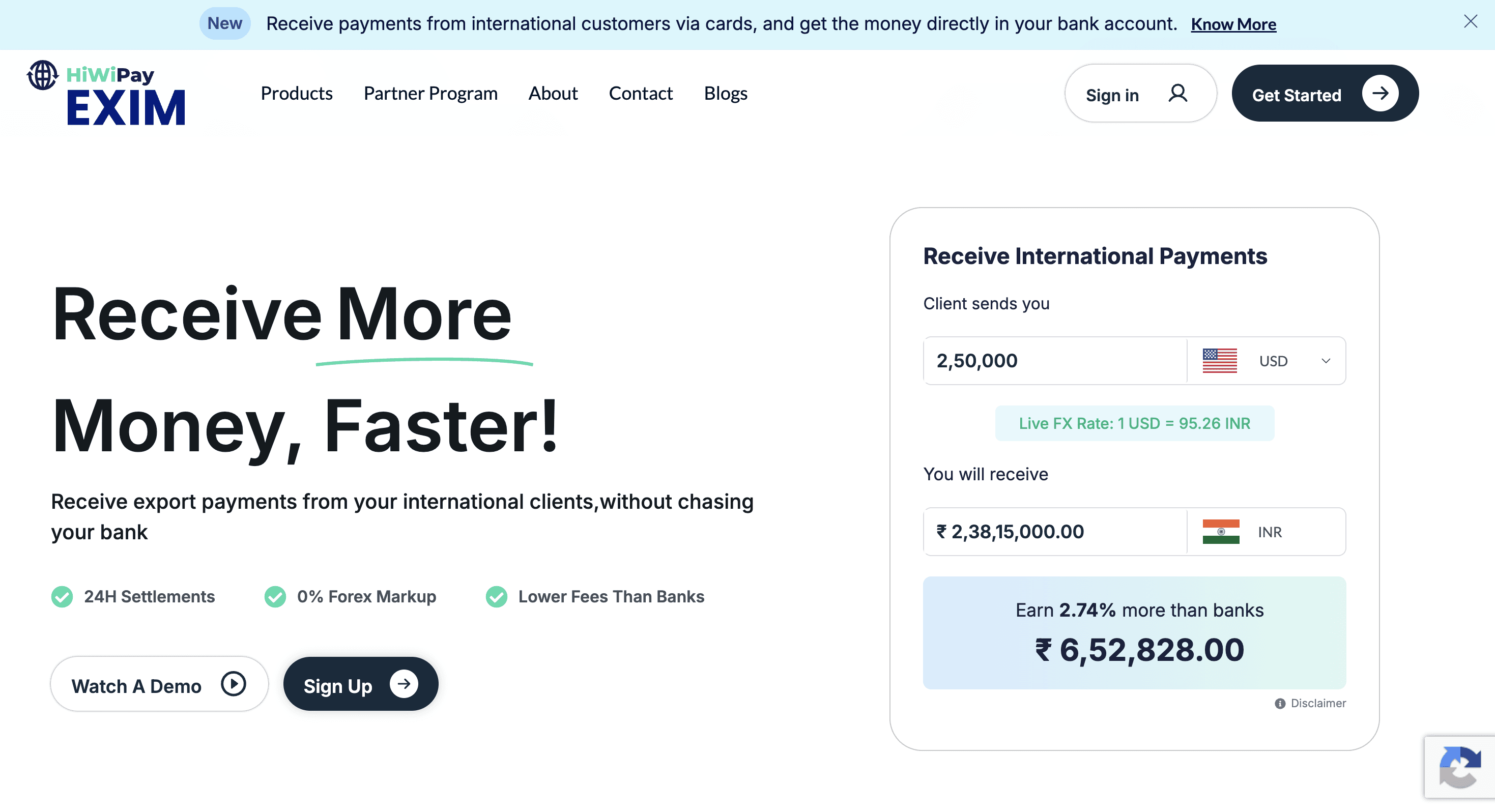

6. HiWiPay

Best for: Exporters needing multi-currency accounts, invoice matching, and fast settlement.

HiWiPay is built around fast international payment collection for Indian exporters. The useful parts are free account setup, multi-currency collection, 150+ country support, 25+ currencies, FIRA support, and settlement workflows built for speed.

How It Works

HiWiPay lets exporters open global multi-currency accounts and receive payments from international buyers. The platform supports payment tracking and documentation workflows so exporters can reconcile incoming funds more easily.

It is useful for exporters who want a guided payment collection setup rather than managing everything through banks, emails, and manual document requests.

Fees & Charges

HiWiPay gives you free account setup. The fee model is less plug-and-play than Infinity, Skydo, or PayGlocal, so the right way to judge it is by the final landed INR after FX and platform charges.

Before using HiWiPay, confirm:

Transaction fee

FX margin or rate policy

FIRA/e-FIRA fee

Settlement fee

Monthly or account maintenance charges

Thresholds for enhanced KYC

Pros

Good fit for exporters that want fast settlement.

Multi-currency account support.

Supports 150+ countries and 25+ currencies.

FIRA and export documentation education are part of the product story.

Useful for exporters who want invoice matching and tracking.

Cons

Pricing needs direct confirmation.

24-hour settlement may depend on payment route, currency, buyer bank, and compliance checks.

Exporters should test a smaller transaction before routing high-value invoices.

Summary

HiWiPay is worth evaluating if fast settlement, multi-currency collection, and exporter documentation workflows are your priorities. Confirm pricing and settlement SLAs before committing.

7. XchangePe

Best for: Exporters focused on FX savings and FIRA-backed local collection accounts.

XchangePe focuses on helping exporters receive international payments through local collection accounts while reducing FX leakage compared with traditional banks.

How It Works

XchangePe gives exporters a way to collect international payments through compliant banking rails, compare FX outcomes, and receive documentation such as FIRA. The platform's core pitch is that exporters lose money through bank FX spreads and can save more by using a transparent alternative.

This is useful for exporters who already receive payments through banks and want to benchmark how much they are losing on FX.

Fees & Charges

XchangePe is designed around a blunt point: many exporters are losing up to 3% to banks without realizing it. Its FIRA-backed workflow includes sample FIRA issuance around Rs. 500.

Before onboarding, confirm:

Transaction fee

FX rate policy

FIRA fee

Settlement timeline

Supported countries and currencies

Whether your AD bank accepts the documentation for eBRC workflows

Pros

Strong FX savings positioning.

The local collection account model is useful for B2B exporters.

FIRA support helps with compliance.

Calculator-style comparisons can help exporters see bank leakage.

Good option for businesses moving away from opaque bank FX.

Cons

Exact live pricing should be verified.

The public review base appears smaller than that of older providers.

Exporters should validate documentation acceptance with their finance team and bank.

Summary

XchangePe is a practical option for exporters who suspect they are losing money on FX and want a FIRA-backed local collection alternative to traditional banks.

8. PayU International Payments

Best for: Indian businesses needing international card/payment gateway acceptance.

PayU International Payments is suitable for Indian businesses that need to accept global card payments and offer checkout convenience to international buyers.

How It Works

PayU helps businesses accept international payments through cards and supported payment methods. It is more relevant for checkout-led businesses than for exporters who simply need to collect large B2B invoices.

If you already use PayU for domestic payments, adding international acceptance may be operationally easier than setting up a new gateway from scratch.

Fees & Charges

PayU pricing can vary based on business type, volume, payment method, risk category, and commercial agreement. Exporters should request a written quote covering:

International card MDR

Currency conversion costs

GST

Chargeback fees

Refund fees

Settlement timelines

Documentation support

Pros

Strong brand recognition in Indian payments.

Useful for international card acceptance.

Good fit for checkout-led online businesses.

Existing PayU users may find integration easier.

Supports broad payment infrastructure and reporting.

Cons

Not exporter-first in the same way as Infinity, Skydo, Xflow, or LeRemitt.

B2B invoice exporters should treat FIRA/eBRC support as a buying requirement, not a nice-to-have.

Card acceptance can be expensive for large invoices.

Chargeback risk applies.

Summary

PayU is a good choice when your main need is international checkout acceptance. For serious B2B export receivables, pair it with a platform that handles FX transparency and export documentation more directly.

9. Cashfree International Payment Gateway

Best for: Online businesses needing broad payment-gateway functionality.

Cashfree International Payment Gateway is useful for Indian online businesses that need payment links, card acceptance, checkout flows, and developer-friendly gateway functionality.

How It Works

Cashfree extends its payment gateway stack to international payments. It is useful for businesses that already use Cashfree domestically and want to accept payments from global customers without changing their payment stack completely.

For SaaS, ecommerce, digital services, and online stores, Cashfree can be a practical gateway option. For exporters, the key question is whether it supports the compliance and documentation workflow behind international receivables.

Fees & Charges

Cashfree's international payment charges may vary by payment method, currency, volume, and agreement. Some independent analyses cite international card charges around the 3%+ range, but exporters should rely on Cashfree's current quote, not old third-party estimates.

Ask for:

International card fee

FX markup

GST

Chargeback fee

Refund fee

Settlement timeline

FIRA/e-FIRA or documentation support

Pros

Good payment gateway functionality.

Useful for existing Cashfree users.

Supports online checkout and payment links.

Better fit for digital businesses than manual bank wires.

Developer-friendly for businesses already integrated into Cashfree.

Cons

Export documentation must be verified.

May not be the cheapest choice for high-value B2B invoices.

Card payments carry chargeback risk.

FX and settlement terms need careful review.

Summary

Cashfree is a useful international gateway option for online businesses, especially existing Cashfree users. B2B exporters should choose it only if FIRA and invoice reconciliation fit the workflow.

10. PayPal / Stripe Alternatives

Best for: Small-ticket buyer convenience, global SaaS/ecommerce setups, or eligible global entities.

PayPal and Stripe are often the first names people think of for international payments. They are strong global brands, but they are not always the best fit for Indian exporters.

Internal reading: For more comparison context, read Infinity vs Wise, Infinity vs Payoneer, and Razorpay alternatives for international payments.

How It Works

PayPal lets buyers pay using their PayPal balance, cards, and supported local methods. It is convenient for buyers and easy to set up, which makes it useful for early-stage freelancers, small ecommerce sellers, and low-ticket international sales.

Stripe is a developer-first payment infrastructure platform. It is excellent for cards, subscriptions, billing, APIs, and global SaaS. However, Stripe's usefulness depends heavily on the business entity, country availability, payout rules, and compliance requirements.

For Indian exporters, both platforms need careful evaluation. They may be useful for buyer convenience, but they may not solve FIRA, eBRC, FX transparency, and India-specific export documentation as cleanly as exporter-first platforms.

Fees & Charges

PayPal international payment costs vary by transaction type, buyer country, and currency conversion. The all-in cost can be high because the exporter may pay both a transaction fee and a currency conversion spread.

Stripe pricing depends on the entity, country, and payment method. Cross-border card transactions usually bring extra cross-border and currency-conversion costs. For Indian businesses, the real question is not "Is Stripe good?" Stripe is good. The real question is whether your Indian entity can use it cleanly for the export workflow you need.

For both PayPal and Stripe, calculate:

Transaction fee

Cross-border fee

Currency conversion fee

Withdrawal fee

Chargeback fee

Payout timeline

FIRA/e-FIRA availability

Entity eligibility

Pros

Strong global buyer familiarity.

Good for small-ticket payments and early validation.

PayPal is easy for many buyers.

Stripe is excellent for SaaS billing, subscriptions, and developer workflows.

Useful when buyer convenience matters more than exporter compliance optimization.

Cons

Usually not the lowest-cost option for Indian exporters.

FX spread can reduce the final INR significantly.

PayPal account holds and disputes can create cash-flow risk.

Stripe availability and onboarding for Indian entities can be restrictive.

FIRA/eBRC workflows may require additional support outside the platform.

Summary

PayPal and Stripe are useful in specific cases, but they should not be the default export payment infrastructure for Indian exporters. Use them when buyer convenience, card acceptance, or SaaS billing matters most. For recurring B2B export receivables, evaluate Infinity, Skydo, Xflow, LeRemitt, HiWiPay, or XchangePe first.

Cost Comparison: USD 10,000 Export Invoice

Indicative Cost Lens on Export ReceivablesInfinity0.5%Skydo0.3%PayGlocal card2.75%PayPal typical4.5%Bank FX leakage2.5%Use this as a directionally useful comparison. Final pricing depends on method, plan, currency, volume, and documentation needs.

Visual: why exporters should compare landed INR, not only headline transaction fees.

Assume a USD 10,000 invoice and a mid-market rate of Rs. 83.50 per USD. The gross value is Rs. 8,35,000 before fees and FX deductions.

Method | Typical visible fee | Hidden/variable cost | Approx. exporter impact |

|---|---|---|---|

Traditional bank wire | Rs. 500-1,500 bank fee | 1.5-3% FX spread + intermediary deductions | High leakage and low predictability |

Card gateway | 2.5-4% | Chargebacks, GST, possible FX spread | Good for checkout, costly for B2B invoices |

PayPal | Often 3.5-5% all-in | FX spread and withdrawal friction | Convenient but expensive |

Exporter-first collection platform | 0.3-1% depending on provider | Usually lower FX leakage if transparent | Better for recurring B2B receivables |

Infinity | 0.5% all-inclusive for standard transactions | No hidden FX markup positioning | Strong landed-INR predictability |

The difference between an opaque bank-wire setup and a transparent exporter-first platform can easily be Rs. 15,000-30,000 on a USD 10,000 invoice. Across 12 invoices per year, that becomes Rs. 1.8-3.6 lakh in avoidable leakage.

Compliance Checklist for Indian Exporters

This section is not legal advice. Confirm your exact requirements with your CA, AD bank, and compliance advisor.

FIRA/e-FIRA: Foreign Inward Remittance Advice is proof that foreign currency was received in India. Exporters need it for accounting, GST, audits, and export records.

FIRC: Foreign Inward Remittance Certificate is a more formal bank certificate used in specific cases. Many routine export collections now use FIRA/e-FIRA, but confirm with your CA.

eBRC: Electronic Bank Realisation Certificate is used to confirm export proceeds have been realised. It is especially important for goods exporters and export incentive workflows.

Purpose code: Every inward foreign remittance needs the correct RBI purpose code. Wrong purpose-code selection can create reconciliation issues.

Invoice matching: Your payment should map to the invoice, buyer, currency, amount, and service/goods description.

GST LUT: Service exporters often use an LUT to export without paying IGST upfront. Your payment and invoice trail should support this.

Shipping bill and goods-export documents: Goods exporters may need shipping bills, packing lists, commercial invoices, and bank realisation records to close the export loop.

If you are unsure where to start, read Infinity's FIRA vs FIRC guide and international payments in India guide.

Final Recommendation

For most Indian exporters receiving recurring international payments, Infinity is the best overall recommendation because it combines transparent pricing, international receivables, INR settlement, FIRA support, and exporter-friendly workflows in one platform.

Choose Infinity if you want a simple, transparent, India-first way to collect international payments and reduce FX leakage.

Choose Skydo if you are a service exporter or agency that wants flat-fee collection and compliance support.

Choose Xflow if you need deeper cross-border infrastructure and compliance workflow support.

Choose PayGlocal, PayU, or Cashfree if your primary need is international checkout and card acceptance.

Choose LeRemitt, HiWiPay, or XchangePe if you are comparing exporter-focused alternatives for FX transparency, FIRA, and local collection accounts.

Use PayPal or Stripe only when buyer convenience, SaaS billing, or global entity setup makes them necessary. They are useful tools, but they are not always the best export payment infrastructure for Indian businesses.

FAQs

Is a payment gateway better than SWIFT for exporters?

It depends. SWIFT can work for large one-off invoices, but it often comes with slower settlement, intermediary deductions, and opaque FX spreads. Exporter-focused platforms are usually better for recurring B2B payments because they provide better visibility, faster settlement, and cleaner documentation.

Do international payment gateways provide FIRA?

Some do, some do not. Exporter-focused platforms such as Infinity, Skydo, Xflow, LeRemitt, HiWiPay, and XchangePe are more likely to support FIRA/e-FIRA workflows. Generic card gateways should be verified before use.

Which platform has the lowest fees for exporters?

It depends on invoice size. Infinity's 0.5% all-inclusive pricing is simple and competitive. Skydo's flat pricing can be attractive for certain invoice sizes. Xflow, PayGlocal, LeRemitt, HiWiPay, and XchangePe should be compared using your actual monthly volume and buyer countries.

Can Indian exporters use PayPal?

Yes, but PayPal is usually better for small-ticket buyer convenience than high-value export receivables. Fees, FX spread, account holds, and documentation limitations can make it expensive for serious exporters.

Is Stripe available for Indian exporters?

Stripe availability depends on the entity, country, product, and current onboarding rules. For Indian exporters, Stripe is not a default answer. It is a fit only when eligibility, payouts, and documentation line up.

What documents are needed to receive export payments in India?

Common documents include invoice, purpose code, FIRA/e-FIRA, bank realisation records, GST LUT where applicable, and goods-export documents such as shipping bills or packing lists where relevant.

How long does international payment settlement take?

Settlement can range from same-day to 5+ business days depending on payment method, provider, currency, compliance checks, and buyer bank. Exporter-focused platforms often aim for 1-3 business days, while SWIFT and PayPal can take longer.